Complete Pest Control Guide

Other |

2026-05-02 09:08:49

As stewards of corporate strategy in animal health, leaders entering 2026 must synthesize a narrow set of high-impact signals into decisive action. Our latest PW Consulting study on the Equine Pharmaceuticals and Supplements market delivers that synthesis: a data-grounded forecast, a pragmatic view of supply-chain and regulatory pressures, and competitor intelligence crafted to inform M&A, product, and commercial choices over the 2026–2032 planning horizon.

Equine Pharmaceuticals and Supplements Market

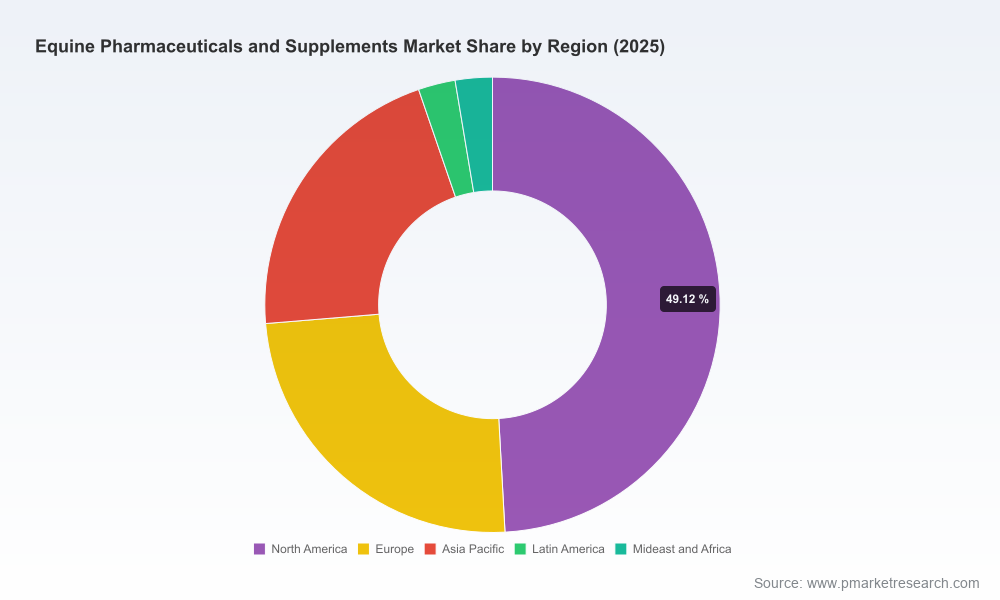

A compact market with steady momentum: Between 2020 and 2025 the equine market grew consistently, and our modeling shows a continuation of that trend into the forecast window (2026–2032) at a compound annual growth rate (CAGR) of 5.98%. For firms evaluating resource allocation, this is not a hyper-growth play but a structurally attractive, resilient segment where disciplined investment is rewarded.

Equine Pharmaceuticals and Supplements Market

Margin and mix implications: The market’s trajectory highlights two practical truths for 2026 planning — product mix and regulatory posture materially influence margins, and incremental gains in market share can outperform greenfield expansion in other animal-health verticals.

Equine Pharmaceuticals and Supplements Market

Timing matters: Recent regulatory and product developments in early 2026 have created new dynamics—introductions of approved generics and bioequivalent formulations are shifting pricing power and opening both risk and opportunity windows for innovators and generic players alike.

Quantitative backbone: historical market sizing (2020–2025), a clear base year (2025), and scenario-based projections through 2032 that translate the 5.98% CAGR into plausibly bounded outcomes for revenue planning and portfolio stress-testing.

Go-to-market playbooks: channel prioritization for veterinary distribution vs. direct-to-owner channels, pricing tactics in a mixed market of regulated pharmaceuticals and largely self-regulated supplements, and promotional levers tied to racing and performance segments.

Regulatory and reimbursement risk maps: including impact analyses for FDA approvals, DSHEA-style supplement governance, and how national equine-sport authority rules can affect claim-making and product adoption.

Supply-chain cost model: detailed line items for raw materials, packaging, and logistics with sensitivity analyses. The model highlights how volatility in key inputs will affect gross margins and suggests hedging and sourcing strategies.

Competitive benchmarking and M&A readiness: profiles of incumbent players, capability gaps, acquisition targets scored by strategic fit, and integration playbooks for 100–300 day post-merger value capture.

Commercial tactics and metric dashboards: customer lifetime value for equine clinics and training operations, channel ROI expectations, and a prioritized metric set for business leaders to track in 2026.

Regulatory inflection: The early-2026 approval of the first FDA-authorized generic for control of clinical signs of Equine Cushing’s signals that portions of the pharmaceutical side of this market are entering a commoditization cycle. For branded innovators, this raises the premium on lifecycle management (new formulations, patent extensions, and evidence generation). For generics and value players, it creates direct opportunities to capture share through cost-competitive listings and formulary placement.

Product launches with strategic implications: The commercial availability of a bioequivalent omeprazole preparation in the U.S. during 2026 demonstrates how regulatory acceptances of bioequivalents shorten windows of exclusivity for established brand leaders and shift procurement dynamics for large veterinary groups and networks.

Cost pressure and margin compression: Input cost trends are real and persistent. Key raw materials have experienced single-digit to low-teens percentage shocks historically, packaging and compliance overheads have risen materially over a multi-year period, and logistics—especially for bulk, temperature-sensitive formulations—constitute a high-teens share of landed product cost. Collectively, these constraints force a 2026 priority: optimize working capital and manufacturing footprint before pursuing margin-accretive investments.

