Payday Loans Service Market Growth Trends and Forecast to 2034

Other |

2026-06-24 13:50:09

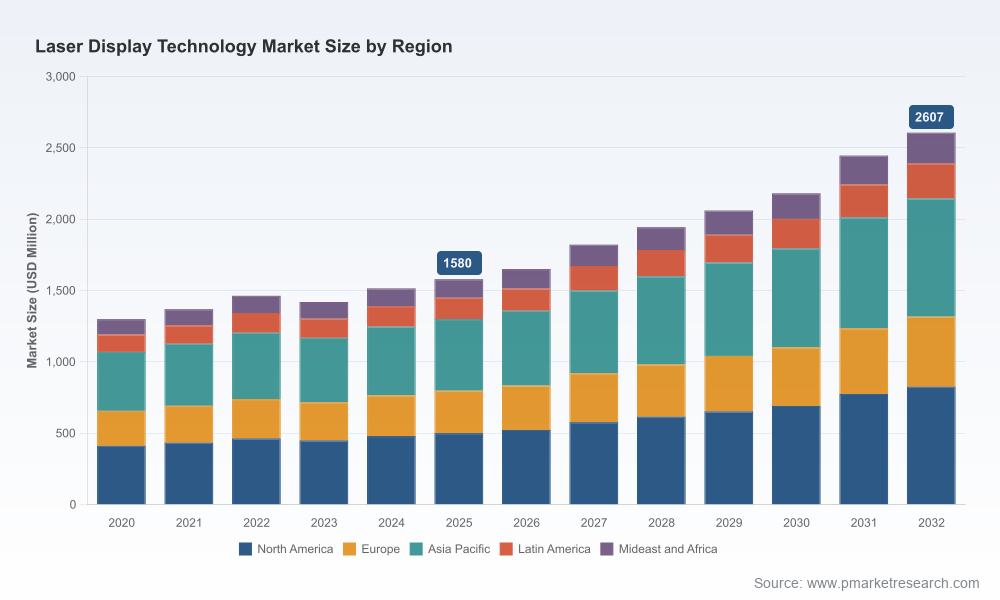

The laser display market has entered a maturation phase characterized by steady expansion, accelerated product innovation, and an increasingly complex regulatory backdrop. From a market size of approximately USD 1.58 billion in the 2025 base year, our forecast shows a continuation of multi-year growth at a compound annual growth rate of 7.45% across the 2026–2032 forecast window, with the market approaching an expected USD 2.6 billion by 2032. The trajectory since 2020 demonstrates resilience — early-decade growth, a transient contraction, and a robust recovery driven by new product classes and venue-scale adoption — signaling sustained commercial opportunity for incumbents and new entrants alike.

Laser Display Technology Market

Timing and resource allocation: With growth compounding through 2032, 2026 is a pivot year for firms deciding whether to accelerate investment in laser light-source R&D, expand manufacturing capacity, or pursue inorganic options. The report quantifies market scale and near-term growth windows to prioritize capital deployment across R&D, production, and go-to-market.

Laser Display Technology Market

Risk-adjusted pathfinding: Emerging regulatory requirements and evolving safety standards are redefining product compliance and cross-border trade risk. Executives must align product roadmaps with compliance roadmaps to avoid market access delays, detention risk at import, or costly retrofits.

Laser Display Technology Market

Competitive positioning: The market exhibits moderate concentration — a small group of global players capture meaningful share, while the remainder is fragmented across regional specialists and technology-focused OEMs. That competitive structure favors targeted alliances, selective vertical integration, and surgical M&A rather than broadscale consolidation.

Technology diversification and product segmentation: Laser display offerings span several light-source technologies and optical architectures — each with distinct performance, cost, and service profiles. Suppliers that match technology choice to high-value end markets (e.g., cinema, simulation, large-venue signage, and ultra-short-throw consumer systems) capture superior pricing and aftermarket revenue.

Innovation vectors: Recent industry activity highlights three near-term innovation vectors — lumen efficiency and thermal management, contrast and black-level enhancement, and compact optics for ultra-short-throw deployments. These vectors are already influencing specification-led procurements in professional and premium consumer segments.

Regulatory and standards inflection: New and updated standards covering medical/aesthetic optical radiation, labeling and testing of protective equipment, and tightened import enforcement are in force or coming soon. Organizations that embed compliance engineering, pre-market self-certification workflows, and supply-chain traceability into product development will reduce time-to-market and avoid expensive remediation.

Channel and ecosystem economics: Value is shifting from hardware-only sales to platform-based models combining hardware, image-processing IP, software features, and recurring services (calibration, warranty, content). Firms that build or partner into aftercare and software ecosystems increase lifetime customer value and create sticky revenue streams.

Sony Group Corporation — Strengths: premium optical IP, deep systems integration capability, and strong brand value in cinematic and consumer premium segments. Strategic play: leverage proprietary light-source R&D and cinematic-grade contrast improvements to defend premium pricing and create licensing opportunities for content delivery partners.

