Middle East and Africa Sulfuric Acid Market Dynamics: Key Drivers and Restraints

Other |

2026-05-27 07:43:30

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a condensed but incisive introduction to our Curing Bladder Market study designed specifically to inform executive decision-making in 2026. The global curing bladder market is a mature, engineering-driven industrial niche that is nevertheless undergoing a renewed wave of product, process and supply-chain transformation. Anchored to a 2025 base year and modelled through 2032, our forecast shows a steady compound annual growth rate of 5.1% and a clear recovery and acceleration path from the 2020 baseline. The result: a market that moved from a sub‑billion-dollar scale early in the decade to well over a billion USD in 2025, and projected to climb toward the mid‑teens of hundreds of millions by the end of the forecast horizon. This trajectory matters for boardrooms contemplating capacity, procurement, R&D investments or M&A in 2026.

Curing Bladder Market

Efficiency and cycle-time pressure. Tire manufacturers continue to push for shorter cure cycles and higher throughput without compromising quality. Material innovations that reduce vulcanization time or improve heat transfer translate directly into factory-level productivity gains — and therefore become strategic differentiators for both bladder suppliers and their OEM customers.

Curing Bladder Market

Technology and digitalization. The integration of RFID, sensors and production analytics into curing bladders has moved from pilot projects to scaled deployments. Traceability, predictive maintenance and cure‑process optimization are becoming procurement criteria rather than optional features.

Curing Bladder Market

Material science as a margin lever. Proprietary elastomer formulations, halobutyl variants and ultra‑high thermal conductive compounds change the performance calculus for both bias and radial curatives. Suppliers who can demonstrably shorten effective cure time command pricing power and preferred‑supplier status.

Supply-side consolidation and regional dynamics. The market exhibits moderate concentration at the top (our model identifies a three‑firm concentration that captures a material share of spend and a five‑firm group that controls the lion’s share of advanced, high-value products). This concentration has implications for negotiating leverage, lead times and access to innovation pathways.

Manufacturing footprint choices. Capital decisions on presses, elastomer blending capacity and regional installations are now evaluated against a 7‑ to 10‑year horizon. Minor gains in per‑cure time compound into meaningful returns when scaled across millions of cures per year.

Lanxess (Cologne, Germany) — Product‑innovation leader: Lanxess’s Rhenoshape® line has become a reference point for high‑performance rubber compounds that prioritise thermal endurance and cycle reduction. Investment in injection‑press capacity in North America and the 2025 launch of an ultra‑high heat‑conductive compound show a go‑to‑market strategy that couples materials IP with regional supply resilience. For corporates, Lanxess represents a partner that can deliver both product advance and localized production throughput.

Continental (Hannover, Germany) — Digitally enabled OEM supplier: Continental’s Conti Bladders, enhanced with RFID and embedded sensors, underline the market’s shift toward digital traceability and process control. The technology has moved well beyond lab validation into real production sites, reinforcing the case for bladders as both hardware and data platforms that enable continuous improvement in cure quality.

Polymer Industrial Products Company, LLC (Searcy, Arkansas, USA) — Specialized manufacturing and formulation tailoring: As an independent US manufacturer, Polymer Industrial Products focuses on proprietary elastomeric formulations for a broad set of tire applications. Its positioning highlights the enduring market for specialized, application‑tailored bladder solutions and the importance of close engineering collaboration with OEMs and tier suppliers.

Shandong Xishui Yongyi Rubber (Guangrao, China) — Scale and breadth: With extensive specification breadth across motorcycle, passenger and commercial tires, large-scale Chinese producers remain critical to global supply chains, particularly where units and specification diversity matter. Their manufacturing scale supports cost competitiveness and rapid delivery for high‑volume programmes.

Tyre Bladder Company Limited (Qingdao, China) — Niche high‑quality specialist: Smaller specialist manufacturers continue to carve durable niches supplying agricultural, industrial and bespoke applications where performance and customization trump pure price competition.

Taken together, the competitive set reflects a market where IP‑driven materials innovation, digital enablement and manufacturing scale each confer distinct competitive advantages. PW Consulting’s market concentration metrics indicate a moderate top‑end control that tilts bargaining power toward established incumbents for advanced products, while leaving room for niche and regional suppliers to win on customization, lead time and cost.

Our full study is structured to be directly actionable for strategy, procurement, R&D and M&A teams. Key practical modules include:

Validated market model and top‑line forecasts (2020–2032) with scenario variants for demand shocks, technology adoption curves and raw‑material volatility.

Supply‑chain and cost‑of‑goods (COGS) modelling — factory‑level cost drivers, capex benchmarks for press and mixing lines, and unit economics sensitivity to cure‑time improvements.

Supplier benchmarking matrix — capability, geographic footprint, IP assets, quality certifications, and commercial terms; plus a risk heatmap for single‑source and concentrated supply exposures.

Technology readiness and adoption playbooks — from traditional halobutyl blends to ultra‑conductive compounds and RFID/sensor integration, with criteria to evaluate co‑development vs. licensing strategies.

Go‑to‑market and procurement playbooks — buying strategies for OEMs and tier suppliers, including negotiation levers, specification bundles, performance guarantees and warranty structures tied to cure metrics.

