Asia-Pacific Chromatography Solvents Market Dynamics: Key Drivers and Restraints

Other |

2026-06-22 04:07:01

As textile manufacturers, chemical suppliers, and investors prepare strategies for 2026, the yarn lubricant market is shifting from a component-driven commodity to a strategically managed lever for productivity, sustainability and product differentiation. PW Consulting’s latest market study — anchored on a 2025 base year and a 2026–2032 forecast window — synthesizes five years of historic performance (2020–2025) and projects forward at a 5.7% compound annual growth rate (CAGR). The market grew steadily from the low hundreds of millions in 2020 to reach approximately USD 800 Million in 2025, with a projected trajectory that approaches USD 1.17 Billion by 2032. These macro dynamics create concrete inflection points for procurement, R&D prioritization, go-to-market planning, and M&A activity in the coming 12–24 months.

Yarn Lubricant Market

Cost-to-quality trade-offs are evolving: manufacturers are increasingly treating yarn lubricants not merely as consumables but as performance enhancers that influence machine uptime, yarn breakage rates, and downstream processing yield.

Yarn Lubricant Market

Sustainability is reshaping acceptance criteria: new certified formulations and OEKO‑TEX/GOTS-aligned chemistries create both barriers and opportunities for suppliers and upstream buyers looking to claim sustainable credentials.

Yarn Lubricant Market

Consolidation and competitive intensity: the market shows moderate concentration—our study finds the top three suppliers account for roughly a third of market share, and the top five near half—creating a landscape where scale, technology differentiation, and distribution reach determine who can move price and service terms.

Between 2020 and 2025 the market expanded meaningfully as spinning throughput and synthetic fiber penetration rose across mature and emerging textile hubs. In 2025 the total market crossed an important threshold (circa USD 800 Million), and at a 5.7% CAGR the sector is set to expand by several hundred million dollars through 2032. For decision-makers, the arithmetic is straightforward: incremental performance or sustainability advantages in lubricant formulations can be monetized across a sizable and growing installed base, but capturing that value requires coordinated actions across procurement, process engineering, and product management.

Practically, manufacturers should plan for three near-term priorities in 2026:

Operational pilots: convert lab claims into mill-level KPIs (breakage reduction, yarn strength distribution, maintenance interval extension) and quantify cost per kilogram of yarn saved — not just lubricant unit cost.

Sustainability procurement criteria: update vendor scorecards to include certified supply chain attributes and end-product compatibilities; prioritize suppliers with documented certifications and circularity roadmaps.

Supplier segmentation: separate transactional supply (price-driven) from strategic partnerships (co‑development, joint trials, service agreements) to allocate R&D budgets and negotiate differentiated commercial terms.

Performance-driven differentiation. Suppliers that demonstrate tangible machine-productivity improvements—extended maintenance intervals, reduced energy consumption, lower yarn wastage—command better commercial terms and adoption rates. Notably, recent field demonstrations have shown step-changes in equipment uptime when combined with service models that include predictive maintenance and OEM alignment.

Regulatory and certification drivers. Certified formulations (for example, REDcert²-validated eco‑lubricants and GOTS/OEKO‑TEX aligned chemistries) are rapidly moving from “nice-to-have” to procurement prerequisites for brands demanding transparency across the supply chain. Expect certified product lines to gain premium positioning in 2026 RFPs and supplier shortlists.

Fragmentation at the supplier level. With the leading three firms holding roughly 35% and the top five close to 45% of the market, mid‑sized specialists remain important innovators and regional supply anchors. This structure rewards both partnerships with regional champions and targeted M&A for global reach.

The competitive map combines global specialty chemical houses, regional formulators, and niche engineered-lubricant providers. All are racing to blend performance claims with sustainability credentials and to extend service offerings beyond simple product delivery. Selected profiles illustrate the strategic diversity:

Klüber Lubrication (Munich): a leader in specialty lubricants for textile machinery, notable for launching REDcert²-certified products and running productivity demonstrations that extend equipment intervals and boost throughput. Their approach emphasizes OEM collaboration and machine‑level value capture.

Rudolf GmbH (Augsburg): focuses on yarn and sewing-thread lubricants with a portfolio that spans wet waxing agents and antistatic treatments—targeting improved yarn handling and downstream durability.

Sarex Chemicals (India): a supplier with strengths in concentrated formulations for friction reduction and antistatic performance—positioned for export-led growth and value propositions tied to rewinding and gliding efficiency.

RAZON Engineering (India): offers thread and yarn emulsions and solutions that integrate with pelletization and sewing-thread manufacturing—representing the kind of regional specialist that serves high-volume local mills.

Zschimmer & Schwarz (Germany): combines specialty chemical expertise with compliance-focused products (GOTS/OEKO‑TEX alignment), making them attractive to brands and mills targeting sustainable natural and synthetic yarns.

Certifications and sustainability launches: suppliers pushing third‑party certified lubricants are turning sustainability compliance into a commercial moat. Buyers should reassess qualification timelines to incorporate certified alternatives.

Demonstrated productivity gains: publicized case studies showing dramatic increases in equipment uptime or productivity materially shorten the buyer’s evaluation cycle when replicated in local mill pilots.

