Metal Ceilings Market 2026: Strategic Preview for Corporate Decision-Makers

PW Consulting presents a forward-looking strategic primer on the global Metal Ceilings market, designed as an executive-level navigation tool for 2026 decision cycles. This overview synthesizes market trajectory, structural forces and competitive dynamics to enable rapid prioritization of investments, procurement changes, and product development pathways. The full market study contains exhaustive segment tables, regional breakouts and modelled scenarios; this introduction surfaces the high-value implications while intentionally withholding the granular segment matrices to encourage direct access to the full report for transactional planning.

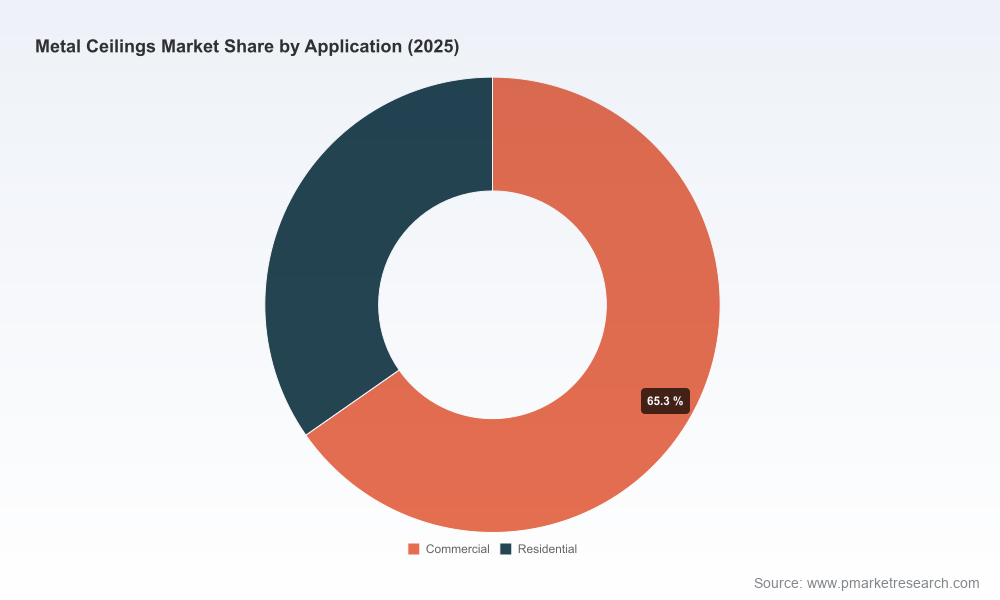

Metal Ceilings Market

Market at a glance — trajectory and scale

The Metal Ceilings market has demonstrated steady expansion through the early 2020s. Using 2025 as the study base year, PW Consulting tracked the market from 2020–2025 and projects through a 2026–2032 forecast horizon. The market grew from roughly USD 2.6 billion (2020) to around USD 3.35 billion (2025) and our model anticipates continued growth toward the mid-decade and beyond — approaching the upper end of the USD 4.5+ billion range by 2032. These projections rest on a base-case compound annual growth rate (CAGR) of approximately 4.5% across the 2026–2032 period.

Metal Ceilings Market

For executives, the takeaway is straightforward: demand is durable and expanding at a stable mid-single-digit pace, creating windows for incremental capacity expansion, targeted product innovation, and consolidation plays — but not a runaway boom that eliminates the need for disciplined capital allocation.

Metal Ceilings Market

Key market dynamics shaping 2026 choices

- Specification-led demand: Institutional and commercial building specifications continue to drive architectural metal ceiling uptake, especially where acoustic performance, durability and bespoke aesthetics are mandated. Updated technical guidance and new application-specific coverage (see regulatory note below) are increasing the role of early-stage specification capture in procurement strategies.

- Supply-chain and raw-material pressure: Metals markets remain a background risk. In 2025, US iron ore production softened markedly and global unit costs for imported iron ore fines averaged near USD 99/ton in recent reporting. These input dynamics translate into episodic margin pressure or the need for quarterly price pass-through clauses for manufacturers and distributors.

- Regulatory and standards signals: Industry standards bodies have refreshed guidance relevant to metal ceilings. Notably, updated CISCA (Ceilings and Interior Systems Construction Association) materials now incorporate dedicated treatment for metal security ceilings and other challenging applications — elevating specification thresholds for many public and commercial projects.

- Product differentiation via sustainability and acoustics: Leading manufacturers are investing in eco-certification, circular-design claims and acoustic engineering as route-to-spec advantage. Sustainability credentials (e.g., Cradle to Cradle) and transparent lifecycle data are increasingly decisive for large architectural and institutional buyers.

- Fragmented competitive structure: Market concentration remains relatively low by heavy-industrial standards. The three largest firms command under one-third of market share while the top five accumulate a little over one-third — a structure that preserves room for regional specialists, artisanal producers and targeted entrants to win project-level business.

What PW Consulting’s full report delivers (operationally oriented)

- Market sizing and validated growth scenarios (base, upside, downside) with transparent assumptions for raw materials, construction activity and specification adoption.

- Go-to-market playbooks for manufacturers, distributors and architectural reps: pricing levers, spec-capture tactics, channel economics and digital sales frameworks.

