Night Vision Devices Market — Strategic Preview for 2026 Decision-Makers

Executive snapshot

As PW Consulting’s Senior Strategic Advisor, I present a concise, decision-focused preview of our full Night Vision Devices Market study. Between 2020 and 2025 the global market expanded from USD 6,500 Million to USD 8,500 Million (base year 2025). With a compound annual growth rate (CAGR) of 8.5% projected over the 2026–2032 forecast window, the market is on a trajectory to roughly double in scale by the end of the forecast period. This growth is neither uniform nor risk-free: it is driven by a confluence of defense modernisation, homeland security investments, and commercial surveillance adoption, while being constrained by export controls and key component supply shortages.

Night Vision Devices Market

Why this study matters for 2026 strategic decisions

- Timing: 2026 is a turning point for procurement cycles and platform upgrades across leading militaries; early movers who align product roadmaps and procurement strategies now will capture disproportionate share of upgrade budgets.

- Risk management: Material supply bottlenecks and tightened export controls mean sourcing and compliance strategies are as important as product performance. The study equips procurement and supply-chain leaders with scenarios to mitigate delivery and regulatory risk.

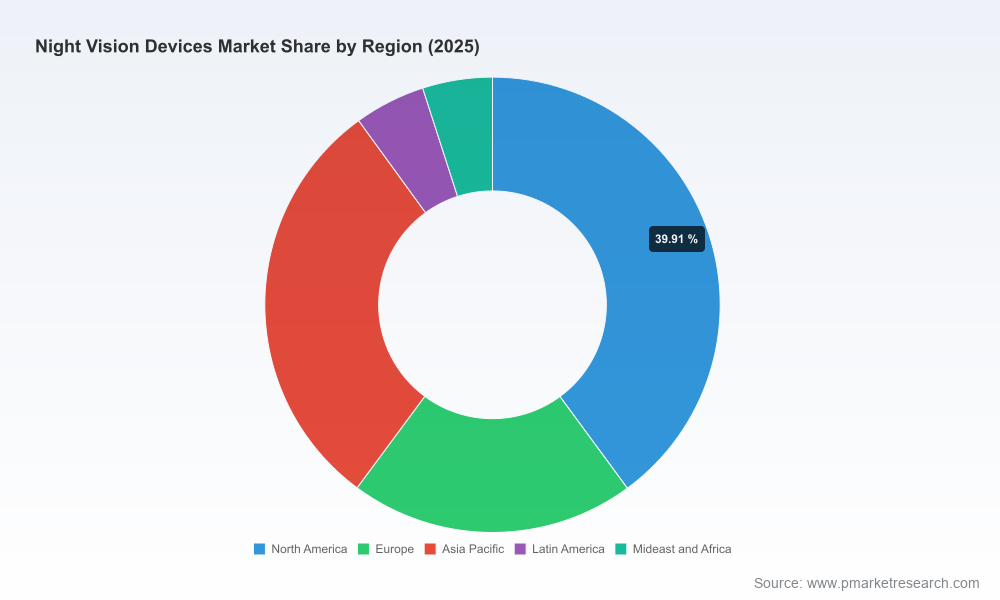

- Value capture: With market concentration still meaningful among the top vendors (CR3 ~48%, CR5 ~54%), well-timed partnerships, M&A, or technology bets can unlock asymmetric returns. Our analysis highlights where competition is fierce and where white space remains.

Market trajectory and what the headline numbers conceal

The headline figures—USD 8,500 Million in 2025 expanding at an 8.5% CAGR through 2032—signal healthy demand. But beneath that topline lie three structural dynamics that will determine winners and losers in 2026:

Night Vision Devices Market

- Defense modernization vs. commercialisation: Military and public-safety procurement remains the primary demand engine, yet commercial surveillance and industrial applications are increasing both unit volumes and expectations for sensor fusion and analytics.

- Platform convergence: Buyers increasingly expect integrated solutions—night vision fused with thermal, augmented reality overlays, and networked sensors—reshaping product roadmaps and supplier selection criteria.

- Supply chain and component scarcity: Production of high-performance image intensifiers depends on constrained substrates and legacy manufacturing capacity. This creates delivery risk and a premium for suppliers who can secure capacity.

Regulatory and supply-side constraints

Night vision devices remain dual-use products subject to tight controls. In the United States, ITAR classification dominates export authorisations; in Europe, export restrictions create accessibility limitations for certain end-markets. Enforcement actions in recent years demonstrate real legal and commercial risk for non-compliant exports. Additionally, a concentrated, geopolitically sensitive supply of gallium arsenide wafers used in Generation III photocathode fabrication represents a material production risk. Meanwhile, defence customers and governments are actively funding supply-chain resilience efforts—an important demand lever for vendors who can demonstrate secure sourcing.

