Biomedical 3D Printing Materials Market Sees Rapid Expansion in Implant Manufacturing

Health |

2026-05-28 13:59:34

As PW Consulting’s Senior Strategy Advisor and Head Industry Analyst, I present a concise, high-fidelity preview of our full Sealing Glass Market study. The sealing glass segment—critical to hermetic packaging, high-temperature fuel cells, advanced batteries, and next‑generation electronics—has transitioned from a niche materials play into a strategically important component layer for complex assemblies. This briefing outlines the market’s macro trajectory, competitive dynamics, regulatory and material drivers, and actionable implications for leadership teams planning their 2026 moves. Core segmented figures and granular vendor scorecards are intentionally withheld to preserve the report’s premium insights and to direct stakeholders to the full release for transaction‑grade intelligence.

Sealing Glass Market

Market scale and momentum: Using 2025 as the analytical base year, the global sealing glass market has demonstrated steady expansion from the early 2020s and reached a material inflection by 2024–2025. Our topline modeling pegs the market at a robust level in 2025 and forecasts consistent growth across the 2026–2032 horizon, culminating in a substantially larger market by 2032.

Sealing Glass Market

Compound growth profile: The market is projected to grow at a compounded annual growth rate (CAGR) of approximately 5.97% over the 2026–2032 forecast period. This rate reflects a blend of steady demand from electronics and semiconductors, accelerating adoption in energy applications (SOFCs and battery systems), and incremental gains from industrial and appliance segments.

Sealing Glass Market

Implication for strategy: A near‑6% CAGR implies that medium‑term investments in capacity, qualification, and supply resilience will pay off for producers and users alike. However, the growth is neither explosive nor static—planning must combine operational discipline with selective innovation bets.

Enabler of advanced assemblies: Sealing glass functions at the interface of materials science and systems engineering. Small shifts in formulation, coefficient of thermal expansion (CTE) matching, or melting profile can materially change yields for hermetic packages, SOFC stacks, or lithium battery seals.

Regulatory and sustainability constraints: Environmental mandates (e.g., RoHS-like restrictions) are accelerating the shift to Pb‑free and PbO‑free glass chemistries in many electronics and defense applications. Companies that fail to anticipate regulatory timelines face requalification costs and lost addressable opportunity windows.

Supply risk and raw material exposure: Certain glass formulations depend on specialty feedstocks and tailored oxides. Combined with a concentrated supplier base and multi-month qualification cycles, procurement strategies must prioritize multi‑sourcing, supplier development, and inventory hedging.

Market sizing and forecast model: Complete historical series and a transparent, scenario‑based projection for 2026–2032; downloadable model with sensitivity levers for price, demand, and substitution.

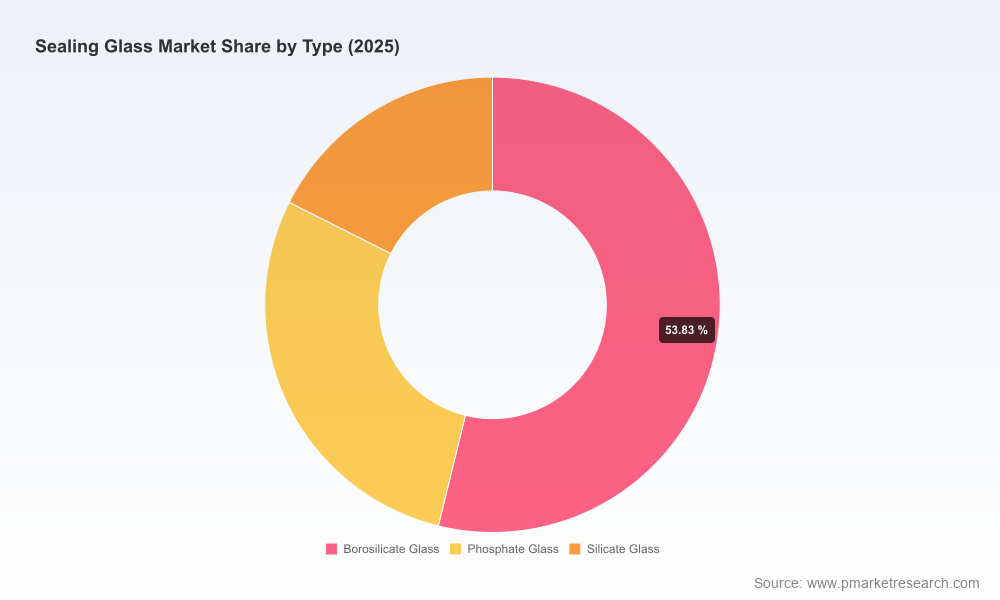

Technology and formulation mapping: Side‑by‑side evaluation of borosilicate, phosphate, silicate, and glass‑ceramic approaches; guidance on selecting glass families based on CTE compatibility, melting windows, and crystallization resistance.

Use‑case diagnostics: Failure‑mode analysis and qualification roadmaps for LED/OLED encapsulation, semiconductor hermetics, SOFC interfaces, and battery sealing—each with recommended test protocols and acceptance gates.

