Strategic Briefing: 3-Methoxypropylamine (MOPA) Market Outlook and Strategic Imperatives for 2026

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present an executive introduction to our new market research on 3-Methoxypropylamine (MOPA, CAS 5332-73-0). This briefing distills the high-conviction insights senior leaders need to align strategy, procurement, and investment decisions in 2026 — while preserving the deeper, proprietary subsegment intelligence that drives tactical execution (available in the full report).

3-Methoxypropylamine (MOPA) (CAS 5332-73-0) Market

Market snapshot and trajectory (data context)

Our base-year analysis uses 2025 as the reference point and covers a historical window from 2020–2025 with a forecast horizon of 2026–2032. The global MOPA market has expanded from roughly USD 90 million in 2020 to USD 120 million in 2025, underpinned by steady demand across corrosion inhibition, chemical intermediates and select agrochemical applications. We forecast continued expansion at a compound annual growth rate (CAGR) of approximately 6.5% across 2026–2032, with the market approaching mid-to-high hundreds of millions of USD by 2032 under the central case.

3-Methoxypropylamine (MOPA) (CAS 5332-73-0) Market

Why this matters: the pace and shape of that growth create distinct windows for competitive advantage — from upstream capacity investments and certification-led premiumization, to downstream formulation lock-ins and distributor consolidation. Our full modeling includes scenario-based revenue paths and sensitivity testing against demand shocks, regulatory shifts, and feedstock price volatility.

3-Methoxypropylamine (MOPA) (CAS 5332-73-0) Market

High-level dynamics shaping strategic choices in 2026

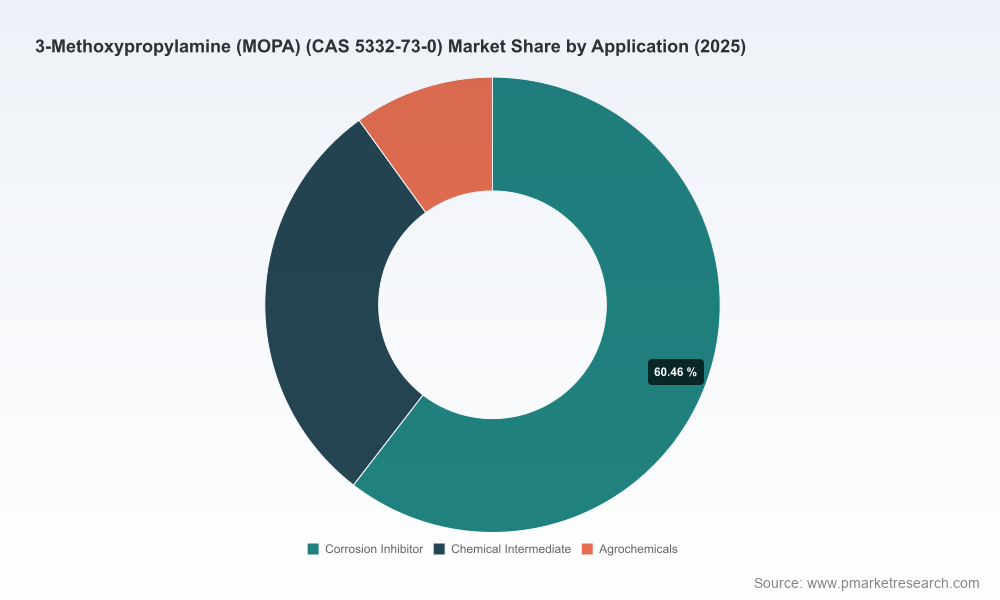

- Demand composition and stability: Demand is concentrated among industrial water-treatment corrosion inhibitors, specialty chemical intermediates (notably pharma building blocks) and a smaller but technical agrochemical segment. Each end market exhibits different tolerance for price, lead time, and purity — an important input for segmentation-aware sourcing and pricing strategies.

- Quality and manufacturing constraints: MOPA production is a multi-step synthesis that frequently requires high-purity infrastructure. These technical requirements create a realistic barrier to rapid capacity expansion for smaller producers and raise the value of certified manufacturing footprints.

- Regulatory and safety overlay: MOPA is listed on the TSCA inventory in the U.S.; standard hazardous-chemical handling rules (e.g., OSHA Hazard Communication) and product-classification regimes (including corrosivity, sensitization and aquatic toxicity considerations) govern manufacturing, transport and downstream use. Public-facing safety classifications from leading suppliers reinforce the need for robust compliance and product stewardship in commercial contracts.

- Concentration and competitive positioning: The market displays moderate concentration — the top three suppliers account for a meaningful minority share and the top five approach a larger, but not dominant, portion of the market. This competitive structure supports opportunities for both incumbents to defend premium niches and challengers to pursue regional or specialty plays.

- Channel dynamics: A mix of integrated chemical majors, regional manufacturers and active distributors defines the go-to-market landscape. Distributors provide critical inventory and logistics flexibility for industrial buyers, while integrated producers compete on quality, traceability and regulatory certifications.

Competitive landscape — what matters to executives

Leading global producers with integrated operations and certified facilities — exemplified by major chemical groups — are positioned to supply high-assay grades, offer bulk packaging options and leverage established quality/safety credentials. Parallel to them are regional manufacturers in Asia and India that provide competitive cost structures and flexible packaging, often servicing domestic and regional industrial chains. Distributors active in North America and Europe supply in-demand inventory and facilitate rapid fulfillment for time-sensitive applications.

