Effective Skin Correction Through Mole Removal in Dubai | Clear & Safe Skin Solutions

Health |

2026-06-09 08:53:16

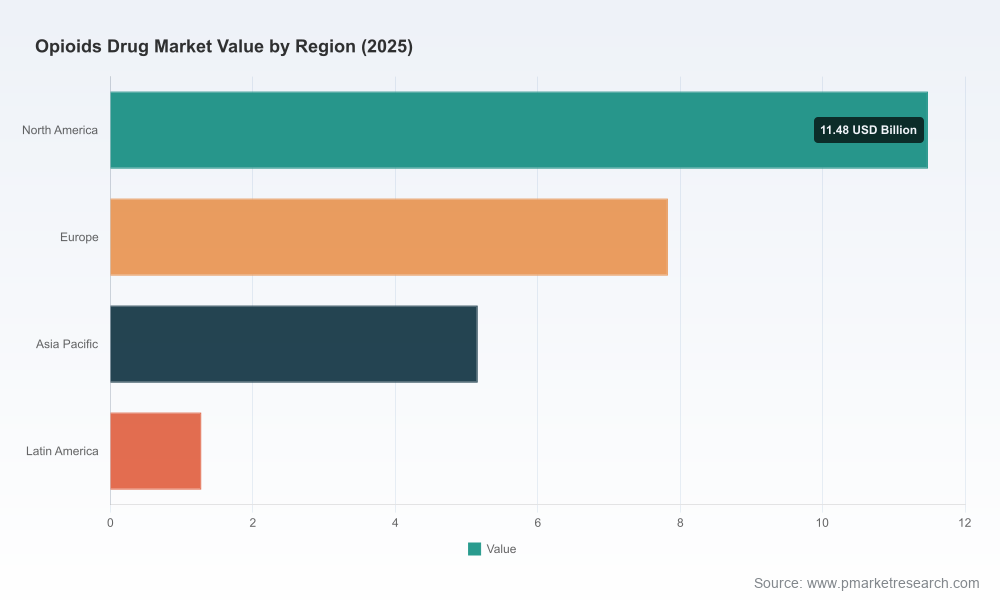

As companies finalize budgets and strategic roadmaps for 2026, the opioids drug market presents a paradox: secular demand for effective analgesia and opioid use disorder (OUD) therapies sits alongside intensifying regulatory scrutiny, pricing pressure, and rapid product- and delivery-system innovation. PW Consulting’s latest market research — based on a 2025 base year and a 2026–2032 forecast horizon — quantifies that this market has expanded from the low‑20 billion USD range in 2020 to roughly USD 25.75 Billion in 2025 and is projected to reach approximately USD 35.02 Billion by 2032, reflecting a compounded annual growth rate of about 4.54% through the forecast period. These headline metrics confirm steady, investible market growth — but they conceal the tactical complexity that will determine winners and losers in 2026.

Opioids Drug Market

Actionable timing. Our analysis converts multi‑year projections into tactical decision windows — when to launch, when to accelerate supply, and when to pause on scale investments pending regulatory clarity.

Opioids Drug Market

Risk-calibrated portfolio guidance. The research links clinical, regulatory, and reimbursement vectors to product‑level revenue volatility so portfolio managers can prioritize programs by risk‑adjusted return.

Opioids Drug Market

Competitive posture playbooks. For market incumbents and challengers alike, we translate market structure signals into go‑to‑market prescriptions: defend via scale and cost leadership, or differentiate via delivery systems and abuse‑deterrent formulations.

Deal and M&A intelligence. We identify where consolidation is most likely to create value — and where price competition will erode synergies — helping M&A teams size targets and model post‑close scenarios.

Proprietary, auditable market-sizing model (2020–2032) with scenario toggles for regulatory tightening, abuse‑deterrent adoption, and OUD-treatment expansion.

Demand-driver framework mapping demographics, surgical volumes, chronic pain prevalence, and OUD treatment uptake to market outlooks.

Regulatory watchlist and event calendar — FDA guidance, REMS revisions, and major litigation outcomes — with likelihood-impact scoring to quantify near‑term shocks.

Pricing and margin-pressure matrix that combines generic dynamics, tendering behavior, and reimbursement shifts across channels.

Go‑to‑market playbooks tailored to business models: large generics, specialty formulators, device‑enabled drug delivery firms, and OUD therapy specialists.

Supply‑chain heatmaps highlighting critical raw-material concentration, API sourcing risk, and capacity bottlenecks that affect launch timelines.

Company benchmark profiles and strategic scorecards: capabilities, route-to-market, pipeline, manufacturing footprint, and regulatory track record.