- Competitive landscaping and handshake maps: audited supplier capabilities, manufacturing footprints and win-loss archetypes for major contract types (new build, retrofit, restoration).

- Procurement and supplier risk toolkit: hedging templates, indexation clause examples, supplier scorecards and contingency sourcing routes for metal inputs.

- Product development roadmaps: acoustic and sustainability packaging, modularity standards, prefabrication approaches for cost-to-install reduction.

- M&A and partnership heatmaps: valuation benchmarks, potential bolt-on targets, and integration playbooks focused on route-to-spec acceleration.

- Spec-ready resources for architects and engineers: sample specification language, installation checklists and performance-testing protocols aligned with the latest industry guidance.

Each deliverable is built to be actionable for 90–180 day decision cycles while preserving deeper modelling and primary research reserved for subscribers.

Competitive landscape — who matters and why

The market is populated by a mixture of multinational systems players, specialist architectural manufacturers, and established regional artisans. Key players included in our competitive analysis are:

- Lindner Group (Germany) — recognized for suspended and perforated systems and a strong push on certified sustainable solutions and acoustic integration. See: https://www.lindner-group.com

- Rockfon (Finland) — a systems player that combines ceiling panels with suspension grids to offer full-system acoustic solutions. See: https://www.rockfon.com

- Armstrong World Industries (United States) — broad commercial portfolio including specialty faux-metal aesthetics that target large commercial and retrofit projects. See: https://www.armstrongceilings.com

- USG Corporation (United States) — integrated ceiling systems with strong distribution channels into contractor communities. See: https://www.usg.com

- Hunter Douglas Architectural (Netherlands) — innovator in multipanel and suspended aluminum systems, with cross-market product families. See: https://www.hunterdouglasarchitectural.com

- Specialist and artisan suppliers (US-based family manufacturers and China-based system producers) — firms such as Shanko Tin Ceilings, Metal Ceiling Express, Chelsea Decorative and TBK Metal occupy important niches where authenticity, restoration capability or low-cost custom production are decisive. See company sites referenced in the full report for profiles and capability maps.

Our analysis shows that the market rewards two distinct strategic postures: system-integrators that capture specification capture earlier in the design cycle, and specialist producers that maintain margin resilience through unique manufacturing capability or bespoke authenticity. The relatively modest CR3/CR5 concentration metrics underline why both postures remain viable concurrently.

Recent corporate moves and signals

- Specification leadership: In January 2026, an established pressed-metal manufacturer published an updated architect specification guide aimed at hospitality and restoration projects — an example of how specification assets are being weaponized to win high-value, design-led contracts.

- Industrial modernization and export of production lines: Late-2025 deliveries of custom production machinery to multiple European factories highlight a parallel cycle of capacity modernization among mid-sized producers, enabling faster turnaround for custom lines and geographic diversification of output.

Strategic implications and recommended actions for 2026

For executive teams preparing 2026 budgets and three-year strategic plans, PW Consulting recommends prioritizing five actions that convert market growth into competitive advantage:

- Lock specification capture early: Invest in architect- and specifier-focused resources (dedicated technical reps, specification libraries, BIM families and acoustic/lifecycle case studies). Early capture reduces tender volatility and supports premium positioning.

- Hedge input risk pragmatically: Adopt a tiered procurement strategy with a mix of long-term supplier agreements, indexed pass-through clauses and a secondary sourcing program. Run stress tests in your internal P&L models using metal-price scenarios tied to recent iron-ore supply shifts.

- Differentiate on certified sustainability and acoustic performance: Certifications and documented lifecycle benefits are increasingly required by institutional buyers. Target investments that deliver measurable LCA improvements and acoustic metrics that can be embedded into spec documents.

- Rationalize manufacturing footprint with customer proximity in mind: The market’s steady growth favors selective nearshoring for lead-time sensitive product lines and centralized fabrication for high-volume modular systems. Use the report’s manufacturing heatmaps to size dual-sourcing options by corridor.

- Be deliberate about M&A and partnerships: With modest concentration, tuck-ins that add specification channels, finishing capability or unique dies can move the needle. Prioritize targets that bring design-engineering talent or specification channels rather than pure volume alone.

Short-term KPIs to track performance in 2026 include specification-share in priority metropolitan markets, order lead-time trends, input-cost pass-through effectiveness, and percent of revenue from certified/sustainability-labelled SKUs.

Why this matters right now

Leadership choices made in 2026 will determine whether firms capture the rising value embedded in specification-sensitive projects and sustainability-driven procurement or remain exposed to episodic margin squeeze from raw-material swings. The market’s stable mid-single-digit growth profile rewards strategic discipline: targeted investments, specification-play wins and pragmatic supply-chain resilience.

Next steps — where to find the intelligence you need

PW Consulting’s full Metal Ceilings Market report contains the underlying segment tables, regional splits, supplier scorecards and model workpapers needed to operationalize the recommendations above. For procurement teams, product leaders and corporate development executives preparing 2026 action plans, the full study supplies the actionable detail that complements this strategic primer.

Contact PW Consulting to obtain the complete report and the accompanying scenario models that will let you stress-test your 2026 investments against alternative raw-material and specification adoption pathways.

For detailed analysis of this topic, please visit the official page:Metal Ceilings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com