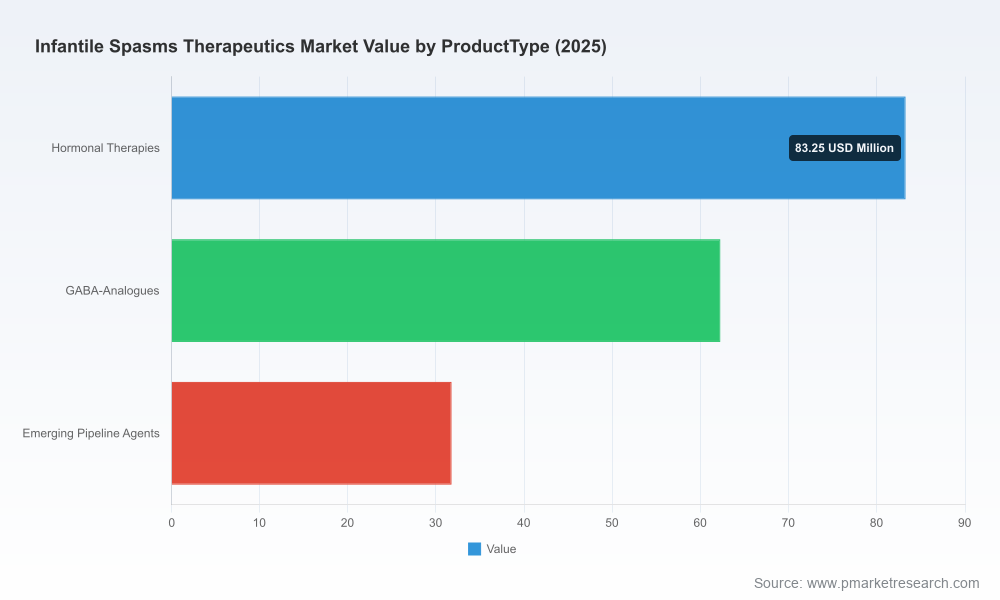

Infantile Spasms Therapeutics Market: Strategic Preview for 2026 Decision-Making

PW Consulting presents a forward-looking, executive-grade preview of our full Infantile Spasms Therapeutics Market study — a tactical resource designed to inform board-level prioritization, launch sequencing, and M&A screening as companies plan for 2026 and beyond. This piece synthesizes the study’s most consequential insights, highlights structural market dynamics and competitive forces, and explains precisely how senior commercial and R&D leaders should use the underlying analysis to shape near-term choices. Consider this a trailer: rigorous, actionable, and directional — while preserving the granular segment-level intelligence that lives in the full report.

Infantile Spasms Therapeutics Market

Why this market matters to 2026 strategies

Infantile spasms (infantile epileptic spasms syndrome) is a small, clinically urgent therapeutic area where treatment choice and timing materially affect developmental outcomes. From a commercial perspective the market combines constrained patient populations, high per-course therapy costs, and distinct access/regulatory hurdles — a mix that creates outsized value for targeted clinical differentiation, optimized payer strategies, and tightly controlled supply chains.

Infantile Spasms Therapeutics Market

From a macroeconomic viewpoint, our modeling shows a steady expansion trajectory: the market expanded through the early 2020s and reached approximately USD 177 million (base year 2025). Under our base-case forecast it grows at a compound annual growth rate (CAGR) of 4.25% across the 2026–2032 horizon, reaching roughly USD 237 million by 2032. That trajectory masks important volatility driven by pipeline readouts, reimbursement shocks, and episodic supply constraints — dynamics that make timing and sequencing of strategic moves especially critical.

Infantile Spasms Therapeutics Market

What the full study delivers (practical content summary)

- Proven forecasting framework: historical reconciliation (2020–2025) plus probability-weighted scenarios for 2026–2032, enabling stress-testing of launch and investment decisions against conservative, base, and upside cases.

- Go-to-market playbooks: tailored commercialization blueprints for new molecular entities, reformulated legacy agents, and biosimilar/generic entrants — covering pricing, channel design, and provider targeting.

- Payer-access and reimbursement models: simulation of prior-authorization pathways, time-to-therapy impact analyses, and recommended evidence dossiers to shorten access delays in key payer systems.

- Regulatory & HTA impact assessment: line-by-line mapping of approval levers, monitoring requirements, and the implications of REMS-like programs on treatment adoption.

- Clinical & pipeline intelligence: comparative assessments of marketed therapies and late-stage pipeline agents, with trial-readiness evaluation and attrition-weighted probability of success.

- Supply chain and manufacturing risk diagnostics: identification of single-point failures, coldchain needs, and distribution constraints that can materially reduce addressable uptake at launch.

- M&A and partnership screening: a prioritized list of target profiles (technology, geography, and stage) with modeled upside and integration risk buckets.

- Real-world evidence (RWE) playbook: pragmatic study designs and data partnerships aimed at securing earlier coverage and conditional reimbursement.

Market structure and competitive posture

The competitive landscape is heterogeneous: incumbent specialty players with established products coexist with smaller innovators advancing novel mechanisms and formulations. Market concentration is meaningful but not monopolistic — our CR3/CR5 analysis shows that the top three suppliers together represent a modest fraction of the market, while the top five account for a majority share. That structure produces both opportunity and friction: established brands command clinical trust and channel relationships, but there is room for disruptive entrants that can materially improve clinical outcomes, simplify monitoring burdens, or reduce total treatment cost.

Key commercial players profiled in the study include multi-national specialty pharmaceuticals and smaller, focused firms:

- H. Lundbeck A/S — a leading supplier of vigabatrin formulations, with both tablet and pediatric oral solution assets positioned for early-life monotherapy. Lundbeck’s portfolio benefits from clinician familiarity and recent clinical disclosures that speak to broader rare epilepsy ambitions.