Investor‑grade pitch decks and executive one‑pagers that synthesize our findings into decision-ready messaging for Boards and investors.

The opioids market exhibits a mixed structure: concentration is meaningful at the top — our analysis estimates that the three largest players control a substantial portion of the market while the top five increase that share further — creating a landscape where scale confers clear advantages in procurement, distribution reach, and regulatory resources. Yet a long tail of specialists and regional players sustains competitive intensity in specific formulations and channels.

Key competitive archetypes and their strategic implications:

Large generics manufacturers (e.g., Teva, Viatris, Sun Pharma, Amneal, Apotex, Alvogen): Compete on scale, cost-efficiency, and broad channel coverage. Their assets — established manufacturing lines and distribution networks — make them default suppliers to hospitals and retail chains. Strategic emphasis for these firms should be optimizing margin through manufacturing footprint rationalization, tender-management capabilities, and proactive regulatory compliance programs to avoid costly plant shutdowns or import restrictions.

Specialty formulators and delivery‑system innovators (e.g., Collegium Pharmaceutical, OsmoTech, Kindeva): Differentiate via extended‑release technologies, abuse‑deterrent formulations, and alternate routes such as nasal sprays and implants. These firms can command premium pricing and defend niches, but they must sustain R&D and regulatory relationships to convert technological differentiation into commercial returns.

OUD and adjunct-treatment specialists (e.g., Indivior): Operate at the intersection of public‑health policy and commercial opportunity. Demand for OUD treatments can be countercyclical to tighter opioid prescribing, creating natural hedges for portfolios that combine analgesics with OUD therapeutics.

Mid‑sized and regional players (e.g., Zydus, Lannett, ANI, Par, Tris, Ascent): Often nimble in launching approved generics, they face margin pressure but can exploit regional supply dislocations and niche formulations. Strategic focus should be partnerships for complex generics and targeted capacity expansion where price competition is less intense.

Branded and strategic big‑pharma participants (e.g., Janssen, Allergan, Hikma): Continue to shape innovation and REMS ecosystems. Their participation underpins markets for specialty products and abuse‑deterrent innovations that alter competitive dynamics.

We provide three practical scenarios that executives should model into their 2026 plans. Each is accompanied by concrete moves that are executable within a 12–24 month window.

Scenario A — Baseline moderate growth (aligned with the 4.54% CAGR): Prioritize operational efficiency and targeted portfolio pruning. Tactical plays: accelerate scale‑up for high-volume oral generics, renegotiate supply contracts to lock raw material costs, and fast‑track a limited set of abuse‑deterrent reformulations that can be commercialized with reasonable regulatory risk.

Scenario B — Regulatory tightening and stewardship acceleration: Shift investments toward non‑prescription adjuncts and OUD therapies; divest commoditized lines where margins compress. Tactical plays: redeploy capital into specialty delivery platforms, secure diversified API sources, and expand collaborations with payors for bundled pain‑management solutions.

Scenario C — Innovation-adoption surge (extended‑release & abuse‑deterrent premium): Lean into product differentiation and commercialization muscle. Tactical plays: prioritize launches of complex generics and device‑enabled products, invest in REMS infrastructure to smooth market access, and pursue bolt‑on acquisitions to fill delivery‑system gaps.

C‑suite and corporate strategy: Use the scenario models to stress‑test capital allocation and M&A pipelines against regulatory shock scenarios and pricing compression.

Business unit leaders: Apply the go‑to‑market playbooks and channel maps to refine launch sequencing and commercial resourcing.

Supply‑chain and operations: Leverage the supplier concentration and capacity heatmaps to build redundancy where failure modes are high impact.

BD and M&A teams: Use the competitor scorecards and playbook to prioritize targets that deliver technological differentiation or fill strategic supply vulnerabilities.

PW Consulting’s brief demonstrates that the opioids market is neither a simple commodity arena nor a protected specialty market; it is a hybrid industry in which scale and regulatory competence coexist with premium pockets for innovation. The headline growth trajectory — moving from around USD 25.75 Billion in 2025 toward roughly USD 35.02 Billion by 2032 at a mid‑single‑digit CAGR — creates optionality, but the value capture will be determined by precise, time‑sensitive moves: where to invest, where to defend, and where to withdraw.

For executives preparing 2026 plans, our report is a decision engine: it pairs auditable models with playbooks and competitor intelligence so leaders can translate market signals into concrete actions. To access the full segmented projections, granular company scorecards, and downloadable scenario models that underpin these recommendations, please consult the PW Consulting market portal where the complete dataset and implementation templates are available.

For detailed analysis of this topic, please visit the official page:Opioids Drug Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com