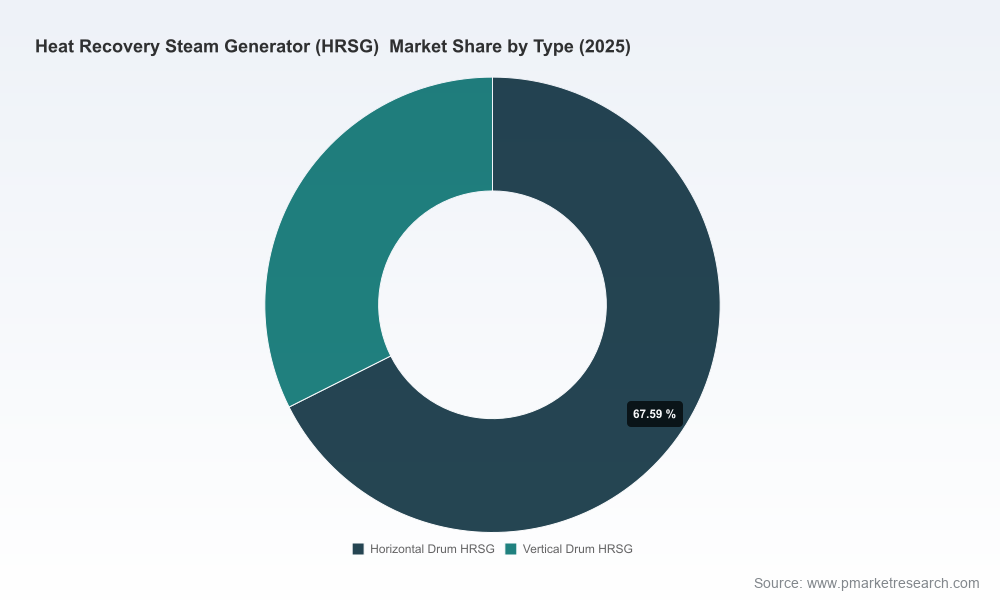

Heat Recovery Steam Generator (HRSG) Market — Strategic Primer for 2026 Decision Makers

Executive snapshot

As organizations plan capex, asset transitions and service strategies in 2026, the HRSG market is in a sustained expansion phase that demands differentiated strategic responses. PW Consulting’s latest study (base year 2025, historical window 2020–2025, forecast 2026–2032) projects a multi-year recovery and growth trajectory with a compound annual growth rate (CAGR) of 5.7% across the forecast window. The global market value, measured in USD million, has roughly doubled from the early-2020s and is projected to continue climbing into the early 2030s. Market concentration remains moderate: the three largest suppliers account for just over one-third of market share (CR3 ≈ 35.2%), while the top five capture under half (CR5 ≈ 48.7%).

Heat Recovery Steam Generator (HRSG) Market

Why this research matters to 2026 strategy

- Timing: 2026 is a decision inflection point for asset owners and OEMs—many combined-cycle and cogeneration projects contracted earlier in the decade will enter execution and retrofit phases now. Understanding near-term demand velocity is critical for supply-chain planning and resource allocation.

- Investment prioritization: Our analysis translates macro growth into actionable priorities for manufacturing capacity, spares inventory, and aftermarket service deployment without exposing confidential segment-level prescriptions.

- Risk-weighted scenarios: The report provides scenario outputs that show how regulatory shifts, subsidy flows, and commodity-price shocks materially alter project economics and order books through 2032.

Market trajectory and what it implies

The market moves we observed from 2020 through the 2025 base year map to a clear structural uptick entering 2026. After a period of volatile OEM ordering and deferred maintenance in some regions, capital is reflowing into combined-cycle modernization and industrial heat-recovery projects. The forecast to 2032 factors in decarbonization policy pathways, merchant power economics, and rising interest in modular combined-cycle solutions. For buyers and suppliers alike, this translates into three practical implications: 1) booking and execution cadence will be uneven across project types, 2) aftermarket and retrofit services become a larger, margin-stable revenue stream, and 3) supply-chain resilience (especially for high-grade alloys and pressure-part fabrication) is a strategic differentiator.

Heat Recovery Steam Generator (HRSG) Market

Key dynamics reshaping demand

- Regulatory and subsidy signals: New and evolving incentive programs are accelerating specific heat-recovery deployments. Examples include Japan’s 2025 subsidy initiatives to reduce renewable-heat and waste-heat costs and European taxonomy rules that change the sustainability calculus for gas-based combined-cycle assets. Such policy drivers materially change project bankability and timeline urgency.

- Fuel and transition economics: Coal-to-gas switching and integration of hydrogen-blended fuels in some fleets create opportunities for HRSG specifications that can tolerate variable exhaust profiles and higher temperature differentials. Strategy must therefore bridge near-term conversions and longer-term fuel-flexibility requirements.

- Modularity and plant architecture: Modular combined-cycle modules and factory-as-assembly approaches compress schedule risk and favor suppliers with repeatable, transportable designs and proven field constructability approaches.

- Materials and manufacturing: High-grade alloys and controlled in-house manufacturing of pressure parts are non-negotiable for reliability in high-temperature/high-pressure applications. OEMs with vertical manufacturing capabilities demonstrate lower execution risk for critical modules.

- Aftermarket economics: Mature markets will increasingly monetize life-extension, inlet-duct, and liner modernization work. Service contracts, condition-based maintenance, and retrofit bundles are central to long-term margin profiles.

