GABA (CAS 56-12-2) Market: Strategic Preview for 2026 Decision-Making

As PW Consulting’s senior strategic advisor and lead industry analyst, this introduction previews the strategic value of our full GABA (gamma-aminobutyric acid) market study (base year 2025). The substance is emerging as a multi-sector ingredient—spanning nutraceuticals, food & beverage innovation, personal care and animal nutrition—and the choices companies make in 2026 will materially affect their competitive positions through the next business cycle. Below we synthesize the report’s highest‑value takeaways, grounded in our proprietary market model, while deliberately reserving core segmentation detail to incentivize direct access to the full study.

GABA (CAS 56-12-2) Market

Market snapshot: scale, trajectory and structure

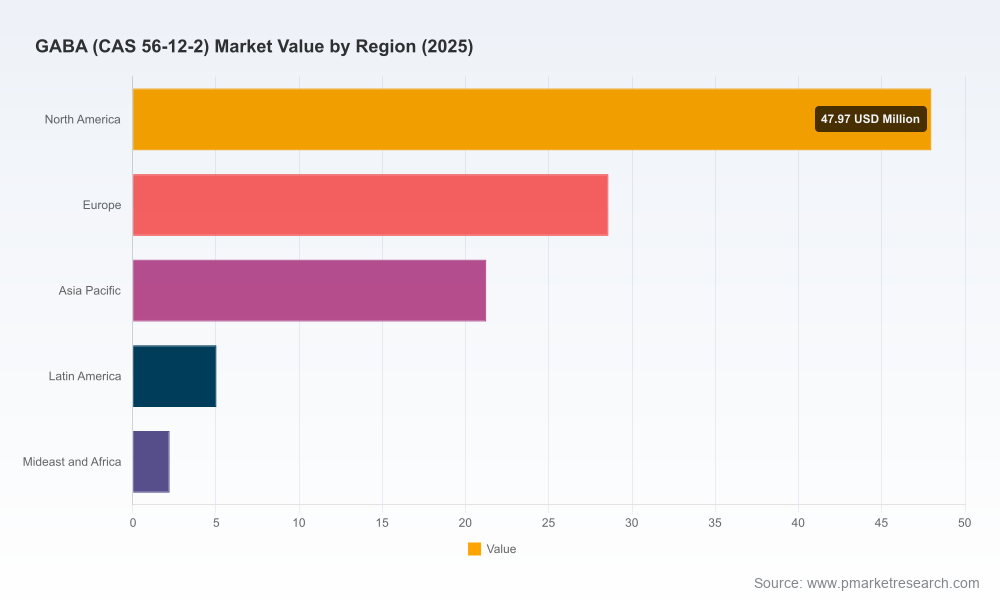

The global GABA market is at an inflection point. Our model, calibrated to historical performance (2020–2025) and rolling forward across seven forecast years (2026–2032), shows the market expanding from an estimated USD 105.0 Million in 2025 to roughly USD 147.8 Million by 2032, reflecting a compound annual growth rate of 5.0% over the forecast period. That steady, mid-single-digit growth combines structural demand from established end‑uses with increasing product innovation and new formulation adoption.

GABA (CAS 56-12-2) Market

Concentration metrics in our analysis indicate a market that is still fairly fragmented: the top three players account for only a quarter of global supply while the top five account for roughly thirty percent. This fragmentation creates a strategic environment where nimble specialty producers, vertical integrators, and innovation‑led entrants can capture disproportionate value—particularly if they secure quality credentials, scale, or unique application know‑how.

GABA (CAS 56-12-2) Market

What is driving growth in 2026 and beyond?

- Formulation migration and functionalization: GABA’s role as a functional ingredient—promoted for sleep, relaxation, and stress-support positioning—has moved it from niche supplements into broader functional food and beverage formats. Consumers’ preference for ingredients with demonstrable physiological effects continues to support reformulation and premiumization strategies.

- Production technology convergence: Fermentation‑based production and advanced chemical synthesis routes coexist in the market. Improvements in fermentation strain development and process yields are reducing the cost gap and enabling expanded use in food-grade and personal-care applications.

- Regulatory clarity: Regulatory recognition—most notably GRAS determinations and national registrations—has lowered commercial friction in major markets. A notable example is the self‑affirmed GRAS profile of specific branded ingredients and their formal registration as new food raw materials in some jurisdictions, which accelerates adoption in packaged goods and foodservice chains.

- Certification & quality premiuming: Certification for personal‑care use and traceable fermentation sourcing (e.g., ECOCERT, food‑grade attestations) is enabling higher margins and opening distribution channels that were previously inaccessible to commodity providers.

- Adjacency demand: Growth in animal nutrition and niche industrial uses adds non‑linear demand, smoothing seasonality and providing avenues for volumetric scale.

Competitive landscape: players to watch (high‑level)

Our competitive analysis profiles both long‑established bioscience incumbents and regionally focused fermentation specialists. Collectively they demonstrate three strategic archetypes: brand‑driven licensors, fermentation specialists, and diversified amino‑acid producers. Selected observations:

- Pharma Foods International Co., Ltd. (Kyoto, Japan): The company’s PharmaGABA®—produced by patented lactobacillus fermentation—remains a benchmark for branded, clinically‑oriented GABA. Recent scientific publications in early 2026 and repeated recognition for workplace health management reinforce both the ingredient’s evidence base and the brand’s institutional credibility. Their established regulatory foothold in multiple markets accelerates adoption by large food and supplement manufacturers seeking lower entry risk.