- Mallinckrodt Pharmaceuticals — provider of repository corticotropin (ACTH) therapies. ACTH remains a clinically effective but high-cost option; its role in payer formularies and hospital procurement continues to shape comparative-cost modeling across markets.

- GW Pharmaceuticals plc — historically active in cannabidiol (CBD) therapeutics with established regulatory and commercialization capability; CBD’s role in infantile spasms is an ongoing clinical and strategic debate, particularly as firms test differentiated formulations and label expansions.

- Orphelia Pharma SA — focused pediatric formulations of vigabatrin, positioned as first-line therapy in many clinician pathways; smaller companies with niche pediatric positioning can win share quickly where clinical guidance favours them.

- Insys Therapeutics, Inc. — pursuing pharmaceutical cannabidiol development for infantile spasms; builds on an emerging class where regulatory clarity and payer receptivity will determine commercial potential.

Recent clinical and corporate developments materially alter the playing field. Notably, H. Lundbeck presented 12‑month results from an open-label extension of a Phase 1b/2a trial (PACIFIC) in April 2026 for a novel agent (bexicaserin) in rare childhood-onset epilepsies, including infantile spasms. Such readouts accelerate the immediacy of launch planning and make early engagement with KOLs and payers imperative.

Access, regulatory and supply dynamics that change decision priorities

Our diagnostics call out four structural frictions that should shape every 2026 plan:

- Clinical monitoring obligations: certain therapies require mandated manufacturer certification and regular ophthalmologic screening for infants, with additional annual monitoring costs that meaningfully affect total cost of care and parental adherence patterns.

- Payer gatekeeping and timing risk: prior-authorization delays are a recurring access obstacle; in some systems these delays can extend up to multiple weeks — long enough to miss optimal early treatment windows that correlate with developmental outcomes.

- Regulatory milestones can re-order markets quickly: recent pediatric approvals for oral solution formulations have changed prescribing behavior. Regulatory wins that reduce administration complexity or monitoring burden deliver outsized commercial benefit.

- Supply-chain complexity limits commoditization: distribution and handling requirements for certain agents create effective barriers to generic entry and complicate inventory planning for hospitals and specialty pharmacies.

For executives, these frictions translate into concrete imperatives: design evidence packages that shorten PA timelines; invest in integrated patient-support programs to manage monitoring requirements; and secure redundant manufacturing and distribution options before launch.

How leaders should use this research in 2026 planning

Below are direct, high‑impact uses of the full report for commercial, clinical development, and corporate strategy teams:

- Launch sequencing and resource allocation — use the forecast scenarios to determine where to concentrate salesforce and medical affairs hires in the first 24 months post-approval, and to size inventory buffers to avoid missed treatment windows.

- Pricing and contracting — leverage modeled payer willingness-to-pay thresholds and total-cost-of-care analyses to craft indication-specific pricing and outcomes-based contract terms that shorten time-to-listing.

- Clinical development prioritization — align Phase II/III designs with payer evidence needs highlighted in the report, particularly around early functional outcomes and RWE endpoints that accelerate coverage decisions.

- M&A and partnering — prioritize targets that solve one of the four structural frictions (monitoring, prior authorization, formulation complexity, or supply resilience); the report’s target screening tool ranks candidates by strategic fit and integration risk.

- Risk mitigation and compliance — adopt the supply-chain and certification checklists to reduce the risk of launch delays and to meet the ophthalmologic monitoring obligations tied to some compounds.

What leaders will miss by not using this study

Absent a concentrated, market-specific intelligence product, organizations risk four avoidable missteps in 2026:

- Over-investing in field coverage where access barriers make rapid uptake unlikely;

- Under-estimating the budgetary impact of monitoring and treatment costs on formulary negotiations;

- Failing to time regulatory and payer engagements around clinical readouts that materially affect early-adopter prescribing; and

- Overlooking supply-chain design choices that defend against generics and ensure uninterrupted hospital access.

Next steps — how to convert insight into action

For executives preparing 2026 investment cases, PW Consulting recommends three immediate actions informed by the study:

- Run a 90-day launch readiness workshop that maps clinical evidence to payer requirements and creates a prioritized RWE plan;

- Execute a supply-chain diagnostic to identify single-point failures and initiate contingency manufacturing agreements ahead of pivotal launches;

- Engage in early payer and HTA dialogues informed by our reimbursement simulations to compress prior-authorization timelines and protect early-window patient access.

Our full report contains the granular, proprietary inputs that make these actions executable: probability-weighted revenue models, product-level adoption curves, detailed payer dossier templates, and a ranked universe of strategic targets and partnership profiles. This preview intentionally omits segment-level splits and the line-item financials that drive our proprietary valuations — information we reserve for clients and subscribers who access the complete study.

Final note — a timely, high-value intelligence asset

With the market projected to grow steadily through 2032 and recent clinical and regulatory events changing the commercial calculus, 2026 is a pivotal planning year. The right combination of evidence generation, payer engagement, and supply resilience will determine which organizations convert small-patient, high-cost markets into durable, defensible franchises. PW Consulting’s full Infantile Spasms Therapeutics Market report provides the tactical playbooks and quantitative models that make those strategic bets repeatable and measurable.

To access the full dataset, segment-level forecasts, and executable commercial templates referenced in this preview, visit our report page or contact PW Consulting’s life sciences strategy team for a guided briefing.

For detailed analysis of this topic, please visit the official page:Infantile Spasms Therapeutics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com