Портреты на заказ методом выжигания огнем по дереву

Other |

2026-02-01 16:08:46

As PW Consulting's lead industry analyst, I present a high-level, action-oriented briefing that frames the strategic value of our full Pyrethroid Market study for corporate decision-making in 2026. This piece synthesizes macro trends, regulatory inflections, competitive posture and supply-side pressure points — while intentionally withholding granular regional and application breakdowns so that commercial teams and M&A sponsors are directed to the full report for transaction-grade detail.

Pyrethroid Market

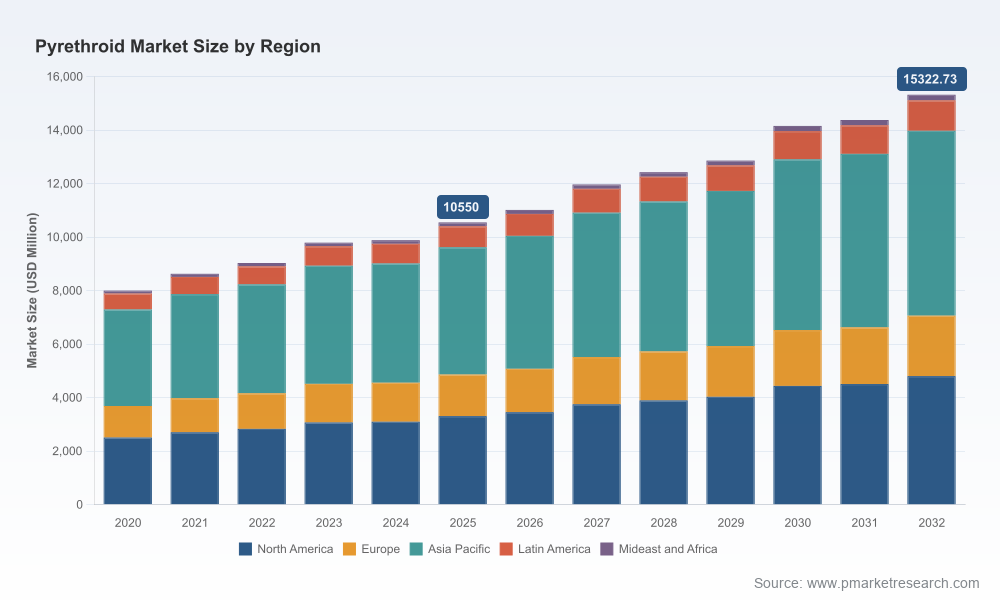

The global pyrethroid market has moved from a recovery phase into a structurally larger and more complex opportunity set. Our base-year analysis shows the market reached USD 10,550 Million in 2025, having grown from USD 8,000 Million in 2020. Under our central forecast the market expands at a compound annual growth rate (CAGR) of 5.5% through 2032, reflecting both continued demand in crop protection and steady requirements in public-health vector control. By the end of our forecast horizon the market passes the mid-teens billion-dollar mark, underscoring meaningful scale for manufacturers, formulators and distributors.

Pyrethroid Market

For senior leaders in ag-chem, specialty chemicals, public-health programs and private equity, that macro trajectory has three immediate implications for 2026:

Pyrethroid Market

Our report goes beyond narrative: it is built for executives who must translate market dynamics into decisions. Key deliverables include:

These outputs are structured to enable rapid decision cycles: whether you are evaluating a buy-side thesis, sizing a new formulation launch, or preparing a global supply-hub strategy for 2026–2028.

Two types of external change are reshaping near-term opportunity sets. First, regulatory developments have become active commercial levers rather than episodic compliance tasks. Notable actions in late 2025 and early 2026 — including final reregistration decisions and new residue tolerances — have the practical effect of altering label usage patterns, increasing compliance costs for registrants and changing the economics of certain post-harvest and specialty uses.

Second, raw-material supply volatility is a persistent source of operating risk. Natural pyrethrins, derived from chrysanthemum extraction, remain a critical feedstock for some formulations. Weather-related disruptions and localized supply shortages have increased spot-price variability and pushed formulators to accelerate dual-sourcing and substitution strategies. These dynamics magnify the advantage of firms that combine formulation know-how with integrated procurement or long-term offtake agreements.

The industry reflects a mid-to-high concentration profile: the top three players control a meaningful share of the market, and the top five raise concentration further. This market structure yields predictable behaviors — price leadership in commoditized channels, differentiated premium positioning in curated formulations, and opportunistic M&A to fill registration or geographic gaps.

How leading players are positioned:

For acquirers or partners, the competitive landscape implies two logical plays: (1) acquire registration depth and distribution to convert commodity active ingredients into margin-accretive formulations; or (2) acquire feedstock/chemical integration to lock-in cost and availability. Our full company profiles and M&A scorecards quantify which targets best match each play.

Based on scenario modeling and desk-to-field validation, Pw Consulting recommends the following priority actions for 2026:

Decision-makers must weigh at least four correlated risks:

Our full report contains probability-weighted scenarios and a risk-adjusted valuation model that quantifies how these exposures change target valuations and capital allocation priorities.

In markets with a 5.5% CAGR and multi-year tailwinds, timing and precision determine value capture. The full Pyrethroid Market study supplies the granular segmentation, regional demand matrices, price histories and company scorecards that transactional and corporate teams need to: prioritize deals, negotiate better warranties, design resilient supply chains and allocate R&D and commercialization budgets with confidence.

We have deliberately kept this briefing high-level to spotlight the strategic implications while reserving the granular, proprietary split-data (regional/application-level revenues, per-product volumes, and confidential company score metrics) for the full report and client briefings. That granular intelligence is what turns market perspective into executable transactions.

For immediate needs in 2026 — whether you are evaluating a buy-side thesis, planning a market-entry, or redesigning procurement strategy — PW Consulting can provide:

Contact PW Consulting to obtain the full report and our interactive modeling tools. The macro view is clear: pyrethroids remain a material market with actionable pockets of margin expansion — but success in 2026 requires calibrated regulatory foresight, supply resilience and disciplined commercial execution.

For detailed analysis of this topic, please visit the official page:Pyrethroid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com