High Purity Iron Market: Strategic Preview for 2026 Decision-Making

Executive snapshot

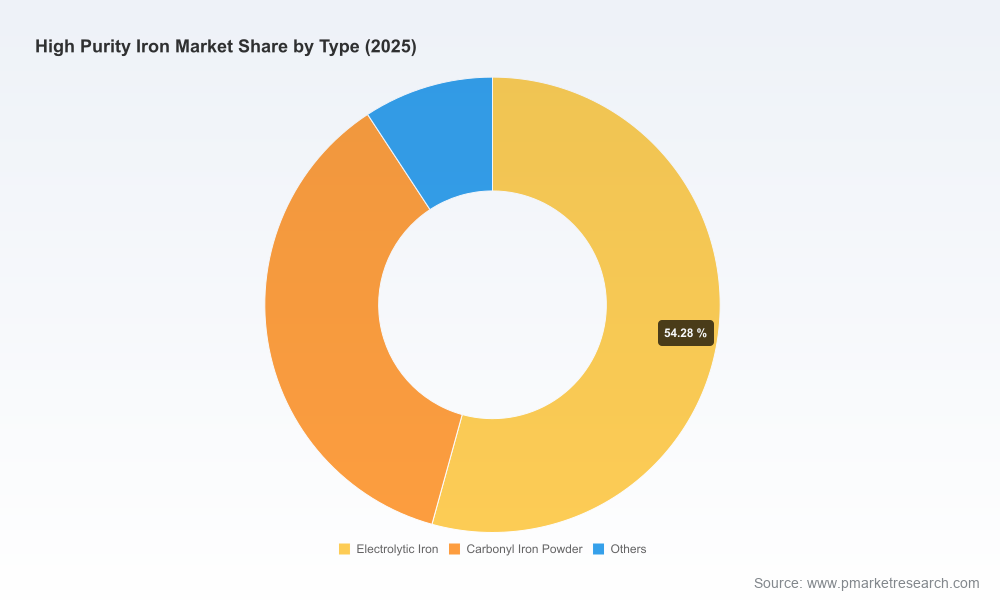

Between 2020 and 2025 the high purity iron market demonstrated steady, investment-grade growth—rising from approximately USD 160 million to USD 215 million (base year 2025). Our forecast horizon (2026–2032) projects a continuation of that trajectory at a compound annual growth rate (CAGR) of roughly 6.95%, taking the market from an estimated USD 224.6 million in 2026 toward a mid-2030s valuation in the high hundreds of millions (our model points to about USD 339.5 million by 2032). Market concentration is meaningful: the top three suppliers account for a material share of the market (CR3 ~62%), and the top five firms control roughly three quarters (CR5 ~76%).

High Purity Iron Market

Why this matters for corporate strategy in 2026

- Timing: 2026 is the inflection year for multiple demand drivers—semiconductor tooling requirements, stricter purity/regulatory standards in electronics and biomedical applications, and accelerated decarbonization efforts in specialty steel production.

- Supply leverage: Concentration metrics indicate that supply-side moves by a small group of established suppliers can shift pricing, qualification timelines and access to ultra-high purity grades quickly.

- Risk-reward balance: The sector exhibits the classic high-margin but high-barrier economics—firm grade control, regulatory compliance and technical validation create durable margins once supply agreements are secured, but they also raise switching costs for buyers.

Market trajectory and what the headline numbers hide

The headline growth (CAGR ~6.95%) reflects three simultaneous effects: steady replacement and growth of legacy applications (magnetic materials, specialty alloys), rapid premiumization for electronics and semiconductor tooling, and selective capacity investments enabling higher throughput of electrolytic and ultra-high purity grades. From an investor or procurement standpoint, the year-on-year rise from USD 160M in 2020 to USD 215M in 2025 validates the transition from niche commodity to strategic input—yet the aggregate figures conceal how value accrues across purity tiers, form factors (powder, flake, billet, rod), and qualification pathways. That opacity is exactly why procurement and strategy teams need a decomposed, actionable view rather than headline aggregates alone.

High Purity Iron Market

Demand and supply dynamics shaping 2026 choices

- Regulatory tightening and performance standards: Recent regulatory moves—such as Canada's 2025 inclusion of high-purity iron on its critical minerals list and industry-driven quality mandates for semiconductor and biomedical applications—are forcing buyers toward electrolytic and ultra-high purity routes. These regulatory signals accelerate qualification cycles for compliant suppliers and lengthen the time-to-contract for new entrants.

- Material and process constraints: Improvements in iron ore availability and unit pricing (observed through 2024) lower raw-material cost pressure, but process-specific constraints—especially for carbonyl processes and the handling of iron pentacarbonyl—have tightened supply-chain resilience and increased compliance costs for certain production routes.

- Capacity and strategic alliances: Select capacity expansions and strategic minority investments (for example, chemical producers aligning with industrial gas companies or equipment makers partnering with specialty metal suppliers) are re-shaping route-to-market for ultra-high purity grades. These moves materially affect lead times and the shape of long-term off-take agreements.

Competitive landscape — who matters and why

The market is anchored by a mix of legacy metallurgical players, specialty powders producers, and materials distributors that each bring distinct advantages to buyers and investors. Our sector scan highlights several strategically significant players:

High Purity Iron Market

- Allied Metals Corporation (USA): Positions itself with a branded high-purity iron product line focused on low-impurity chemistries and tailored alloys—appealing to alloying and vacuum-melted superalloy customers that demand certified chemistries and traceability.