M&A and partnership screening tool — high‑level valuation drivers, typical multiple ranges, earn‑out structures reflecting technology transfer, and checklists for operational integration.

Operational templates — sample RFQs, supplier scorecards, trial protocols for new bladder compounds and a turnkey approach to piloting RFID-enabled cures at scale.

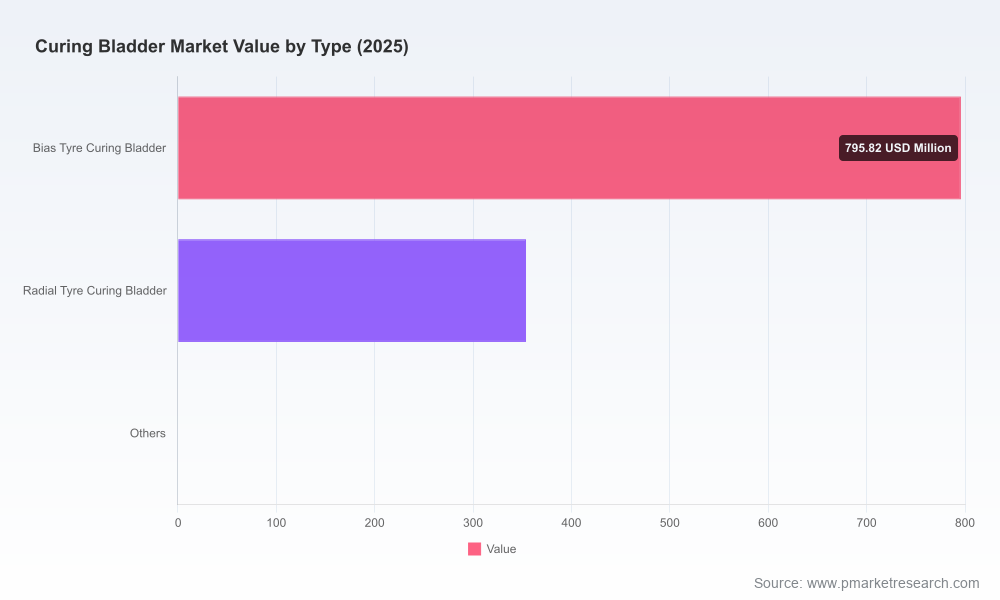

We intentionally withhold granular segment tables and proprietary splits in this executive preview — the full report contains detailed regional and application-level matrices and downloadable modelling assets that clients rely on to operationalize these findings.

Prioritize cure‑time economics over unit price. A small percentage reduction in cycle time typically delivers a multiple of procurement savings when multiplied across production volumes. Tender and contract language should include measured cure‑time KPIs and joint validation protocols.

Invest selectively in material partnerships. Co‑development agreements or preferred‑supplier clauses with vendors that control advanced elastomer technology can shorten time‑to‑market for higher‑throughput tyres and protect margin against commoditization.

Modularize capacity expansion. Given the capital intensity of mixing and press assets, consider staged capacity additions and hybrid sourcing (localize critical volumes; offshore commodity volumes) to balance cost and supply resilience.

Embed digital traceability requirements in procurement. RFID and sensorized bladder systems are now proven at scale for many production lines — requiring such features will improve quality control, yield analytics and spare‑parts planning.

Monitor raw‑material and regulatory drivers closely. Elastomer feedstock pricing and any material‑specific regulations materially affect total cost and technical feasibility of new formulations. Scenario planning for raw‑material stress cases should be part of 2026 capital approvals.

Evaluate M&A for vertical or regional access. Strategic acquisitions of specialised bladder manufacturers can provide quick access to validated formulations or regional footprints; build earn‑outs keyed to performance improvements, not just revenue targets.

Boards and strategy teams — quantify long‑term capital allocation trade‑offs and set performance KPIs for operations and procurement aligned to cure economics rather than unit price.

Procurement and supply‑chain leaders — restructure sourcing strategies toward performance‑based contracts, supplier scorecards and dual‑sourcing where needed.

R&D and plant engineering — prioritize trials on thermal‑conductive compounds and pilot sensorized bladders; use our trial protocols and test case templates to accelerate learning.

M&A teams — apply our screening tool and valuation framework to identify targets that deliver either technology uplift or immediate regional market access.

The curing bladder market in 2026 is not a passive commodity market; it is an operational lever for tire‑making productivity, quality and data‑driven process improvement. Our forecast — grounded on historical dynamics and forward scenarios — shows steady growth underpinned by materials innovation and digital enablement. For executives, the practical question is which strategic posture to adopt: invest in product partnership and local capacity, or lock in differentiated supply contracts that transfer performance risk to suppliers.

PW Consulting’s full Curing Bladder Market report provides the detailed segment tables, supplier scorecards, modelling files and step‑by‑step implementation templates that will enable you to convert the insights above into investable actions. To review the complete intelligence package, including downloadable models and supplier‑level commercial benchmarks, please visit our full study on the PW Consulting portal.

For detailed analysis of this topic, please visit the official page:Curing Bladder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com