TFT‑LCD Photomask Market — Strategic Preview for 2026 Decision‑Makers

As companies prepare capital allocation, supplier contracts and go‑to‑market moves for 2026, a clear, actionable view of the TFT‑LCD photomask market is essential. PW Consulting’s latest study (base year 2025) synthesizes five years of historical dynamics (2020–2025) with a robust forecast through 2032 to help executives translate market reality into defensible strategy. This preview surfaces the structural signals decision‑makers must act on immediately while preserving the granular segment tables and interactive models for the full report.

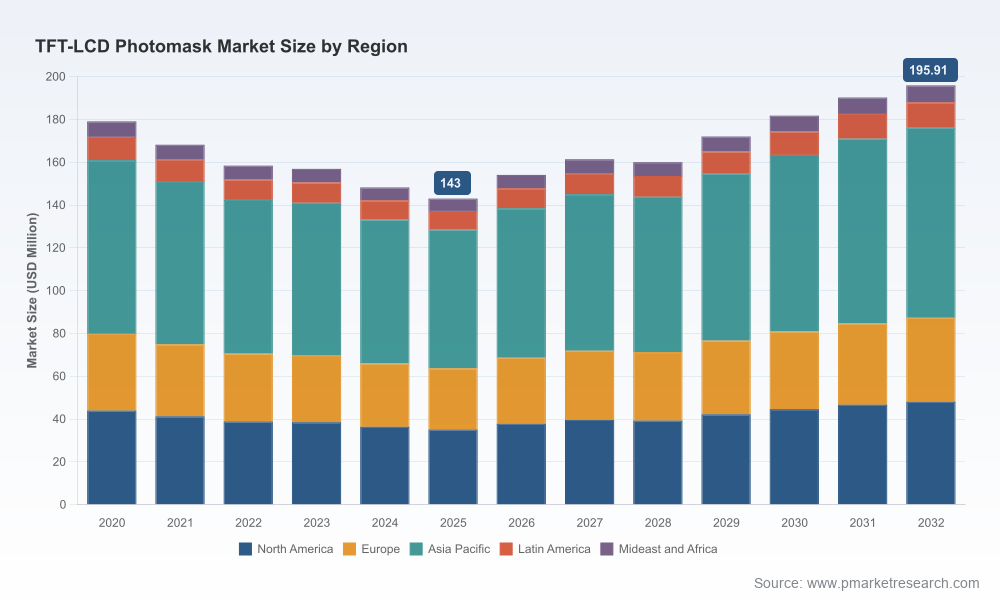

TFT-LCD Photomask Market

Why this study matters for 2026 choices

The photomask market experienced a multi‑year contraction from 2020 through the 2025 base year — a cyclical retrenchment that reset capacity rationales and supplier bargaining power. PW Consulting’s topline sizing shows the market declining in the early part of the decade and beginning to recover in 2026, with a compounded annual growth rate (CAGR) of 4.6% through the 2026–2032 forecast window (currency: USD; revenue unit: Million). By the end of the forecast period the market is materially larger than the 2025 trough, reflecting steady demand recovery, technology transitions and incremental unit value per mask driven by higher precision requirements.

TFT-LCD Photomask Market

For 2026, the strategic stakes are straightforward: firms taking conservative positions on capacity and supplier commitments risk being under‑supplied when demand normalizes; conversely, premature over‑investment can lock capital into assets that underperform if display demand diverges. Our research converts these high‑level trade‑offs into actionable scenarios and decision triggers that procurement, corporate development and manufacturing leaders can operationalize.

TFT-LCD Photomask Market

What the research delivers (practical content summary)

- Market sizing and trend decomposition — historical performance (2020–2025) and base‑case, upside and downside scenarios for 2026–2032 driven by panel demand elasticity, generational shifts, and price dynamics.

- Supply‑chain risk map — tiered supplier lists, critical raw‑material dependencies (high‑purity quartz, chrome coatings, specialty photoresists), single‑sourced inputs and mitigation playbooks.

- Technology and generation roadmap — comparative analysis of mask generations relevant to large‑format TFT and AMOLED backplanes, precision requirements, and the cost/benefit calculus for quartz versus alternate substrates.

- Cost and margin models — bottom‑up manufacturing cost models, sensitivity to raw‑material price volatility and environmental compliance costs, plus benchmarking of CAPEX and OPEX intensity for typical mask fabs.

- Vendor benchmarking and competitive positioning — multi‑dimensional scorecards covering process capability, generation footprint, geographic exposure, quality certifications and strategic customers.

- Regulatory and compliance playbook — checklist for environmental controls, hazardous waste protocols, and export‑control compliance steps that materially affect cross‑border supplier relationships.

- Strategic options and investment cases — scenarioized ROI for capacity expansions, insourcing versus long‑term contracting, joint ventures and targeted M&A.