Regulatory asymmetry between segments: While pharmaceuticals follow established approval pathways, supplements broadly operate under self-regulatory frameworks in major markets, leaving manufacturers responsible for substantiation of safety and claims. This asymmetry creates a spectrum of commercial risk: supplements can scale faster but deliver more brand risk exposure; pharmaceuticals require more capital but offer stronger pricing defense.

Our analysis covers the leading global players whose portfolios and capabilities will matter for competitive positioning in 2026:

Zoetis Inc. — Global scale and distribution reach position the company to defend premium therapeutic franchises and to accelerate the commercialization of novel biologics or diagnostics targeted at performance and chronic-care segments. Strategic emphasis: sustaining vet channel loyalty and clinical evidence programs.

Dechra Pharmaceuticals — A specialist-oriented approach and strong presence in regulated equine therapeutics create opportunities in endocrine and chronic-disease niches. Strategic emphasis: leverage specialty reputation for premium pricing and targeted clinical engagement.

Boehringer Ingelheim Animal Health — Broad R&D capabilities and vaccine expertise make the firm a key player for preventive health investments and integrated herd-level solutions for high-value equine operations. Strategic emphasis: cross-selling bundled preventive and therapeutic offerings.

Merck Animal Health — Research intensity and global scale allow the firm to play both innovation and access roles, especially for formulations requiring significant clinical evidence. Strategic emphasis: invest in next-wave therapeutic modalities and data-driven outcomes studies.

Elanco Animal Health — A commercial focus on efficient product rollouts and partnerships gives Elanco flexibility to pursue cost leadership or targeted niche entries. Strategic emphasis: channel partnerships and contract manufacturing optimization.

Norbrook Laboratories — Known for value-priced injectables and generic-equivalent products, Norbrook is positioned to capture share as generics and biosimilars expand. Strategic emphasis: scale supply chain and secure distribution plug-ins with key veterinary networks.

Virbac Animal Health — A strong vet-facing brand with a suite of therapeutic and preventive products; Virbac can amplify claims with targeted field data collection. Strategic emphasis: veterinarian education and loyalty programs.

Vetoquinol — Therapeutics-focused with strengths in regional markets and clinical support for clinics and performance stables. Strategic emphasis: deepen clinical service offerings and local regulatory expertise.

Bimeda — Recent 2026 U.S. launch of an FDA-recognized bioequivalent omeprazole product demonstrates its intent to compete aggressively on generics and bioequivalents. Strategic emphasis: aggressive entry strategies in high-volume therapeutic classes.

Ceva Santé Animale — Strong in companion and production-animal segments, Ceva’s equine play leverages technical service and international market access. Strategic emphasis: export-led growth and technical-support differentiation.

Prioritize portfolio clarity: Differentiate between assets that benefit from evidence-driven, high-barrier commercialization (pharmaceuticals) and those that require brand trust and marketing velocity (supplements). Allocate R&D and commercialization resources accordingly.

Hedge input-cost risk: Lock predictable supply for key ingredients, evaluate forward-purchase agreements for volatiles, and explore near-shore or co-manufacturing options to blunt logistics and packaging inflation.

Prepare for generics competition: For molecules facing generic entry, accelerate lifecycle strategies (new formulations, combination products, or complementary diagnostics) and build defensive pricing playbooks for major veterinary buying groups.

Invest in real-world evidence (RWE): For both brand therapeutics and premium supplements, real-world outcome data from stables, race tracks, and clinical networks will become a decisive commercial asset in 2026 and beyond.

Explore bolt-on M&A: Given a moderately concentrated incumbent base and fragmented mid-market, targeted acquisitions can deliver rapid access to formulations, registrations, or regional distribution—particularly attractive to firms seeking scale in a non-explosive growth environment.

Refine channel economics: Revisit margins paid to distributors, evaluate direct-to-clinic programs, and pilot direct-to-consumer education platforms where permissible—each can materially affect unit economics.

In this executive overview we surface the signals decision-makers need to act in 2026, but we have deliberately omitted granular region- and application-level breakdowns and detailed revenue-by-segment tables. Those granular splits are central to tactical planning (e.g., regional market-entry sequencing, SKU-level pricing, and targeted promotional spend), and they are included in full in the comprehensive report and supporting datasets available through our report portal. If your 2026 play requires that level of operational precision, the full dataset and our advisory services will accelerate execution and de-risk implementation.

Use this briefing as a strategic lens: align portfolio investment, supply-chain resilience, and commercial model adjustments to the five-to-seven-year horizon mapped by our CAGR-informed scenarios. For boards and executive teams, the practical next steps in 2026 are straightforward—prioritize defensive moves where regulatory-driven commoditization is measurable, and invest selectively where higher barriers to entry and evidence-based differentiation preserve margin. Our full report provides the detailed inputs, playbooks, and transaction-ready analysis to convert these priorities into a 100–300 day roadmap.

To access the full report, segmented datasets, and bespoke strategic advisory options, please visit the PW Consulting report page for the Equine Pharmaceuticals and Supplements Market. The complete materials include downloadable models, company scorecards, and a 90-day implementation checklist tailored for 2026 execution.

For detailed analysis of this topic, please visit the official page:Equine Pharmaceuticals and Supplements Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com