Competitive landscape — strategic positioning and implications

The competitive set is a mix of large, integrated OEMs and specialist fabricators/services providers. Across this spectrum, differentiation hinges on three vectors: engineering pedigree (design options and thermodynamic optimization), manufacturing footprint (localization, alloy capability, and size limits), and aftermarket services (inspection, repair, modernization).

Heat Recovery Steam Generator (HRSG) Market

- GE Vernova — Leveraging extensive installed base (global HRSG installations in the thousands), integrated solutions with OT/controls, and regional manufacturing hubs, GE plays to scale, digital-enabled performance guarantees, and turnkey delivery. Their in‑house pressure‑part capabilities are a notable risk mitigant for buyers seeking tight schedule control.

- Siemens Energy AG — Siemens positions HRSGs within larger combined-cycle offerings and turbine integrations, favoring DrumPlus and other design platforms that enable close OEM turbine-HRSG integration. Their strength is end-to-end project scope alignment with large combined-cycle EPC work.

- Mitsubishi Heavy Industries — A long-history player with vertical and horizontal flow designs, MHI is often selected for high-temperature/high-pressure projects where long-term reliability is prioritized. Their engineering consistency over decades remains a selling point in conservative utility procurement.

- Babcock & Wilcox and Nooter/Eriksen — These specialists differentiate on retrofit expertise, constructability, and code compliance for diverse international markets. Designs that account for shipping restrictions and site assembly constraints reduce total installed cost in challenging locations.

- Regional players (Thermax, BHEL, Doosan, CMI, VOGT, John Cockerill, Wood) — These firms offer competitive alternatives based on localization, cost optimization, or niche engineering packs (marine applications, modular plants, or specific service bundles). Their role is critical in markets where local content requirements or logistical constraints dictate sourcing.

Recent contract-flow examples underscore market dynamics: integrated OEM orders tied to fuel-transition projects and modular-scope awards for combined-cycle plants appear alongside targeted aftermarket contracts for inlet‑duct and liner replacements. These moves validate the dual growth runway—new-build combined-cycle plus retrofit/modernization services.

Operational levers and scenarios we modelled for 2026

Our report does the heavy lifting for executives who must select between capacity expansion, partnership, or M&A in 2026. We modelled multiple scenarios that stress-test commercial choices across policy, commodity and construction-cost assumptions. Key levers that consistently improve outcomes are:

- Localization vs. centralized manufacturing: criteria to decide when to invest in regional fabrication capacity versus leveraging contract manufacturers.

- Service-first business models: packaging conversions, heat-recovery upgrades and long-term O&M to secure recurring revenue streams.

- Standardization and modularization: component standardization that reduces lead-times and supports modular transportability and repeatable field assembly.

- Supply-chain hedging: strategic alloy sourcing contracts and second-sourcing pressure-part fabrication to limit single-point failure risk.

- Digital performance contracts: embedding OT and predictive maintenance to shift the value mix from one-time supply to operations-linked annuities.

Six immediate strategic recommendations for 2026

- Prioritize aftermarket and retrofit offerings that can be executed with existing field teams—these provide near-term margin stability as new-build order phasing normalizes.

- Conduct a quick-hit supply‑chain audit focused on alloy availability and fabrication lead‑times; convert critical single-source suppliers into dual-source arrangements where feasible.

- Evaluate selective capacity expansion only where order pipelines show multi-year visibility; favor flexible, modular manufacturing cells over large fixed-line investments.

- Develop pilot digital O&M contracts tied to performance KPIs to capture upside from plant efficiency improvements and reduced unplanned outages.

- Use targeted M&A or JV activity to fill capability gaps—especially in modular transportable designs, marine HRSG experience, or regional service networks—rather than broad horizontal consolidation.

- Embed policy-scenario clauses into bid assumptions for projects in jurisdictions subject to evolving taxonomy rules or subsidy programs.

What’s inside the PW Consulting report (operationally focused)

The full study is structured to support board-level and commercial-execution decisions. Deliverables include:

- Market sizing and seven-year forecast (2026–2032) anchored to validated project pipelines and first‑principles demand drivers.

- Scenario modelling that quantifies downside and upside order flows under alternative regulatory and fuel-price regimes.

- Supplier benchmarking and capability maps that highlight manufacturing constraints, alloy dependencies, and site‑assembly risk profiles.

- Actionable go‑to‑market playbooks for OEMs, EPCs and service providers, including pricing levers, contract structures, and aftermarket roll‑out plans.

- M&A and partnership screens that identify targets by capability gap and regional priority (including diligence checklists and integration risk indicators).

- Country‑level policy and subsidy scans with implications for project bankability and timeline acceleration.

- Service and retrofit opportunity maps designed to prioritize field teams and spare‑parts inventory for highest ROI.

How to use this brief

This primer showcases the strategic lines of inquiry and operational levers material to 2026 while preserving the detailed, proprietary segment tables and project-level datasets that underpin our recommendations. If your team is evaluating capacity investments, M&A, or a major shift toward service-led revenue in HRSGs, the full PW Consulting report provides the granular segmentation, region-by-region demand curves and supplier-level analytics you will need to finalize investment cases and procurement strategies.

Next steps

To access the complete intelligence suite—detailed regional and application splits, supplier scorecards, project-level pipeline data and our full scenario models—please contact PW Consulting or visit our HRSG market briefing page. The full report will enable you to convert the strategic direction outlined here into executable plans for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Heat Recovery Steam Generator (HRSG) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com