Regional innovation hubs: expect more product introductions from Asia-based formulators focused on cost-performance trade-offs, and from European players focused on premium, compliance-driven formulations.

This research is designed to be decision‑grade for 2026. Highlights include:

A concise market sizing and forward projection calibrated to a 2025 base and projecting through 2032, including a transparent methodology and sensitivity scenarios that reflect raw material cycles and regulatory tightening.

Value-driver centric analysis: quantified links between lubricant attributes and operational KPIs (e.g., yarn breakage rates, maintenance intervals), alongside modelled ROI cases for common mill scales.

Supplier playbooks: profiles of leading vendors, comparative scoring on technology, sustainability, service, and distribution capabilities, plus negotiation templates and contract clauses tailored for both transactional and strategic engagements.

Go-to-market roadmaps: product positioning blueprints and channel strategies for suppliers seeking to scale regionally or enter new vertical niches (e.g., performance fibers, technical textiles).

M&A and partnership diagnostics: guidance on target screening, valuation adjustments for intangible capabilities (certifications, OEM partnerships), and integration checklists.

Built for executives, procurement leads and product managers, our recommended sequencing for 2026 decisions is:

Q1: Rapid internal audit — quantify current lubricant-related losses (stoppages, breakage, rework) and validate with machine OEMs the scope for improvement through alternative chemistries and service packs.

Q2: Pilot and procurement design — run controlled mill pilots with two contrasting suppliers (one performance-focused, one certified-sustainability-focused) and measure against standardized KPIs over 6–8 weeks.

Q3: Commercialization or scale-up — translate pilot learnings into supply contracts that include performance-bonded service levels, joint product development clauses, or price/volume ladders depending on outcomes.

Q4: Portfolio and partnership review — reassess supplier segmentation, update tender documents to incorporate sustainability thresholds, and explore co-development or M&A where scale or capabiliy gaps persist.

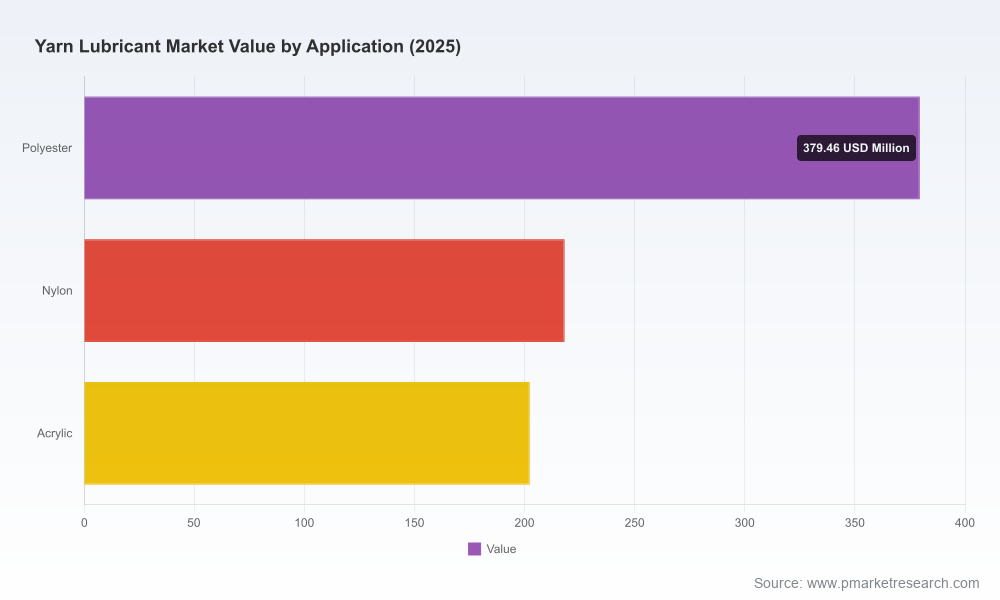

To preserve the strategic value of our full study for subscribers and clients, this preview emphasizes the decision-making implications while intentionally withholding granular segmentation data, specific regional or application share breakdowns, and vendor pricing matrices. These detailed datasets—along with downloadable KPI templates, supplier scorecards, and modeled ROI spreadsheets—are included in the full PW Consulting report, enabling teams to run bespoke financial and operational scenarios aligned to their scale and geography.

As the yarn lubricant market continues its steady expansion, the firms that win in 2026 will be those that convert chemical and service innovations into measurable mill-level outcomes, align procurement to sustainability imperatives, and structure commercial relationships to share both risk and upside. Whether you are a mill operator seeking to reduce unit costs and improve throughput, a supplier aiming to ascend the value chain, or an investor evaluating consolidation targets, the strategic playbook in PW Consulting’s full report will help translate market growth into concrete competitive advantage.

For companies preparing RFPs, planning pilots, or evaluating partnerships in 2026, PW Consulting’s comprehensive dataset and operational tools provide the necessary scaffolding to act decisively. Contact our research desk to access the complete study and the downloadable toolkits that underpin the recommendations summarized here.

For detailed analysis of this topic, please visit the official page:Yarn Lubricant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com