Inosine Pranobex Market — Strategic Briefing for 2026 Decisions

Executive teaser

PW Consulting’s latest Inosine Pranobex Market study (base year 2025) equips corporate leaders, BD teams, and investors with the actionable intelligence needed to make high‑conviction decisions in 2026. The report synthesizes historical performance (2020–2025) with a rigorous forecast to 2032, revealing a resilient market trajectory driven by steady clinical relevance, cost advantages, and diversified manufacturing footprints. While this briefing highlights the study’s strategic takeaways and competitive dynamics, the full report contains the granular region‑ and application‑level analytics, vendor scorecards, and pricing matrices that underpin our recommendations.

Inosine Pranobex Market

Market trajectory at a glance — what the headline numbers mean

Between 2020 and 2025 the Inosine Pranobex market expanded from an observed baseline to reach a 2025 market size of USD 215.0 Million (USD, revenue unit: Million). Our model projects continuation of this expansion through 2032, culminating in an estimated market size of USD 344.8 Million. This implies a compound annual growth rate (CAGR) of 6.98% over the forecast period 2026–2032 — a tempo that supports both organic product plays and selective inorganic moves.

Inosine Pranobex Market

Key interpretation points for 2026 planning:

Inosine Pranobex Market

- The mid‑single digit CAGR signals a market with durable demand and predictable expansion, suitable for scalable manufacturing investments and multi‑year commercialization plans.

- Historical growth from 2020 to 2025 demonstrates existing market adoption and price elasticity characteristics that favor low‑cost producers and differentiated combination products.

- Moderate market concentration (as captured in our study) indicates a fragmented supplier base — creating opportunities for consolidation, contract manufacturing relationships, and strategic alliances that can rapidly capture share.

What the full report delivers (practical, operational, and strategic components)

Our study is designed as an operational playbook rather than a purely academic forecast. Highlights include:

- Methodology and datasets — transparent modelling steps, input assumptions, and sensitivity runs so teams can adapt the forecast to internal scenarios.

- Commercial intelligence — validated pricing ranges, documented B2B transaction patterns across R&D to industrial volumes, and supplier capacity maps.

- Regulatory and clinical mapping — country‑level authorizations, an audit of active clinical studies, and a regulatory risk matrix focused on strategic markets.

- Go‑to‑market tools — channel economics, tender participation guidelines, and templates for cost plus and value‑based contracting in price‑sensitive markets.

- Supply chain and sourcing playbooks — supplier scorecards, contingency routing, and raw material hedging strategies calibrated for low‑margin APIs.

- M&A and partnership frameworks — valuation benchmarks, target screening filters, and integration risk checklists informed by market concentration metrics.

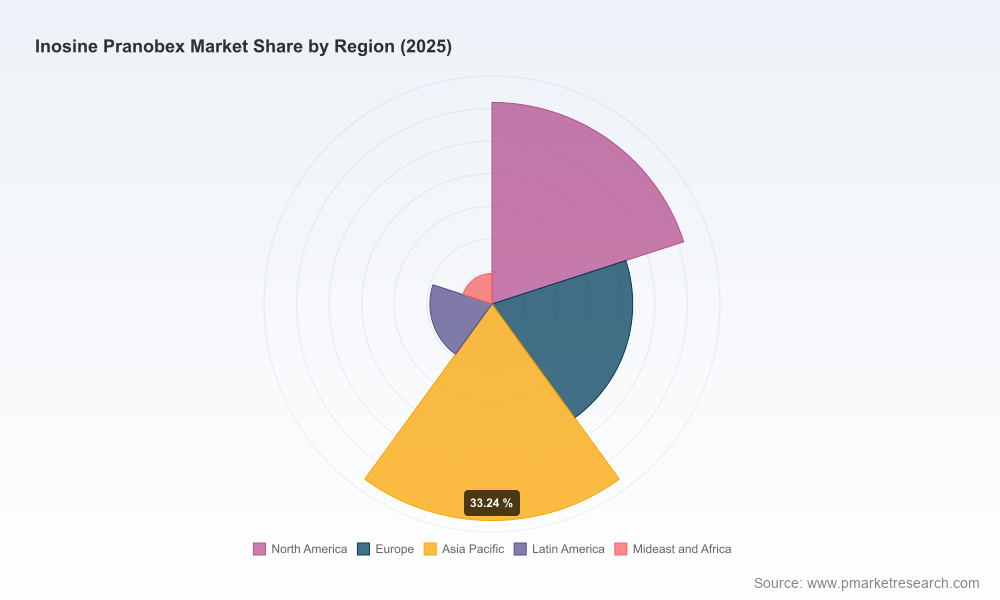

Note: detailed segmentation by region, application, and product type is deliberately reserved for the full report to preserve competitive differentiation and data provenance.