Night Vision Devices Market

Competitive landscape — what to watch in 2026

The market combines global primes with specialised optics firms. Our study profiles incumbent suppliers and rising challengers across technology, customer access, and manufacturing capabilities. Key companies highlighted include:

- L3Harris Technologies — Known for binocular systems such as the NOVA™ helmet-mounted binoculars and the company’s priority position on major Binocular Night Observation Device procurements. Recent product launches and program wins in early 2026 have increased its strategic momentum.

- Elbit Systems of America — A major supplier of enhanced night-vision binoculars with entrenched program relationships; continuing delivery orders keep it central to U.S. modernization efforts.

- Teledyne FLIR — Strong in thermal modules and fleet night-vision sensors; increasingly important where thermal-imaging fusion is required for fixed and mobile platforms.

- Thales Group, Hensoldt, Senop Oy — European leaders with deep aerospace and defence integration experience; they are particularly relevant where export and partnership dynamics favour regional suppliers.

- Specialised U.S. and niche manufacturers — Firms such as Night Vision Devices, Inc., AGM Global Vision, and Nivisys supply MIL‑SPEC image intensifiers, monoculars, and tactical systems that feed both military and law‑enforcement funnels.

Recent industry moves—product launches, multi-year procurement awards, and regional framework agreements—have reshaped competitive positioning in early 2026. The study assesses competitive strengths across product modularity, manufacturing scale, integration capabilities, and compliance posture.

Strategic implications by function

- Executive leadership: Prioritise portfolio bets that move beyond single-component sales to integrated sensing solutions and lifecycle services. The market premium for systems-level suppliers will widen as customers prefer turnkey deliveries with assured supply chains.

- Product & engineering: Accelerate modular designs that enable thermal-intensifier fusion and open architectures for software upgrades. Roadmaps should account for obsolescence of legacy tubes and the expected shift to hybrid sensors.

- Supply chain & procurement: Build dual-sourcing strategies for critical substrates and negotiate long-lead capacity agreements. Scenario planning for wafer constraints and quality-controlled stockpiles will reduce schedule and contractual risk.

- Commercial & BD: Leverage thesis-driven targeting—identify pockets of white space where platform integration or local production confers commercial advantage. Partnerships with systems integrators and local manufacturing hubs will open restricted markets.

- Legal & compliance: Invest in export-control capability and transaction screening. Non-compliance has material financial and reputational consequences; compliance capability will be a competitive differentiator in international tenders.

Report contents — what you will find in the full PW Consulting analysis

Our comprehensive study is built for executives who need both strategic context and actionable steps. The full report contains:

- Topline market sizing and a reconciled historical series (2020–2025) plus a transparent model for the 2026–2032 forecast horizon (USD Million, base year 2025).

- Demand-driver analysis by end-use and procurement cycle modelling that maps purchase windows and obsolescence timelines.

- Competitive positioning matrices and capability heatmaps for the leading suppliers, benchmarking product portfolios, program wins, and integration depth.

- Supply-chain stress-testing scenarios: constrained substrates, regulatory shocks, and mitigation pathways that include localised manufacturing and strategic inventory.

- Commercial playbooks: go-to-market approaches for defence primes, law-enforcement tenders, and commercial surveillance buyers, plus pricing strategy guidance under different procurement regimes.

- M&A and partnership screening: target profiles, valuation heuristics, and integration risk checklists designed for acquirers and private-equity sponsors.

- Policy and compliance dossier: a practical guide to export control regimes, licensing pathways, and due-diligence templates tailored to night-vision technologies.

- Decision-ready appendices: sourcing scorecards, RFP templates, and a vendor short-listing tool that executives can apply immediately.

How to use this research in 90 days

- 90-day procurement sprint: Use the supply-chain scenarios to secure contingent capacity and revise delivery SLAs for existing contracts.

- Product roadmap triage: Prioritise modules that enable sensor fusion and open APIs; de-prioritise legacy-only tube upgrades that face component scarcity.

- Commercial acceleration: Initiate two strategic pilot partnerships—one with a systems integrator for platform-level integration and one with a regional manufacturer for market access under export constraints.

- M&A diligence: Run a rapid-screen shortlist of acquisition or investment targets that complement your manufacturing or integration gaps; our checklist reduces diligence time and highlights regulatory red flags.

Conclusion — the strategic choice for 2026

For organisations active in or adjacent to the night-vision ecosystem, 2026 is a year for decisive action. The macro numbers—an industry base of USD 8,500 Million in 2025 and an 8.5% CAGR—point to substantial upside, but the path to capture that upside is narrow. Companies that align product modularity, secure supply of critical components, and demonstrate robust compliance will outpace competitors. Equally, governments and large buyers that invest in supply-chain resilience and clear export-track policies will unlock both industrial capacity and strategic autonomy.

Next step

PW Consulting’s full Night Vision Devices Market report contains the underlying data, segment-level forecasts, and the operational tools referenced above. The preview you’ve read is intentionally curated to demonstrate our analytical depth while reserving the proprietary granular segmentation and scenario outputs for report subscribers. Contact PW Consulting for access and a tailored briefing that maps the insights in this study to your 2026 strategic plan.

For detailed analysis of this topic, please visit the official page:Night Vision Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com