Notable strategic implications:

- Integrated majors are best placed to win long-term supply contracts with OEMs and formulators that require capacity guarantees, quality certificates and supply continuity.

- Regional manufacturers can compete on lead time and localized regulatory knowledge — a valuable proposition for domestic formulators and contract manufacturers.

- Distributors add value by offering smaller pack sizes, on-the-shelf availability and attendance at industry events that accelerate matching of buyers and specialty end-users.

Recent commercial activity in 2026 underscores these dynamics — distributors are actively promoting MOPA at specialty chemical events, while suppliers continue to emphasize certified manufacturing and high-assay grades in their product communications.

Strategic options and playbooks for 2026 decision-makers

- For procurement leaders: Move beyond spot sourcing. Prioritize a two-track sourcing strategy combining a certified integrated producer for primary supply and a regional manufacturer/distributor for contingency. Embed quality acceptance criteria (assay, impurity profile), regulatory compliance clauses and dynamic price-adjustment mechanisms into contracts.

- For chemical manufacturers and CMOs: Evaluate selective capex to upgrade purification and QA capabilities if your roadmap requires entry into pharma-grade supply chains. Certification attainment (ISO 9001, ISO 14001, OHSAS/ISO 45001 equivalents) can notably expand addressable demand and justify price premiums.

- For distributors and specialty traders: Invest in inventory density at key logistics hubs and develop technical service capabilities (e.g., formulation support, small-batch packaging). Trade-show presence and direct OEM engagement drive velocity in fragmented opportunity pools.

- For investors and M&A strategists: Look for targets that combine niche technical capability (high-purity synthesis, regulatory dossiers) with stable industrial offtake. The market’s moderate top-line concentration creates acquisition pathways to scale regional incumbents into larger global niches.

Risk matrix — triggers to monitor in 2026

- Feedstock and energy price volatility: Elevated input costs can compress margins for non-integrated producers.

- Regulatory tightening: Stricter occupational or environmental rules could raise compliance costs and shift sourcing toward certified suppliers.

- Capacity shocks: Disruptions at a few mid-sized plants can tighten availability given the technical production footprint.

- Demand-side shifts: Faster-than-expected substitution or reformulation in major end markets would alter demand elasticity and pricing power.

What’s included in the PW Consulting MOPA report (practical deliverables)

The full market study is designed as an operational tool for decision-makers. Key components include:

- Base-year (2025) market sizing and a detailed historical series (2020–2025).

- Scenario-based forecasts for 2026–2032 with sensitivity runs to test demand and supply shocks.

- Supply-side mapping that profiles integrated producers, regional manufacturers and distributor networks, including capability matrices and certification status.

- Regulatory and product-stewardship dossier compiling jurisdictional requirements, labeling and handling implications for industrial users.

- Commercial playbooks: contracting templates, procurement scorecards, and supplier due-diligence checklists tailored to MOPA’s hazard profile and quality requirements.

- Go-to-market and M&A decision frameworks: target prioritization, valuation lenses and integration checklists for buyers and investors.

- Risk/contingency planning templates, including inventory hedging models and crisis-response flows tied to supplier disruptions.

Note: In keeping with our “trailer” principle, the public briefing intentionally omits granular subsegment revenue breakdowns, regional percentage splits and supplier-level shipment volumes. Those detailed data series, primary-sourced supplier contacts, and downloadable Excel models are included exclusively in the full PW Consulting report.

Actionable next steps for leaders in 2026

- Short term (0–6 months): Secure primary supply with a certified integrated producer and qualify a regional backup; update safety and procurement clauses to reflect current classifications and handling requirements.

- Medium term (6–18 months): Complete an assessment of internal high-purity processing capability vs. outsourcing; if pursuing in-house capability, prioritize modular upgrades that reduce scale risk.

- Longer term (18–36 months): Evaluate strategic acquisitions or partnerships to close capability or geographic gaps; lock in multi-year offtakes with price-review mechanisms tied to feedstock indices.

Conclusion — the strategic value of timely, granular intelligence

For 2026 executives, MOPA represents a technically demanding but commercially attractive specialty-amines market segment. Its growth profile—backed by a 6.5% CAGR into the forecast period—creates distinct opportunities to capture margin and market share, provided strategies are calibrated to manufacturing realities, regulatory compliance demands, and the competitive split between integrated producers, regional manufacturers and distributors.

PW Consulting’s full study delivers the granular subsegment data, supplier scorecards and executable templates that convert these strategic insights into commercial outcomes. For companies preparing procurement negotiations, capex approvals, or M&A diligence this year, access to the underlying datasets and supplier-level intelligence in the full report is the difference between directional strategy and executable advantage.

To request the full report, scenario models, or a tailored briefing for your executive team, please contact PW Consulting. Our advisory team can walk you through supplier risk matrices, cost-to-serve models, and the tailored playbook most relevant to your role (procurement, R&D, manufacturing or corporate development).

For detailed analysis of this topic, please visit the official page:3-Methoxypropylamine (MOPA) (CAS 5332-73-0) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com