Market structure and concentration — what to watch

The market exhibits moderate concentration, with a limited number of specialist providers commanding significant roles in high‑precision, high‑generation photomask supply. Concentration metrics indicate that top players hold a meaningful share of the market, enough to influence pricing and capacity allocation during upcycles while leaving room for nimble challengers to capture niche growth. This structure creates both opportunity and risk: incumbents can enforce lead times and premium pricing for advanced masks, yet regional champions and well‑capitalized entrants can scale quickly where policy, cost or logistical advantages exist.

Competitive dynamics — profiles and strategic activity

Our competitive review focuses on companies with proven production competencies across large‑format and high‑generation masks. Public and private players each bring differentiated strengths:

- Established Japanese and Korean firms maintain leadership in process maturity, quality controls and long‑standing partnerships with panel makers—critical where reliability and tight tolerances are non‑negotiable.

- U.S. and Taiwan players combine advanced patterning technologies with cross‑border manufacturing footprints that support both TFT‑LCD and emerging AMOLED backplane demand.

- Chinese firms have accelerated investments in high‑generation, high‑precision capacity, gaining recognition for localized supply resilience and competitive cost structures.

Recent industry signals reinforce these themes. Notable 2026 developments include facility upgrades and equipment installation by major mask makers to support advanced generation backplanes, alongside recognitions and provincial‑level awards for companies that scaled high‑generation production domestically. These events are tangible proof that technology parity and capacity expansion are core battlegrounds in 2026.

Regulation, raw materials and operational constraints

Three systemic constraints shape near‑term strategy:

- Raw‑material concentration: High‑purity quartz substrates and chrome‑based coatings are sourced from a limited supplier universe. This creates single‑point‑failure risk for mask fabs and elevates the value of supplier diversification, strategic stockpiling and backward integration analyses.

- Environmental compliance: Stringent regulations around etching, cleaning chemistries and hazardous waste disposal impose recurring compliance costs and capital requirements for treatment systems. Companies that internalize these costs late can see margin erosion and project delays.

- Export controls and technology transfer: Semiconductor‑linked equipment and IP controls complicate cross‑border capacity planning and supplier selection. Firms must assess compliance exposure when choosing partners or relocating capacity.

These constraints are not abstract; they materially influence procurement strategy, site selection, and the speed at which new capacity can be brought online.

Strategic implications for 2026 — concrete recommendations

Below are priority moves PW Consulting is advising clients to evaluate now. Each item is tied to clear decision points in our full models and scenario dashboards.

- Adapt capacity commitments to scenario triggers: favor phased capacity ramps tied to lead indicators (panel fab announcements, equipment procurement signals) rather than large one‑off expansions.

- Hedge critical inputs: implement multi‑tier sourcing for quartz and photoresists, negotiate index‑linked contracts where feasible, and model strategic inventory buffers in stress scenarios.

- Invest in compliance as a competitive moat: early investments in effluent treatment and chemical substitution can shorten time‑to‑supply for customers with strict environmental standards.

- Pursue selective vertical integration or JV structures: where single‑source raw materials or export controls create bottlenecks, partnerships that secure upstream inputs reduce delivery risk and protect margin.

- Prioritize technology parity for target customers: for players serving AMOLED backplane or large‑size TFT fabs, readiness for higher‑generation mask writing (e.g., G8.6 and beyond) is increasingly a table‑stakes capability.

- Use supplier scorecards to negotiate lead times and price protection: leverage benchmarking data to create tiered sourcing strategies that balance cost and resilience.

How to use this preview — and where to find the rest

This preview surfaces the strategic contours PW Consulting believes will most determine 2026 outcomes: a recovering topline driven by technology transitions, constrained raw‑material supply, regulatory intensity and a moderately concentrated competitive set where both incumbents and ambitious entrants can win. The full PW Consulting TFT‑LCD Photomask Market report contains the granular intelligence that operational teams need to execute: downloadable Excel models, scenario dashboards, supplier scorecards and deal‑level investment cases that we have intentionally withheld from this public summary in order to preserve client value and confidentiality.

If your 2026 capital, procurement or M&A decisions depend on a defensible view of mask generation timing, supplier risk or regulatory exposure, PW Consulting’s full dataset and advisory toolkit provide the evidence base to accelerate with confidence. Our work is geared to convert the 4.6% CAGR expectation and the post‑2025 recovery pathway into specific, measurable actions that limit downside and capture upside as the market normalizes.

Next steps

- Request the full report and interactive models to access the detailed segmentation tables, regional and application breakdowns, and vendor scorecards that underpin our recommendations.

- Book a strategy session with PW Consulting’s display and semiconductor practice to map the scenarios to your balance sheet and procurement calendar for 2026.

- Engage our due‑diligence team if you are evaluating acquisitions, JV partners, or greenfield mask‑making capacity — we combine technical, regulatory and commercial assessments into a single investment case.

PW Consulting’s TFT‑LCD Photomask Market intelligence is designed to be the operational input that converts market forecasts (base year 2025, historical 2020–2025, forecast 2026–2032) into executable 2026 strategies. For executives who need both depth and discretion, our full report supplies the empirical foundation and tactical playbook to act decisively as the market turns.

For detailed analysis of this topic, please visit the official page:TFT-LCD Photomask Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com