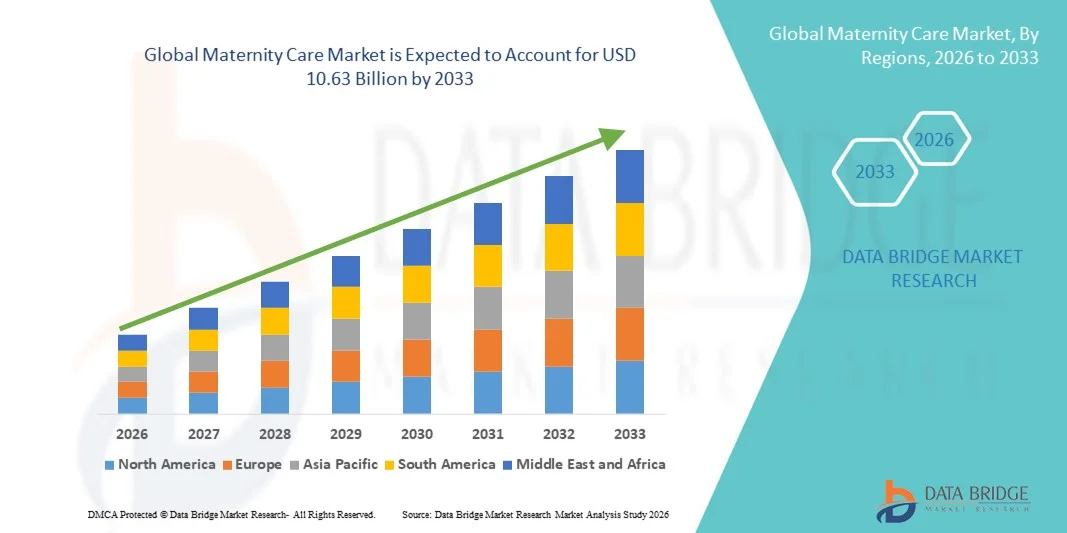

Maternity Care Market Size, Share, Trends, and Industry Forecast by 2033

Other |

2026-06-05 09:39:09

As companies plan their 2026 agendas, the acrolein market presents a profile of steady expansion, concentrated supply, and regulatory complexity. Our baseline analysis (base year 2025) shows the market recovering from near-term volatility and tracking a measured compound annual growth rate (CAGR) of 3.02% across the 2026–2032 forecast window. PW Consulting’s new Acrolein Market study synthesizes historical performance (2020–2025), supply-side shifts, feedstock dynamics, and regulatory inflection points into a decision-ready framework for commercial, sourcing, and M&A leaders.

Acrolein Market

Viewed through the lens of system-level totals, the global acrolein market grew from approximately USD 944.0 Million in 2020 to USD 1,089.0 Million in 2025 (base year). Under our central forecast trajectory, the market expands to roughly USD 1,103.1 Million in 2026 and reaches an estimated USD 1,347.0 Million by 2032. The modest but consistent CAGR of 3.02% signals a market that is not hyper-growth, but rather structural growth driven by downstream demand stability and incremental new uses.

Acrolein Market

For executives, that profile calls for calibrated moves: prioritize operations and contracts that preserve margin in a low-to-mid-single-digit growth environment, and target selective investments that leverage scale or integration advantages rather than broad capacity gambits. The numbers favor targeted consolidation, downstream integration plays, and product-differentiation strategies over large, undirected greenfield builds.

