Forged Steel Grinding Balls Market — Strategic Outlook for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused, decision-centric briefing on the forged steel grinding balls market designed to align executive choices in 2026 with the most consequential market forces. This preview synthesizes our full market study (base year 2025) to show why buyers, OEMs, and investors must act now — and where they should concentrate scarce strategic bandwidth. The full report contains the granular segmentation, supplier scorecards, price-sensitivity models and interactive scenario tools that procurement and strategy teams will need to operationalize these findings.

Forged Steel Grinding Balls Market

Executive snapshot: trajectory and scale

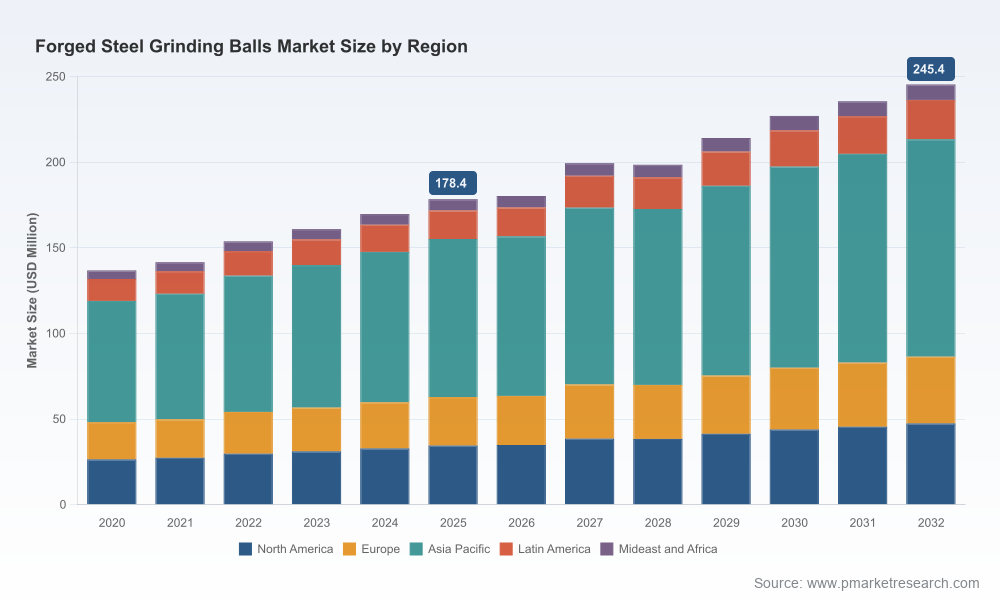

The forged steel grinding balls market has moved steadily from a modest post‑pandemic recovery into a structurally growing subsector. Historical industry revenue climbed from approximately USD 137 million in 2020 to about USD 178 million by the 2025 base year. Our forecast shows continued expansion over the 2026–2032 horizon at a compound annual growth rate (CAGR) of roughly 4.8%, reaching an anticipated market size in excess of USD 245 million by 2032.

Forged Steel Grinding Balls Market

Those headline figures mask important inflection points: demand for high-performance forged media is being reshaped by commodity cycle investment (notably copper and gold projects), by shifting trade and regulatory pressures, and by rising emphasis on operational resilience within mill circuits. The next 12–18 months will be decisive in separating firms that secure differentiated supply positions from those that remain exposed to cost volatility and regulatory disruption.

Forged Steel Grinding Balls Market

Why this matters to executives in 2026

- Procurement resilience: Forged grinding media is not a simple commodity; scrap steel and ferroalloy inputs represent a material share of production cost (our sector analysis estimates this exposure in the mid‑range of industry norms). Volatility in these feedstocks creates earnings and service-level risk unless addressed through proactive sourcing and hedging strategies.

- Operational uptime & mill efficiency: Higher‑quality forged balls reduce breakage, decrease mill downtime and improve throughput for large SAG/ball mill circuits. For mining and cement operators, media selection now directly affects unit cost of production and project payback timelines.

- Trade and compliance planning: New anti‑dumping investigations initiated early in 2026 have re‑ranked trade risk for players reliant on specific supply corridors. Strategic sourcing must therefore incorporate tariff, compliance and nearshoring scenarios into capital and inventory planning.

- Competitive positioning: Suppliers able to offer technical support, local stocking, and product validation are capturing premium revenue pools; buyers should mirror that capability in their supplier governance models.

Market structure and competitive dynamics

The market displays a mixed structure: global established players coexist with regional specialists that leverage proximity to end users and low logistics lead times. Leading global engineering and media manufacturers continue to broaden product portfolios and service capabilities to target high‑value comminution segments.

- ME Elecmetal (United States): A long‑standing supplier with engineering depth around SAG, ball and rod mill media and a reputation for technical service and mill‑circuit optimization.

- Molycop (Australia): Focused on high‑carbon alloy forged and SAG balls with recent capacity moves to serve regional demand directly; active in trade shows and industry dialogues on comminution optimization.

- Magotteaux (Belgium): Offers a wide range of forged and cast media including chromium‑alloy variants; positions itself on metallurgical design and alloys science.

- GSI Lucchini (Italy): Premium forged media supplier that emphasizes custom forging and metallurgical controls for mining and mineral processing.

