Vacation Ownership (Timeshare) Market 2026 Preview: Strategic Imperatives for Corporate Decision‑Makers

As vacation ownership re-emerges from the pandemic-era reset into a structurally healthier growth path, senior executives and corporate strategists must recalibrate portfolio, distribution, and capital-allocation choices for the next planning cycle. PW Consulting’s forthcoming Vacation Ownership (Timeshare) Market study—anchored on a 2025 base year and a 2026–2032 forecast horizon—distills the market forces that will shape winners and losers through 2032. The market we model grows at a compound annual growth rate of 7.2% and moves from a 2025 baseline to materially larger volumes by the end of the forecast period. This introduction maps the top-line dynamics, competitive positioning, and actionable use cases where the research delivers immediate decision support for 2026.

Vacation Ownership (Timeshare) Market

Why 2026 Is a Strategic Inflection Point

- Macro–micro alignment: The market’s mid-single-digit-plus CAGR masks a structural transition from product-led timeshare propositions to service- and membership-led ownership ecosystems. Executives who see beyond unit sales to lifetime-owner economics will capture disproportionate value.

- Capital-market readiness: Leading public players continue to monetize scale through diversified revenue streams (membership tiers, exchange programs, third-party management). The 2025 corporate results and public filings we synthesize signal that access to liquidity and capital for development will be more contingent on proven owner-retention economics than on footprint expansion alone.

- Regulatory and financing constraints: Consumer finance, anti-corruption, and disclosure regimes are tightening in key jurisdictions. This changes the calculus for financing product innovation and secondary-market activities—both core themes of the report.

Top‑line Market Trajectory (What the Numbers Tell Us)

Our model—built from 2020–2025 historicals and extended through 2032—captures a steady recovery and expansion trend. From the 2025 base year, the model projects continued growth driven by rising owner families, higher occupancies in owner-stays versus comparable transient lodging, and an expanding set of ownership product designs and membership experiences. The headline growth rate (7.2% CAGR) implies that the aggregate market size in the forecast end-year is materially larger than today, creating pockets of scalable opportunity across development, exchange platforms, and ancillary services.

Vacation Ownership (Timeshare) Market

Important: this introduction synthesizes the directional implications of the sizing and trajectory. The full study contains the granular regional, product and application splits, detailed unit economics and three-layered scenario outputs—data we intentionally reserve for the full report to support confidential board-level modeling and transaction diligence.

Vacation Ownership (Timeshare) Market

What the Report Contains — Practical, Deployable Assets

- Robust market sizing and forecast models (2020–2032) with transparent assumptions and sensitivity analyses suitable for integration into corporate financial planning tools.

- Market-structure diagnostics including concentration metrics and segmentation frameworks that explain where pricing power resides and how scale converts into margin.

- Competitive heatmaps and capability matrices for operator, developer, and exchange-platform archetypes—useful for rake-rate design, partner selection, and M&A screening.

- Go‑to‑market playbooks for four strategic moves: premiumization (experience-plus-membership), conversion (hotels-to-ownership), portfolio optimization (asset-light management), and secondary‑market platforms (resale & buyback programs).

- Regulatory and financing playbooks that translate consumer‑finance compliance demands into practical underwriting and servicing controls.

- Ready-to-use diligence checklists and an acquisition target scorecard tailored to vacation ownership assets and businesses, enabling expedited transaction evaluation.

- Appendices with primary-source citations, transaction comps, contract‑sales benchmarks, and an anonymized owner-economics dataset for benchmarking retention, NPS, and lifetime value.

Competitive Landscape — Who Matters and Why

The industry balances legacy hospitality incumbents, stand‑alone vacation ownership specialists, and growing platform-oriented players. Market concentration is material: a small set of large operators controls the majority of channel revenues, creating durable scale advantages in distribution, owner services, and cross-selling.

- Hilton Grand Vacations: A brand-forward operator that has aggressively extended membership layers and experiential access. Recent filings show record sales performance tied to premium-access offerings and elevated membership benefits—evidence that premiumization, when executed with tight owner economics, can expand average contract value while improving retention.

- Marriott Vacations Worldwide: Operates at the intersection of hospitality standards and long-term owner relationships via strategic brand licensing. Its expansion of owner families and resort footprint highlights the ongoing value of exclusive brand alignment in supporting pricing power and broad exchange appeal.

- Travel + Leisure Co.: Reconfiguring itself with acquisitions and corporate consolidation, it is positioning to scale club portfolios and to standardize member experiences across diverse brands—an important playbook for operators seeking to multiply customer lifetime touchpoints.

- Disney Vacation Club: Exemplifies exclusive-experience ownership where IP-driven demand and captive destination ecosystems allow for differentiated pricing and extremely high retention—an archetype for owners of signature destination assets.

- Holiday Inn Club Vacations, Diamond Resorts International, Bluegreen Vacations, Westgate Resorts, Wyndham Hotels & Resorts: These players illustrate variant strategies—from asset-heavy resort portfolios to asset-light management and franchise models—each with different capital intensity and margin profiles. Their competitive moves illuminate tradeoffs between rapid expansion and owner-service scalability.

For dealmakers and strategists, the implication is clear: scale matters for distribution and loyalty economics, but differentiated ownership propositions (IP, tiered experiences, seamless exchange interoperability) create defensible margins—especially when combined with asset‑light servicing or management businesses.

Structural Dynamics and Industry Signals

- Occupancy and Utilization: Owner-stays exhibit significantly higher utilization than comparable transient lodging, underpinning the durability of membership cash flows and ancillary spend pools.