Acrolein Market

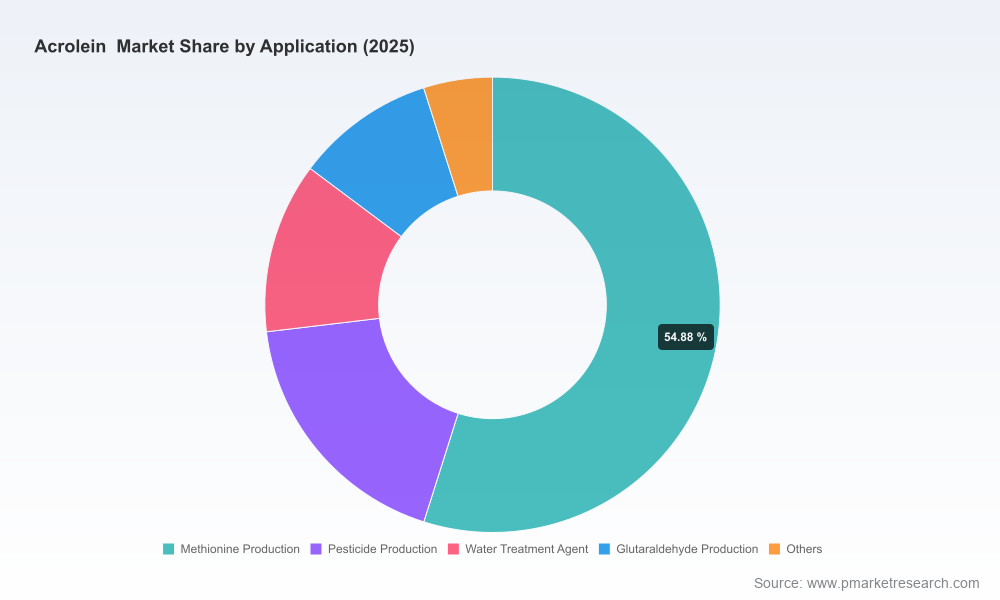

Downstream resilience: Established derivative streams — including feedstocks for amino-acid synthesis, water treatment chemistries, and pesticide intermediates — provide base load demand that cushions cyclical swings in broader chemicals markets.

Commodity feedstock linkages: Propylene and other upstream feedstock dynamics remain the primary short-run cost drivers. Recent observations of propylene price stability in early 2026 contributed directly to a more stable acrolein price index across producers, reducing near-term margin pressure for integrated operators.

Incremental application growth: Emerging product applications and regional infrastructure programs create pockets of higher-than-average demand; these are best approached with modular supply strategies rather than full-scale capacity deployments.

Regulation is a defining risk/option set for acrolein users and producers in 2026. The U.S. Environmental Protection Agency (EPA) has taken actions that materially affect the operating envelope for acrolein-based products. An interim registration review decision in February 2024 identified acute ecological risk concerns and additional data requirements for pollinator and ecological impact pathways. Subsequent EPA determinations have treated certain irrigation-canal herbicide uses as restricted, reflecting a tighter approval environment for conventional uses that pose high ecological exposure.

Practically, this means buyers and producers must factor conditional use restrictions, monitoring obligations, and potential label constraints into commercial and product development decisions. For companies supplying water-treatment, irrigation, or open-environment pesticide markets, a regulatory contingency plan is now a standard element of the commercial playbook.

The market exhibits measurable concentration: the top three suppliers account for a majority share of global capacity, and the top five increase that share further. That concentration (CR3 ~57%, CR5 ~63%) creates predictable negotiation dynamics — buyers face fewer atomic suppliers for spot or short-term contracts, while large sellers gain pricing and allocation leverage, especially during constrained feedstock cycles.

For corporate strategy, this concentration creates three immediate options:

Secure multi-year offtakes or equity-in-contracts with integrated producers to guarantee feedstock volumes and mitigate allocation risk.

Pursue vertical integration into derivative chains (e.g., methionine intermediates or specialized water-treatment formulations) to capture margin and reduce exposure to commodity pricing cycles.

Target bolt-on acquisitions that add complementary capabilities or regional presence rather than large-scale capacity purchases that carry long payback periods in a slow-growth market.

Our analysis emphasizes the strategic positioning of a mix of integrated multinationals and regional specialists. Key players include established chemical groups operating integrated value chains and a set of regional manufacturers focused on fine-chemical and intermediate markets.

