Machine Tool Bearing Market — Strategic Imperatives for 2026

As global machine tool builders, spindle integrators, and precision-component OEMs position for the next wave of automation and multi-process machining, bearings remain a high-leverage element of competitive advantage. This briefing previews PW Consulting’s 2026 Machine Tool Bearing Market research: it surfaces the macro trajectory, competitive dynamics, regulatory and raw-material headwinds, and the concrete decision levers that executives must act on in 2026. In keeping with our “trailer” principle, we demonstrate analytical depth and actionable frameworks while reserving granular segment tables and proprietary vendor scorecards for the full report.

Machine Tool Bearing Market

Why this study matters for 2026 decision cycles

- Capital allocation: Clarifies where to prioritize spindle and axis investments given expected market growth and technology adoption curves.

- Product strategy: Informs R&D trade-offs between super-precision, hybrid, and air-bearing approaches for new machine families.

- Supply chain & procurement: Highlights sourcing and hedging strategies to mitigate steel-price exposure and single-supplier risk.

- Aftermarket & service models: Quantifies the economic opportunity in retrofits, predictive maintenance, and life-extension services.

- M&A and partnerships: Provides a focused lens on targets whose technology or footprint accelerates customers’ time-to-market.

Market at a glance — macro trajectory and what it implies

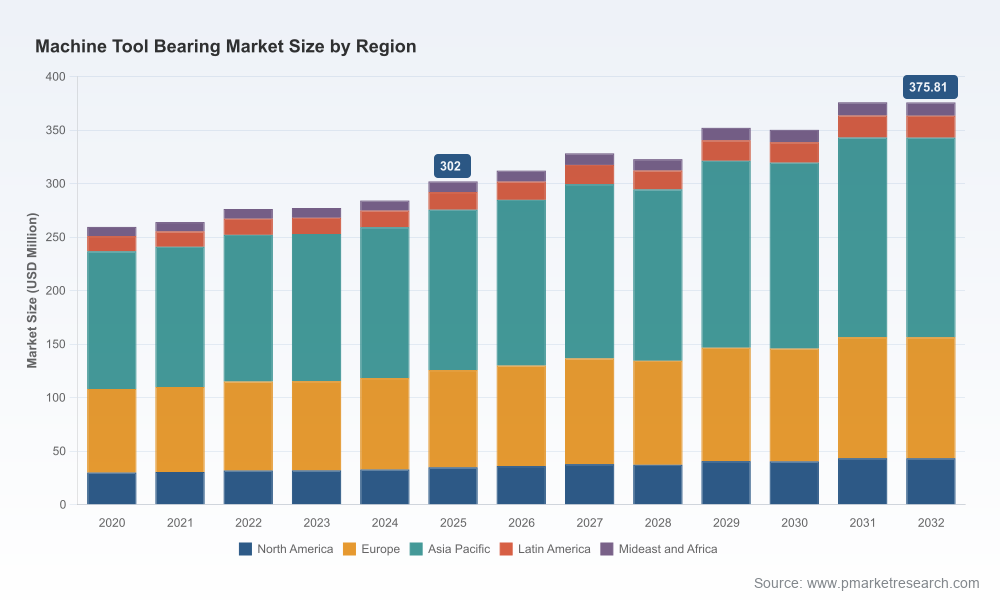

Our base year is 2025. Between 2020 and 2025 the market demonstrated resilience, recovering from early-decade dislocations and moving into a steady expansion phase. In 2025 the market reached an inflection that sets a new baseline for strategic planning. For the forecast window (2026–2032) PW Consulting projects a compound annual growth rate (CAGR) of 3.2%. The trajectory shows moderate growth with episodic volatility tied to capex cycles, customer mix shifts, and raw-material swings.

Machine Tool Bearing Market

Three implications follow for 2026 planning horizons: first, buyers and OEMs should expect steady but non-linear growth—enough to justify targeted investments in higher-performance spindles and automation-enabled systems. Second, discretionary R&D and tooling budgets should be prioritized around technologies that deliver measurable productivity and lifecycle cost advantages. Third, suppliers that can combine product performance with resilient, low-cost supply chains will capture outsized share.

Machine Tool Bearing Market

Key dynamics and systemic risks

- Technology adoption: Automation and multi-process machining continue to push demand toward higher-speed, higher-accuracy bearing solutions and integrated linear technologies. Leading suppliers are responding with specialized angular-contact bearings, hybrid lubrication systems, and linear guideway assemblies tailored to automated axes.

- Standards & compliance: New normative updates (e.g., standards affecting life calculation and machine safety) are compressing lead times for qualification and require earlier engagement between bearing engineers and machine-system integrators.

- Raw-material pressure: A meaningful share of manufacturers report margin pressure from fluctuating precision-steel prices. Procurement strategies that combine hedging, supplier diversification, and design-for-cost are now core capabilities.

- Market concentration: The sector shows a moderate level of consolidation among tier‑one suppliers, creating both competitive intensity and opportunity for differentiated niche players that can offer ultra‑precision, aftermarket services, or cost-competitive scale.