- TOHO ZINC CO., LTD. (Japan): A leader in electrolytic iron with product grades extending into ultra-high purity territory; their strength is process expertise that serves magnetic and high-performance electronic applications where ppm-level control matters.

- Industrial Metal Powders India (India): Growing capacity and cost-competitive electrolytic iron powder production; their recent expansions reflect demand elasticity in pharmaceutical and industrial applications where scale and regulatory certifications intersect.

- American Elements (USA), William Rowland (UK), AK Steel International (Netherlands), QS Rare Elements (USA), and Goodfellow (UK): Each brings differentiated offerings—from research-grade ultra-high purity forms to bulk industrial billets and flake—making them attractive either for R&D partnerships, pilot-scale supply or as tier-1 preferred suppliers for qualifying customers.

Recent commercial moves—large contract awards for ultra-high purity powder and minority stake investments in regional facilities—underscore an industry consolidating around quality, supply security and long-term contractualisation.

Recent developments and regulatory signals to watch

- Commercial wins & partnerships: A sequence of contract wins with semiconductor equipment suppliers and co-development partnerships for advanced electronics packaging reflects an urgent, high-value demand segment that prioritizes traceability and zero-failure tolerances.

- M&A and strategic investments: Minority stakes and partnerships (observed in 2024–2025) are increasingly being used as strategic levers to lock in supply to electronics and semiconductor ecosystems—an important precedent for buyers seeking supply security in 2026.

- Safety and environmental regulation: Tightening standards around handling carbonyl iron and environmental controls for ultra-purity production are raising the bar for certification and on-site controls—creating both a barrier to entry and a moat for compliant producers.

What PW Consulting’s full report delivers (practical, decision-grade content)

Our comprehensive study is built to move decision-makers from "awareness" to "action." The full deliverable provides:

- A validated historical dataset (2020–2025) and a transparent, scenario-based forecast model for 2026–2032, including sensitivity to purity premium, qualification timelines and regional demand drivers.

- A supplier matrix with production routes, capacity estimates, qualification credentials, technology strengths and quantifiable lead-time risks—ranked for strategic sourcing decisions.

- Commercial playbooks and negotiation levers for buyers and investors: supplier qualification checklists, procurement contracting templates (including sample clauses for quality, traceability and force majeure), and capex vs. purchase decision frameworks.

- Value-capture frameworks for suppliers: route-to-market strategies, price-mix modelling, and go-to-market recommendations for entering or upgrading presence in electronics, pharmaceuticals and specialty alloys.

- Regulatory and compliance tracker: a jurisdictional map of emerging standards and actionable mitigations tied to qualification and capital planning horizons.

To honor our “trailer” principle, the report highlights that the granular segmentation tables, the proprietary unit-cost model and the supplier-level revenue/volume splits are available only in the full report; those are the elements that materially change commercial outcomes and require access to the source dataset.

Actionable decision frameworks for 2026

- Procurement: Adopt a two-track sourcing strategy—secure a primary, long-term qualified supplier for ultra-high purity grades while maintaining an alternate short-list for scale or emergency supply. Use staged qualification milestones to balance speed versus certification risk.

- Supply-side investors/manufacturers: Prioritise investments in electrolytic production and environmental control technologies that reduce compliance costs. Consider minority investments or offtake agreements with regional producers to shorten qualification cycles for end-customers in strategic markets.

- R&D and product teams: Prioritize materials co-development with suppliers that can demonstrate ppm-level control and documented traceability. Early co-validation reduces adoption friction and shortens time-to-revenue.»

- M&A and corporate development: Look for targets that combine production scale with niche ultra-high-purity capabilities, or facilities that can be retrofitted to electrolytic production with modest capex and clear regulatory pathways.

Decision triggers and watchlist for the next 12–18 months

- Contract awards by major semiconductor equipment OEMs and large-scale capacity expansions—these are leading indicators of near-term surge demand and qualification bottlenecks.

- Regulatory updates affecting carbonyl routes and environmental permitting—any abrupt tightening can reroute demand to electrolytic producers and complicate supply chains.

- Supplier consolidation or strategic investments by large commodity or industrial gas players—signals that supply security is being vertically integrated and that pricing dynamics may shift.

Closing—how PW Consulting’s insight helps you act in 2026

For executives planning capital allocation, procurement directors finalizing supplier shortlists, and strategists designing market entry or M&A plays, the high purity iron market in 2026 is no longer a peripheral input—it's a strategic lever. The aggregate growth story (from roughly USD 160M in 2020 to USD 215M in 2025 and projected CAGR near 7% through 2032) validates investment. The structural details—supply concentration, regulatory tightening, and route-specific constraints—determine which projects win. Our full report turns the macro narrative into transaction-grade intelligence: supplier-scorecards, price/mix sensitivity runs, and contractual playbooks that materially shorten the path from insight to procurement and investment action.

To access the full dataset, supplier-by-supplier analysis, and the proprietary forecast workbook that underpins these recommendations, refer to the PW Consulting High Purity Iron Market full report—your operational playbook for 2026.

For detailed analysis of this topic, please visit the official page:High Purity Iron Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com