Seiko Epson Corporation — Strengths: broad projector portfolio and distribution reach across business, education, and home segments. Strategic play: pursue ultra-short-throw and workspace-focused deployments where form factor and installation simplicity matter, while optimizing manufacturing scale for cost leadership.

Barco NV — Strengths: focus on large-venue, cinema, and simulation markets with high-brightness engineered solutions and advanced image processing platforms. Strategic play: bundle premium service agreements and expand vertical proofs of concept (e.g., simulation and themed entertainment) to capture high-margin system contracts.

Hisense Group & Appotronics and Chinese systems specialists — Strengths: rapid productization of laser TV and ultra-short-throw consumer categories, plus semiconductor laser light-source innovations (e.g., ALPD). Strategic play: drive scale through consumer channels while selectively migrating successful consumer optics to professional variants.

Specialist vendors (e.g., Pangolin, AVIC Guohua, LDT) — Strengths: niche expertise in show control, scanning, and professional opto-mechanical subsystems. Strategic play: provide modular subsystems and software integration offerings to larger OEMs, or position for acquisition as larger vendors seek to internalize capabilities.

Advances in cooling and durability (e.g., new liquid-cooling projector platforms) reduce total cost of ownership in demanding installations and extend operational windows for 24/7 applications such as control rooms and live events.

Ultra-short-throw projector launches for modern workspaces lower installation friction and create new uptake in retail, collaborative offices, and higher-education deployments where floor space is constrained.

Proprietary light-source breakthroughs targeting black-level and contrast improvement are re-opening cinematic and premium visualization budgets; this favors suppliers who control both optical engine and image-processing stacks.

Major exhibitors and integrators showcasing next-generation projection engines at global events signal an acceleration of refresh cycles at cinema and themed-entertainment venues — an early revenue opportunity for qualified OEMs and integrators.

Product compliance is no longer a peripheral cost. New and updated standards for optical radiation, testing and labeling, and exhibition safety raise baseline design and testing requirements. Non-compliant imports face detention risk under targeted import alerts.

For companies selling into medical, aesthetic, and exhibition markets, proactive alignment with region-specific standards and pre-certified test reports will shorten contracting cycles and support premium positioning.

Regulatory complexity favors early investment in in-house compliance capabilities or long-term partnerships with accredited test labs, rather than ad-hoc third-party testing late in the development cycle.

Re-scope R&D portfolios to prioritize high-differentiation features (thermal management, contrast optimization, and compact optics) that map to target verticals with the strongest willingness-to-pay.

Operationalize compliance-first product development: embed regulatory checkpoints into stage-gate reviews, and establish traceable documentation to mitigate import and market access risk.

Define a two-track go-to-market approach: (1) platform plays for system integrators and venue-scale customers with recurring service contracts; (2) productized bundles for scale channels (education, SMB, consumer) optimized for cost and installation speed.

Pursue targeted M&A or partnerships for critical subsystem capabilities (image processing IP, scanning and show-control software, or proprietary light-source modules) to accelerate time-to-market and preserve margin.

Hedge supply-chain exposure by qualifying dual sources for key laser-diodes and optics, and by developing predictive inventory buffers tied to lead-time volatility scenarios.

Monetize software and service: introduce tiered service offerings (remote calibration, content management, extended warranties) to increase post-sale revenue and customer stickiness.

Market sizing and rigorously modeled forecasts (base year 2025, historical 2020–2025, forecast 2026–2032) that support scenario planning and investment prioritization.

Technology and product taxonomy with performance, cost, and commercialization readiness assessments to guide R&D and product roadmaps.

Regulatory and standards matrix (global and regional) with compliance checklists, certification pathways, and estimated time-to-compliance for critical certifications.

Competitive landscaping and vendor scorecards, including capability gaps and acquisition targets, to inform partnership and M&A strategies.

Go-to-market playbooks by vertical, channel, and product-class — including pricing strategy frameworks, commercial terms templates, and service monetization levers.

Supply-chain risk map and recommended mitigation playbook: dual-sourcing options, inventory strategies, and contract negotiation blueprints.

Financial models and unit-economics templates that allow users to stress-test investments under different adoption curves, margin scenarios, and regulatory cost assumptions.

For executives and investors making allocation decisions in 2026, the laser display market offers a clear, measurable growth runway underpinned by technology-driven refresh cycles and new usage contexts. However, success depends less on raw market size and more on how organizations manage compliance risk, convert feature superiority into reproducible manufacturing, and monetize beyond the initial hardware sale. The coming 18–36 months will separate players who merely supply components from those who own platform value and recurring revenue.

This briefing is a strategic “trailer” designed to surface the analytical thesis and the operational levers that matter in 2026. The full PW Consulting Laser Display Technology Market report contains the detailed subsegment analyses, modeled scenarios, vendor scorecards, and executable templates referenced above. For access to the complete dataset, proprietary segmentation, and the tools to convert insight into an action plan, please consult the full report.

For detailed analysis of this topic, please visit the official page:Laser Display Technology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com