- Bloomage Biotechnology Co., Ltd. (Jinan, China): With a fermentation‑derived offering positioned for food and personal‑care applications and ECOCERT certification for personal care, Bloomage exemplifies a strategy combining quality credentials with market segmentation—targeting higher‑margin channels that value traceability and natural sourcing.

- Kyowa Hakko Bio Co., Ltd. (Tokyo, Japan): As a nutraceutical ingredient specialist, Kyowa Hakko brings deep fermentation know‑how and supply chain integration. Their presence supports strategic customers seeking turnkey ingredient reliability and technical collaboration on formulation stability and bioavailability.

- Richen Nutritional Technology Co., Ltd. (Shanghai, China): Richen’s food‑grade fermentation outputs and branded ingredient programs underscore the importance of scale at cost‑competitive quality levels for mainstream food and supplement customers.

- Zhejiang Yiwan Biolabs Co., Ltd. (Zhejiang, China): As part of a broader amino‑acid portfolio, players like Yiwan illustrate the optionality that diversified producers have—leveraging existing fermentation platforms to flex into GABA as margin conditions and demand dictate.

These firms illustrate the competing strategic plays: invest in branded clinical evidence and regulatory clearance to command premium positioning; pursue certification and product differentiation for personal‑care and high‑value food channels; or double down on scale and cost competitiveness to serve mass-market formulations.

Regulatory and quality signals that matter to 2026 strategy

- Regulatory clarity in major markets has de‑risked product launches. Multiple GRAS determinations and documented national registrations for certain branded GABA ingredients are key enablers for food and beverage formulators.

- Certification for personal‑care applications and documented food‑grade quality systems are differentiators that unlock higher margin channels; this is already being leveraged by select suppliers.

- Broadly, GABA production does not face unusual regulatory hurdles beyond standard food‑grade and supplement labeling regimes—however, the value of documented safety studies and compliance declarations cannot be overstated when negotiating with multinational branded customers.

Strategic priorities for corporate leaders in 2026

If you are evaluating portfolio moves, supply agreements, capacity investments or M&A in the GABA space this year, prioritize actions with asymmetric upside and limited downside:

- Secure branded supply and regulatory comfort: For consumer goods firms and ingredient distributors, securing supply from GRAS‑backed and nationally registered sources reduces time‑to‑market and legal exposure. Negotiate quality‑anchored contracts with performance and continuity clauses.

- Invest selectively in fermentation capabilities: Proprietary fermentation strains and process IP are defensive assets. Licensing or minority investments into fermentation specialists can reduce price exposure while preserving option value for formulation innovation.

- Pursue certification as a route premiuming: Certification for cosmetic and natural product markets can unlock higher ASPs; integrate certification strategy with sales and marketing plans for these channels.

- Differentiate through application science: Fund targeted clinical or consumer studies that validate effects in specific delivery systems (e.g., beverage formats, sachets, topical products). Evidence‑led differentiation materially increases buyer willingness to pay.

- Prepare for consolidation windows: With market concentration relatively low, attractive consolidation opportunities will favor acquirers with integration playbooks—target companies with clean quality systems and channel access rather than speculative technology bets.

- Embed scenario‑based risk planning: Model price swings in upstream feedstocks and capacity ramp timelines across conservative, base and aggressive adoption scenarios to stress test strategic plans.

What the full PW Consulting report delivers (operationally actionable content)

The full study is designed as a playbook for 2026 strategy teams. Highlights of the operational content include:

- Market sizing and validated forecast model (2026–2032) with scenario toggles to test adoption curves under alternative policy and demand assumptions.

- Product taxonomy and route‑to‑market maps distinguishing fermentation vs synthesis pathways, quality tiers, and channel economics.

- Go‑to‑market and commercial frameworks tailored to ingredient suppliers, formulation houses and CPG brands—covering pricing levers, channel entry strategies, and contract structures.

- Supply chain and capacity analysis highlighting pinch points, raw material exposure, and near‑term expansion projects to anticipate pricing pressure.

- Regulatory and certification compendium capturing GRAS status, national registrations and certification options across key geographies.

- Company profiles, capability assessments and strategic benchmarks for leading providers—illustrating where competitive advantage is built (R&D, regulatory, scale, certification).

- M&A and partnership screening matrices identifying high‑value targets and partnership archetypes for rapid capability acquisition.

- Risk register and mitigation playbook, including supply shocks, rapid product substitution, and reputational risk scenarios.

How to use this preview—and next steps

This introduction is structured to give corporate decision‑makers a clear line of sight on why 2026 is a pivotal planning year, and what types of strategic moves will generate optionality through 2032. To preserve commercial value for paying subscribers, granular segmentation tables, region‑ and application‑level splits, and confidential company revenue estimates are withheld here. Those data elements are essential for transaction diligence, procurement negotiations, and capex sizing—and they are included in the paid report.

If your 2026 plan includes product launches, supply commitments, or M&A in the GABA space, PW Consulting can provide: (1) a tailored briefing that overlays your corporate position on our model; (2) a rapid diligence package focused on target shortlists; or (3) a commercialization playbook that sequences regulatory, quality and go‑to‑market steps for accelerated launch. Reach out to our industry desk to arrange a confidential briefing and obtain the full report materials.

In short: the GABA market offers both predictable growth and asymmetric opportunities for value capture. The companies and strategies that combine evidence‑led branding, certified quality, and flexible fermentation capacity will command durable advantage as the market expands at an expected mid‑single‑digit CAGR through 2032. Use our full report to convert this preview into executable priorities for 2026.

For detailed analysis of this topic, please visit the official page:GABA (CAS 56-12-2) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com