Competitive landscape — who to watch and why

The market is populated by a mix of originators, regional players, and specialized API manufacturers. Key participants covered in the research include established and regionally influential firms that collectively shape supply, quality standards, and commercialization strategy:

- Aflofarm (Poland) — a proactive product innovator that introduced a zinc‑combined formulation line in 2024, demonstrating demand for combination antiviral/immunomodulatory offerings and rapid label expansion through syrup and tablet forms.

- ICE Pharma (Italy) — a GMP API manufacturer with global‑grade dossiers (USDMF, CEP) and published product specifications; their dual‑jurisdiction manufacturing footprint supports supply diversity and regulatory traceability.

- Gedeon Richter, Newport Pharmaceuticals, Alfasigma, Polfarmex, Mochida, Yung Shin, Andrómaco, Sanfer, Meprofarm, Novell Pharmaceutical, and select Chinese API specialists — each contributes to global capacity, regional access, or formulation capability.

- Shandong Perfect Biotechnology and other API producers — important for price competition and scale, especially in markets where cost sensitivity drives procurement.

Recent corporate moves captured in our dataset underscore tactical behaviors you should expect in 2026: product line extensions into combination therapies, public availability of GMP API dossiers, and targeted regulatory clearances in national markets. These behaviors signal two concurrent strategies in the field — differentiation through formulation and consolidation through validated API supply.

Market dynamics and structural drivers

Our analysis identifies several structural drivers shaping market outcomes in 2026 and beyond:

- Regulatory heterogeneity — while Inosine Pranobex is authorized across numerous countries, notable regulatory gaps exist in major markets. The absence of certain regional approvals establishes both a barrier and an upside: companies that invest in pivotal trials and dossier assembly can unlock premium channels.

- Price sensitivity and reimbursement patterns — low manufacturing cost supports broad access in price‑conscious regions, fostering stable volume opportunities but compressing margins for commoditized supply.

- API procurement dynamics — documented transaction behavior shows distinct price bands aligned to order size (from R&D quantities to large industrial lots), and a finite set of high‑quality GMP suppliers. Buyers that secure long‑lead contracts or multi‑site sourcing reduce supply risk and gain negotiating leverage.

- Product innovation through combinations — Aflofarm’s 2024 launch exemplifies a rapid route to differentiation: combining Inosine Pranobex with adjunctive agents (e.g., zinc) to create new clinical positioning and patentable formulations.

Strategic playbook for executives entering 2026

For leadership teams preparing budgets and M&A targets in 2026, adopt a dual‑track approach: secure supply and pursue differentiated offerings. Our recommended actions:

- Supply security: Establish multi‑sourced API contracts with at least one GMP‑certified supplier holding international dossiers; prioritize capacity options in facilities with multi‑jurisdiction certifications.

- Commercial differentiation: Invest in combination formulations or delivery formats that deliver perceived clinical or convenience benefits; fast‑to‑market product extensions can command premium access in local formularies.

- Regulatory investment: Assess the ROI of pursuing approvals in higher‑barrier markets; selective regulatory dossiers tied to differentiated products tend to offer higher payback than generic entry.

- Cost and margin management: Use tiered pricing strategies and tender playbooks for price‑sensitive markets while protecting margin in specialty channels through value messaging and bundled contracts.

- M&A and partnerships: Target bolt‑on deals that add validated GMP API capacity, dossier completeness, or regional commercialization expertise; the market’s current fragmentation presents attractive roll‑up economics for disciplined acquirers.

Risk matrix and scenario planning

Critical risks to model in 2026 planning include regulatory reversals, concentrated supplier outages, and price erosion from increased low‑cost competition. Our scenario toolkit — included in the full report — evaluates four priority cases (base, accelerated commercialization, supplier shock, and regulatory tightening), with quantified impacts on revenue, margin, and required cash‑capex adjustments.

Why this research matters for 2026

With steady projected growth (CAGR 6.98% over 2026–2032) and a market environment characterized by both price sensitivity and pockets of premium opportunity, 2026 is a pivotal year for firms to lock in strategic advantages. Companies that move early to secure differentiated product positioning, diversify high‑quality API sources, and align regulatory investments with commercial pathways will convert a market that is stable but fragmented into a durable competitive moat.

Next steps — how to use our findings

PW Consulting recommends three immediate actions for 2026 planning cycles:

- Commission a short vendor due‑diligence sprint using our supplier scorecards to shortlist two primary API partners and one contingency source.

- Pilot one differentiated formulation (combination or novel dosage form) in a targeted low‑barrier market to validate price elasticity and label extensions before scaling dossiers to higher‑barrier regions.

- Integrate our scenario outputs into your FY‑2026 budget process to quantify capital allocation for regulatory filings, manufacturing scale‑up, and potential M&A activity.

For teams that require the full granular intelligence — including region‑ and application‑level splits, detailed pricing tables, supplier contracts, and step‑by‑step regulatory pathways — the complete PW Consulting Inosine Pranobex Market report contains the data and executable templates. Contact our research desk to obtain access and receive a tailored briefing for your corporate strategy session.

For detailed analysis of this topic, please visit the official page:Inosine Pranobex Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com