Competitive landscape — reading leader moves

The landscape is characterized by incumbent precision-engineering specialists and a cohort of regional players focused on cost and local service. Across this field several strategic plays are visible:

- Product-depth differentiation — incumbents with legacy expertise in super-precision bearings continue to invest in spindle-centric solutions focused on minimizing vibration, thermal growth, and noise while maximizing rotational accuracy. These firms defend margins through deep application know-how and close design-in partnerships with OEMs.

- High-speed and hybrid solutions — a set of suppliers is advancing hybrid lubrication and air-bearing technologies to improve dynamic stability in high-RPM spindles and axes. These technologies are becoming decision criteria for machine designs aimed at high-value, high-speed metalworking.

- System integration and linearization — a subset of players is extending beyond rolling elements into linear guides, rotary tables, and hybrid screw drives to capture more of the machine’s bill of materials and lock in long-term service relationships.

- Aftermarket & service monetization — leading vendors are formalizing predictive-maintenance offerings, condition-monitoring kits, and refurbishment programs that increase lifetime revenue per unit and reduce end-customer total cost of ownership.

Representative vendor positions (selected leaders) illustrate these plays: some firms emphasize super‑precision spindle bearings designed to minimize noise and thermal drift; others showcase ultra-high-speed, high-load angular-contact bearings and advanced cage technologies targeted at heavy cutting; a few focus on hybrid and air-bearing approaches for dynamic stability. Several showcased product innovations at major trade events in 2025 that confirm the strategic direction—particularly investments focused on driven tool bearings, hybrid screw drives, and high-speed cage designs.

What the PW Consulting report delivers — practical, executable outputs

- Market model and scenarios — top-down and bottom-up forecasts (base year 2025; historical 2020–2025; forecast 2026–2032) with sensitivity analyses for capex shocks and raw-material volatility.

- Decision frameworks — capital-prioritization matrices, product-roadmap scoring, and a 90‑day procurement playbook for hedging steel exposure and securing precision-grade inputs.

- Commercial enablement — go-to-market playbooks tailored to spindle OEMs, retrofit specialists, and aftermarket channels, including value-pricing templates and service-bundle economics.

- Supplier & M&A diagnostics — shortlists of strategic targets by technology gap, footprint, and integration risk; acquirer‑ready due‑diligence checklists and synergy capture estimates.

- Engineering-to-cost (E2C) tools — lifecycle cost calculators for bearings in spindle and axis applications, failure-mode economic impact matrices, and testing/validation roadmaps mapped to recent standards.

- Customizable dashboards — KPI sets for production, quality, and aftermarket performance that can be deployed in executive presentations and investor materials.

Note: The full report contains granular segment breakdowns, region and application tables, and vendor scorecards. Those details are intentionally omitted here to preserve the strategic discovery arc and to encourage direct engagement with PW Consulting for the complete dataset and models.

A 2026 decision playbook — seven high‑impact moves

- Rebase R&D priorities on lifecycle value: Shift discretionary spend toward bearing technologies whose lifecycle cost savings offset incremental unit cost within three years.

- Lock early-stage supplier agreements: Secure multi-year supply agreements with tier‑one steel and component suppliers with indexation clauses to stabilize margin exposure.

- Invest in modular spindle architectures: Standardize on modular interfaces that allow OEMs to upsell higher-performance bearing modules as options.

- Monetize aftermarket sooner: Pilot predictive-maintenance subscriptions on a representative machine park to prove ARR economics and capture service margin uplift.

- Target inorganic options selectively: Pursue bolt-on acquisitions that deliver either a technological leap (e.g., air-bearing competence) or immediate aftermarket access.

- Operationalize standards readiness: Embed new life‑calculation and safety standards into procurement and qualification gates to avoid late-stage redesigns.

- Stress-test scenarios quarterly: Use the report’s scenario engine to re-evaluate priorities against steel-price swings, demand shifts in automation, and regional capex patterns.

How PW Consulting’s research adds strategic value to your 2026 planning

This study translates a complex field of incremental innovations and cyclical demand into prioritized, executable options. For executives, the value is threefold: (1) conviction in where to place bets across product and geographic plays; (2) tools to translate market movement into contract, sourcing, and R&D actions; and (3) a clear path from insight to execution via vendor scorecards, cost models, and M&A shortlists that are ready to be actioned in 2026.

Next steps — accessing the full intelligence

If your 2026 strategy depends on precise segment economics, vendor comparative matrices, or scenario-ready models, the full Machine Tool Bearing Market report contains those deliverables along with downloadable datasets and board-ready slides. PW Consulting can also run a tailored workshop to map these insights directly into your product roadmap, procurement strategy, or M&A pipeline.

Contact PW Consulting to obtain the complete report and schedule a strategic briefing—our advisory team will walk you through the full datasets, vendor scorecards, and operational playbooks necessary to convert 2026 uncertainty into competitive advantage.

For detailed analysis of this topic, please visit the official page:Machine Tool Bearing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com