Regulatory and compliance matrix: Jurisdictional timelines for hazardous substance restrictions, recommended documentation for customer qualification, and templates for supplier declarations.

Supplier and vendor intelligence: Vendor scorecards, product positioning, capacity maps, and strategic partnership opportunities—presented without publishing sensitive contract terms.

Commercial playbook: Pricing benchmarks, margin archetypes, go‑to‑market options for specialty formulators, and M&A diligence checklists for targets in the sealing glass value chain.

Practical deliverables: Excel‑based TCO calculators, qualification checklists, and a library of recommended mechanical and environmental tests that procurement, quality, and R&D teams can deploy immediately.

Mo‑Sci, LLC (Rolla, Missouri): A specialty glass innovator focused on high‑temperature and viscous sealing glasses. Mo‑Sci’s product architecture emphasizes high‑reliability SOFC seals, sodium‑ion battery interfaces, and customizable CTE formulations. Their recent Sealing Glass Selector Guide (January 2026) added multiple GL‑series formulations targeted at alumina, YSZ and metal interfaces—an indication of continued investment in application‑specific datasheets to shorten customer qualification cycles.

Elan Technology (Roswell, Georgia): Positioned as a supplier of hermetic sealing glasses and composite preforms, Elan has been expanding into lithium battery sealing and LAS ceramic‑glass composites. The January 2026 materials expansion highlights a strategy to serve adjacent electrification markets that require matched mechanical and thermal behavior.

Nippon Electric Glass (Otsu, Shiga): Longstanding specialist in low‑temperature sealing glasses for devices such as quartz oscillators and SMD packages. Their portfolio emphasizes precise sealing temperatures and substrate compatibility—attributes that matter for high‑yield semiconductor packaging and MEMS hermetics.

SCHOTT AG (Mainz): A leader in high‑purity, high‑temperature sealing solutions—offering frits, pastes, sintered preforms, and green sheet formats. SCHOTT’s 130+ year expertise and broad product form factors make it a default choice for extreme‑heat and high‑reliability applications like SOFC and industrial flash lamps.

AGC Inc. (Tokyo): Supplies Pb‑free sealing glass powders, pastes, and frits for semiconductor packaging and MEMS applications, stressing corrosion and moisture resistance. AGC’s catalog highlights practical, regulation‑ready options for customers migrating away from Pb‑containing chemistries.

Market concentration signals are noteworthy: the top three suppliers account for a majority share of the market, and the top five approach nearly seven in ten of market revenues—indicative of a moderately concentrated industry where scale and technical IP confer durable advantages. For buyers, this dynamic creates negotiation leverage but also underscores the importance of supplier risk mitigation.

Lead‑free transitions are non‑negotiable in many electronics segments. Several suppliers now explicitly offer Pb‑free and PbO‑free formulations to comply with RoHS and similar standards—this is a baseline requirement rather than a differentiator for Tier‑1 suppliers.

Qualification temperature windows matter. Low‑temperature sealing glasses designed to process below key solder reflow thresholds enable integration into SMD workflows, while ultra‑high‑temperature, alkali‑free glasses are engineered for SOFC stacks and other environments up to and beyond 1,600°C.

Form factor diversity: Vendors provide powders, pastes, preforms, and green sheets. Selection determines upstream handling, dispensing equipment, and thermal processing investments—decisions that should be made in tandem with procurement and process engineering.

Prioritize qualification pipelines: Start qualification of Pb‑free and low‑temperature formulations in H1 2026 to meet product launch windows in 2027–2028. Leverage supplier labs for co‑development to compress qualification lead times.

Adopt a dual‑track supplier strategy: Balance one scaled, incumbent supplier for volume and one agile specialist for innovation. This reduces single‑source exposure while preserving access to bespoke chemistries.

Embed regulatory foresight into product roadmaps: Map RoHS‑equivalents across target markets and bake declarative documentation into supplier contracts to avoid requalification costs later in the product lifecycle.

Invest in materials characterization: Allocate modest central R&D resources to CTE mapping, wetability testing, and long‑term moisture/corrosion aging. These tests often uncover substitution risks before they surface in the field.

Use M&A and partnerships tactically: Given the market’s moderate concentration, bolt‑on acquisitions in specialty chemistries or strategic long‑term supply agreements can create defendable advantages for OEMs seeking vertical control.

This preview highlights the strategic contours that will matter for corporate decision‑makers in 2026. PW Consulting’s full Sealing Glass Market report includes the proprietary datasets, vendor scorecards, and the transaction‑grade models required to execute on the recommendations above. If your team is evaluating supplier strategy, entering an adjacent application, or assessing acquisition targets, our full study provides the validated inputs and tactical playbooks to reduce risk and accelerate time to value.

To access the complete report, detailed segmentation, and downloadable tools—including the interactive forecast model—visit our official release page or contact your PW Consulting account lead. The in‑depth intelligence we provide is designed to convert material science insights into boardroom‑level decisions and measurable commercial outcomes.

For detailed analysis of this topic, please visit the official page:Sealing Glass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com