Multinational integrated producers: Global players with methionine-oriented downstream integration maintain preferential access to derivative demand streams and typically manage a broader risk posture by internalizing margin capture. Their site footprints — including North American and European manufacturing locations — support diversified distribution and technical service capabilities tailored to feedstock users.

Specialist domestic manufacturers: Several China-based producers operate dedicated acrolein capacities within fine-chemical clusters and have been expanding production bases to serve export and domestic demand. These suppliers often offer competitive pricing and agility in customized intermediates but face margin pressure when feedstock costs rise or when regulatory adjustments affect export markets.

Industrial service suppliers: Certain engineering and oilfield service companies produce acrolein to support niche applications (for example, oilfield bacteria and sulfide control programs), reflecting the product’s functional versatility across industrial sectors.

Understanding each counterparty’s strategic role — integrated margin capture, regional cost advantage, or niche-service orientation — is essential to negotiating commercially constructive agreements in 2026.

Production expansions in the United States in 2025 increased domestic supply capacity by roughly 10%, a tactical response to both rising local demand and export opportunities. This changes logistics and allocation dynamics for North American purchasers and can create temporary regional softness in spot markets.

Feedstock stability—particularly propylene—has eased short-term pricing volatility in early 2026, offering an opportunity window for contract renegotiations and cost-based tender strategies.

The report is structured to support immediate decision-making and near-term planning cycles. Key deliverables include:

A consolidated historical dataset (2020–2025) and an integrated forecast model (2026–2032) with scenario toggles for regulatory tightening, feedstock shocks, and demand-side shifts.

Supplier mapping and concentration analysis, with profiles of incumbent producers, asset-level capacity notes, and commercial behavior archetypes to inform negotiation and sourcing playbooks.

Regulatory impact matrices that translate EPA and equivalent jurisdictional actions into operational triggers: label constraints, data requirements, use restrictions, and compliance timelines.

Price-sensitivity and margin modelling tools that allow users to stress-test value chains under different propylene and energy-price scenarios.

Actionable checklists for procurement, M&A screening templates for bolt-on target evaluation, and go-to-market playbooks for launching derivative products or reformulated chemistries under constrained-use conditions.

Importantly, the report contains the granular regional and application-level forecasts and unit economics that underpin the top-line trajectories described here — information we intentionally withhold in this overview to preserve the integrity of the purchased dataset and to encourage direct engagement for full access.

Procurement leaders: Use the price-sensitivity models to reset multi-year contracts and to frame cost-plus versus fixed-price negotiations during the propylene stability window.

Business development and R&D: Prioritize derivative formulations and value-added services that insulate customers from regulatory constraints (e.g., closed-system applications, engineered dosing platforms).

Corporate development: Screen M&A targets through the lens of concentration (CR3/CR5 dynamics) and feedstock integration potential; prefer targets that accelerate margin capture or fill strategic geographic gaps.

Regulatory and compliance teams: Implement a tiered monitoring program aligned to the EPA’s registration review milestones and build contingency product label strategies to retain market access under restricted-use scenarios.

For leaders allocating capital and risk in 2026, the acrolein market rewards focused, risk-aware strategies: secure supply via structured partnerships, pursue downstream integration where it yields sustainable margin, and treat regulatory developments as a core input to portfolio prioritization. The market’s modest CAGR and concentrated supplier base argue against speculative, large-scale capacity bets; instead, favor surgical M&A, long-term offtakes with technical collaboration, and product differentiation that reduces exposure to open-environment regulatory restrictions.

PW Consulting’s full Acrolein Market report provides the complete datasets, scenario dashboards, and executable templates referenced above. For teams preparing 2026 procurement cycles, regulatory submissions, or corporate development pipelines, the study is designed to compress analysis timelines and provide a defensible basis for strategic choice. Contact our practice to access the full market model and to arrange a tailored briefing focused on your specific value chain position.

For detailed analysis of this topic, please visit the official page:Acrolein Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com