Dental Air Abrasion Market Expected to Surpass US$123.3 Mn by 2031 Amid Rising Demand for Minimally Invasive Dental Procedures

Networking |

2026-07-08 10:26:33

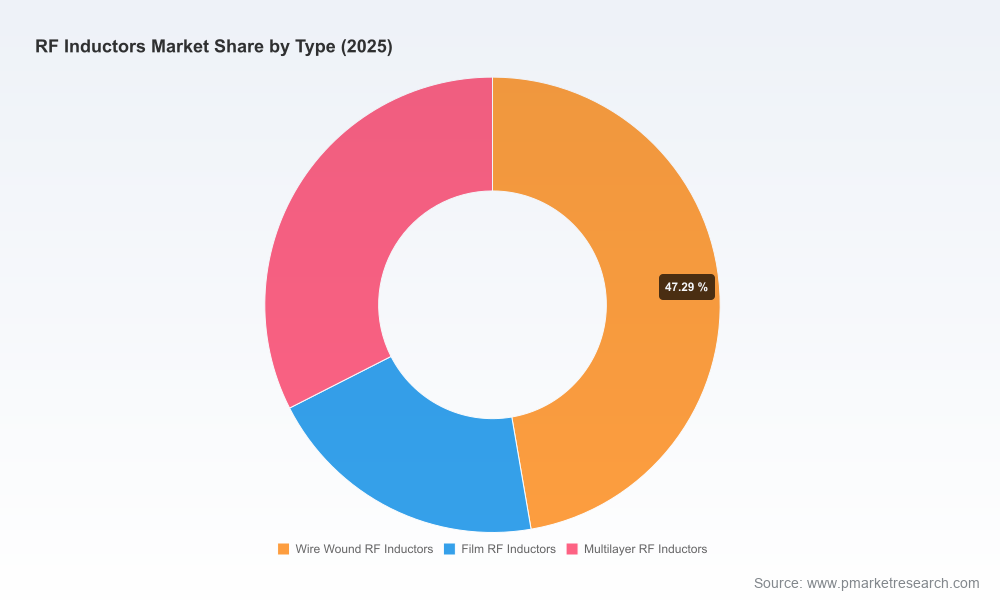

As companies set strategy for 2026, the RF inductors market is neither a niche replacement business nor a solved commodity market — it is an inflection point. PW Consulting’s latest market study (base year 2025, historical window 2020–2025, forecast 2026–2032) shows a steady multi-year expansion that demands nuanced, execution-ready responses from product leaders, supply-chain strategists, and corporate development teams. The global market, measured in USD millions, has grown consistently from the early-2020s and our model projects continued expansion through 2032 at a compound annual growth rate of approximately 4.97% — creating both runway and pressure for differentiation.

RF Inductors Market

Our analysis synthesizes demand-side shifts and supply-side constraints into a concise strategic view. Key drivers include the widespread rollout of higher-frequency wireless technologies (including 5G and mmWave use cases), persistent requirements for miniaturization in mobile and automotive electronics, and the growing importance of in-vehicle connectivity and power-over-coax configurations. On the supply side, capacity expansions, materials cost volatility, and test/qualification lead times for automotive and aerospace customers are shaping vendor economics and time-to-revenue curves.

RF Inductors Market

Between 2020 and 2025 the market exhibited resilient growth despite cyclical pressures; our forecast through 2032 reflects both secular adoption (new RF-enabled vehicle and communications architectures) and the intermittent short-cycle volatility tied to consumer electronics refreshes and infrastructure deployments. This combination creates a market that rewards both product specialization (high-Q, ultra-miniature packages, automotive-grade robustness) and operational excellence (tight inventory management, flexible capacity).

RF Inductors Market

The competitive field is populated by global component leaders and agile regional specialists. Leading Japanese manufacturers continue to push the envelope on ultra-compact multilayer chip inductors and high-Q wire-wound types tailored for automotive and RF front-end modules. Their investments in micro-package variants and automotive-grade product lines reflect strategic bets on in-vehicle connectivity and high-frequency consumer devices.

North American and European specialists are reinforcing positions in high-reliability, defense and telecom verticals with air-core and ceramic-core technologies, while several Taiwan-based and other Asian manufacturers leverage cost and volume advantages to supply industrial and high-frequency consumer circuits. Across the board, we see a mix of premium engineering-driven offers and cost-competitive SMD (surface-mount device) portfolios.

Notable recent developments underscore the ongoing product refresh cycle. Manufacturers have launched ultra-compact high-frequency chip inductors for automotive proof-of-concept and RF front-end uses, expanded high-current and high-inductance automotive grade chip series, and introduced multilayer and thin-film variants optimized for power-over-coax and 5G use cases. These product introductions are not incremental — they redefine acceptable form factors and performance baselines for system OEMs.

PW Consulting’s research is designed to be operationally actionable. The report contains a suite of decision-ready tools and templates that support 2026 planning cycles:

Operationalize the strategy with a focused set of KPIs: design-win velocity (quarterly), qualification lead-time (months), yield and first-pass success rates (percent), landed cost volatility (rolling 12-month), and customer concentration metrics. Establish a quarterly competitive watch that tracks product launches, capacity announcements, and supply-chain disruptions; these signals are leading indicators of margin compression or opportunity windows.

The full study goes beyond high-level narrative and provides the executable intelligence needed for board-level decision-making and day-to-day commercial operations. Deliverables include:

2026 is a pivotal planning year: it sits at the cusp of mid-cycle demand drivers (5G densification, automotive connectivity rollouts) and the mature, structural shifts toward miniaturization and higher-frequency operation. The market’s projected multi-year growth trajectory and the competitive activity we observe — characterized by targeted product launches and an emphasis on compact, high-Q solutions — create a landscape where deliberate, data-backed choices will separate winners from the rest.

PW Consulting’s RF Inductors Market study is designed to be the strategic companion for those choices: grounding 2026 decisions in rigorous historical analytics, forward-looking scenarios, and practical execution roadmaps. For teams preparing budgets, redesigning product families, or evaluating M&A targets in 2026, the intelligence in this report reduces uncertainty and accelerates time-to-value.

To access the full intelligence — detailed model outputs, granular vendor profiles, and the operational toolkits that underpin the recommendations above — please consult the full PW Consulting report page. The summary here highlights the most consequential strategic insights while reserving the detailed, actionable segment data and model spreadsheets for the full publication.

For detailed analysis of this topic, please visit the official page:RF Inductors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com