- Energosteel (Ukraine): Expanding European warehouse footprint to simplify imports and improve lead times for buyers in the EU market.

- Grinding Media South Africa: Regional specialist for southern African markets and select industrial sectors, focusing on high‑chrome options for specific ore types.

Recent supplier activity through 2025–2026 illustrates strategic priorities: capacity extension in Southeast Asia, EU‑facing warehousing to bypass logistics friction, and active engagement at major mining exhibitions to validate product claims and secure offtakes. These moves collectively point to higher investments in service and logistics as key differentiators beyond metallurgical capability.

Key dynamics shaping 2026 decisions

- Raw material cost volatility: Scrap and ferroalloy inputs account for a dominant portion of production costs (sector estimates indicate this is a majority share). Buyers and producers that align procurement horizons, indexation mechanisms and inventory buffers will reduce margin and service risk.

- Regulatory and trade shocks: Anti‑dumping measures and trade investigations launched in early 2026 have already altered freight flows and sourcing economics for several buyers. Risk mitigation requires rapid legal, customs and supply‑chain scenario planning.

- Commodity capex: New mining projects in Latin America and Africa continue to lift long‑term demand for forged media in large SAG and ball mills. Project owners and EPC contractors should incorporate media lifecycle cost into early engineering to avoid late‑stage cost surprises.

- Environmental and safety drivers: Tighter standards in mining and cement sectors favor products with superior impact toughness and lower fragmentation. This both increases demand for higher‑spec forged items and raises the bar for supplier qualification.

Strategic implications by function

- Procurement & supply chain: Move from transactional buying toward supplier partnerships with shared price mechanisms, joint inventory strategies, and performance‑linked contracts. Nearshoring and regional warehousing reduce exposure to sudden trade measures and freight volatility.

- Operations & maintenance: Shift specification focus from simple unit price to lifecycle cost: breakage rate, mill performance uplift, and replacement frequency. Pilot test programs and in‑situ metallurgical validation should be a standard part of qualification.

- Commercial & finance: Model multiple pricing and tariff scenarios into three‑year budgets. Capital allocation for mine projects should reflect the incremental operating benefits of higher‑performance media when calculating IRR and payback.

- Risk & compliance: Integrate anti‑dumping and customs risk into supplier scorecards. Legal exposure and potential retroactive duties can be material to total landed cost if not proactively managed.

Report deliverables (practical, executable)

Our full PW Consulting market study provides a suite of operational tools designed for immediate use by 2026 decision-makers, including:

- Actionable procurement playbooks that convert metallurgical specifications into commercial terms, recommended contract clauses, and inventory hedging approaches.

- Supplier evaluation and scorecard templates that combine technical performance, logistics resilience, and trade‑risk exposure.

- Scenario models for raw material price stress-testing and tariff event simulations to quantify landed cost sensitivity across multiple regions.

- Operational case studies showing how incremental reductions in media breakage translate into mill throughput, energy consumption and unit cost improvements.

- Roadmaps for nearshoring and regional warehousing, including decision criteria and phased implementation templates.

To respect the “trailer” principle of this briefing, we present strategic intent and practical outputs while withholding detailed regional and application splits, granular supplier financials and the full set of model inputs — these are available in the complete report and the interactive data workbook that accompanies it.

Risk register and mitigation priorities

Key risks that should be actively managed in 2026 include:

- Feedstock price shocks: Mitigate through multi‑tier suppliers, indexed price mechanisms, and strategic stockpiles where capex and working capital allow.

- Trade & tariff volatility: Engage customs counsel and consider alternative routing, bonded warehousing, and re‑routing of shipments to neutral jurisdictions.

- Supplier concentration: While the market includes several global leaders, concentration metrics indicate substantial room for regional specialists. Diversify to balance lead‑time and cost objectives.

- Technological obsolescence: Maintain active R&D engagement with key suppliers to ensure alloy developments and heat‑treatment advances are accessible to your operations.

How to use this research in 90 / 180 / 360 day plans

- 90 days: Map current supply exposures, identify single‑sourced items, and initiate supplier qualification audits for at‑risk categories.

- 180 days: Negotiate short‑term contracts with hybrid price mechanisms, pilot a nearshore warehousing proof‑of‑concept, and roll out a supplier scorecard process for all major contracts.

- 360 days: Implement optimized sourcing lanes, finalize strategic supplier alliances with shared inventory and performance targets, and embed media lifecycle costing into capex approvals and operational KPIs.

Conclusion — the strategic opportunity

The forged steel grinding balls market is neither static nor purely commoditized. Growth at a roughly 4.8% CAGR, combined with shifting trade, raw material volatility, and rising performance expectations, creates a window for buyers and suppliers to lock in differentiated economics through better design‑to‑supply strategies. Companies that align procurement, operations and risk management will convert market dynamics into sustainable cost and throughput advantages.

PW Consulting’s full report provides the data, models and executable templates to make those decisions with confidence. For access to the complete dataset, supplier scorecards, and the scenario workbook required to operationalize these recommendations, please consult the source page accompanying this briefing.

For detailed analysis of this topic, please visit the official page:Forged Steel Grinding Balls Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com