- Supply Pipeline: Development intentions remain active, with industry reports noting a substantive pipeline of units planned for the coming years. That pipeline will compress or expand depending on financing conditions and pre‑sale performance—factors our scenarios explicitly model.

- Finance & Compliance: Consumer-lending rules and anti-corruption frameworks are increasingly consequential for underwriting and cross-border distribution. Firms that institutionalize robust compliance and transparent financing terms will win trust and market access in regulated markets.

- Owner Base Scale: Leading operators report large owner-family counts and multi‑resort portfolios—resources that enable cross-sell, exchange liquidity, and data-driven personalization at scale.

Strategic Questions the Report Answers for 2026 Planning

- Where should capital be allocated between greenfield development, acquisition of operating platforms, or expansion of managed-services lines to maximize risk-adjusted returns over a 5–7 year horizon?

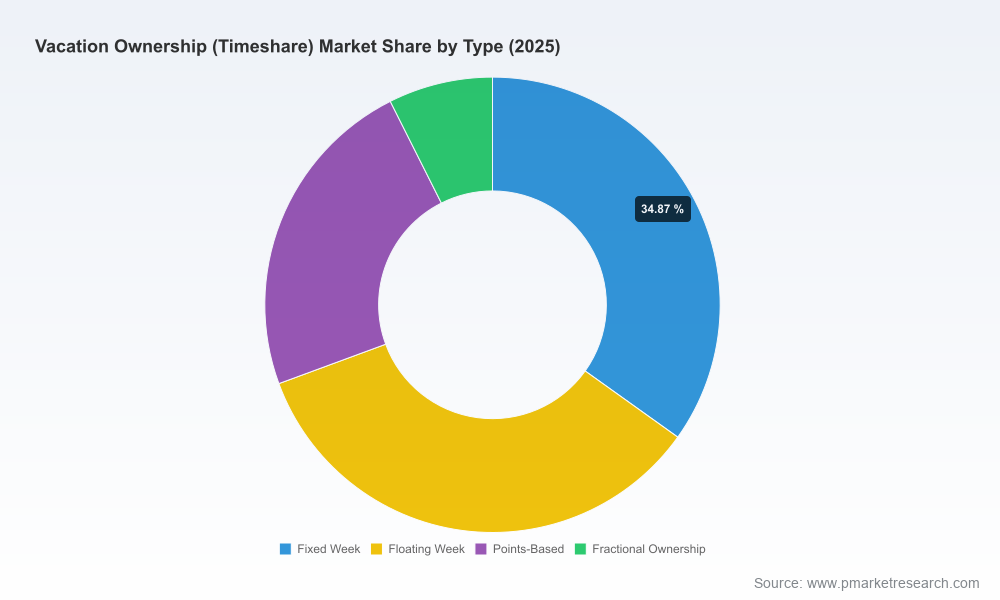

- Which product innovations—points-based models, fractional ownership, or hybrid subscription offerings—deliver the best tradeoff between upfront revenue and long-term recurring cash flows in different market contexts?

- How do regulatory changes around consumer finance and third‑party distribution alter go‑to‑market viability in key jurisdictions, and what operational mitigants should be implemented now?

- Which competitive moat—brand alignment, experience exclusivity, distribution scale, or exchange interoperability—best protects margin expansion in an increasingly consolidated market?

How Leading Firms Are Responding (Illustrative Developments)

- Record contract sales tied to premium, access‑oriented membership layers demonstrate that product upgrading can drive higher conversion and spend per owner when supported by robust fulfillment and inventory access.

- Strategic M&A and HQ investments reveal a trend toward platform centralization and corporate control over member experiences—moves that simplify cross-brand integration and reduce fragmentation costs.

- Public filings and annual reports show operators leaning into owner services, exchange capabilities, and loyalty-integration as key levers to boost lifetime value and de-risk resale pressure.

Decision‑Ready Deliverables and Next Steps

PW Consulting’s full Vacation Ownership (Timeshare) Market study is structured as an executive-grade toolkit for leaders making 2026 strategic commitments. It delivers a fitted financial model, scenario-driven investment cases, M&A screening templates, regulatory impact maps, and a prioritized list of tactical initiatives for commercial and operations teams.

We designed the study as a practical bridge between high-level strategy and execution: C-suite briefings that translate into 90‑day pilots, 12‑month rollouts, and transaction targets that can be evaluated under uniform metrics. The granular regional, product, and application splits—central to board-level strategy and M&A diligence—are contained in the paid report. Those detailed tables and owner‑level datasets are intentionally withheld here to preserve the structured confidentiality and competitive utility required by corporate buyers.

Closing: What Leaders Should Do Now

- Prioritize a short diagnostic: map your current ownership economics against the report’s benchmark LTV/retention bands to identify immediate margin improvement opportunities.

- Stress-test new product propositions (membership tiers, flexible access, resale guarantees) under the report’s scenario suite to quantify capital efficiency and payback horizons.

- Embed compliance and finance guardrails into any expansion plan—early alignment with consumer-lending and anti-corruption standards materially de-risks cross-border and third-party distribution initiatives.

- Use the report’s acquisition scorecard to triage targets that deliver distribution scale or experience IP, rather than simply accretive unit counts.

For decision-makers preparing budgets, M&A pipelines, or product roadmaps for 2026, PW Consulting’s Vacation Ownership study provides the market map, playbooks, and models necessary to act with clarity. To access the complete datasets, regional and application splits, and the full suite of operational templates, please visit the report landing page and download the full study.

For detailed analysis of this topic, please visit the official page:Vacation Ownership (Timeshare) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com