Miniature Atomic Clock Market: Strategic Outlook for 2026 Decision-Making

PW Consulting’s Miniature Atomic Clock Market primer frames why 2026 is a strategic inflection year for companies engaged in precision timing. Using 2025 as the base year and projecting through 2032, our modelling shows the addressable market expanding at a compound annual growth rate (CAGR) of 9.87% (USD, revenue unit: Million). Historical momentum is clear: the market rose from roughly USD 141 million in 2020 to about USD 208 million in 2025 and is projected to approach USD 396 million by 2032. This trajectory reflects a convergence of technology maturation, new operational use cases (LEO constellations, resilient terrestrial networks, autonomous systems), and an accelerating migration from laboratory-grade timing to embedded, SWaP-optimized timing modules.

Miniature Atomic Clock Market

Why this study matters for 2026 corporate decisions

- Timing is a strategic input. High-precision timing is now a cross-domain enabler — influencing telecom synchronization, GNSS resilience, defense systems, and distributed sensing. Executive decisions in product roadmaps, procurement, and partnerships must internalize timing as a system-level capability, not a component afterthought.

- Mid-decade acceleration. With a near-10% CAGR baked into our base-case forecast, companies that secure design wins and supply resilience in 2026 position themselves to capture disproportionate share of growth through 2032.

- Market structure favors focused plays. Market concentration is low: the top-three and top-five suppliers together account for only a quarter-ish of total sales, indicating a fragmented landscape and multiple commercially viable niches for innovators, integrators, and specialist suppliers.

- Supply-side constraints present both risk and opportunity. Key components — notably miniature lasers and certain exotic packaging elements — remain cost and capacity drivers. Firms that invest in upstream supply assurance or alternate technologies can create durable competitive advantage.

Teaser of core findings (high-level)

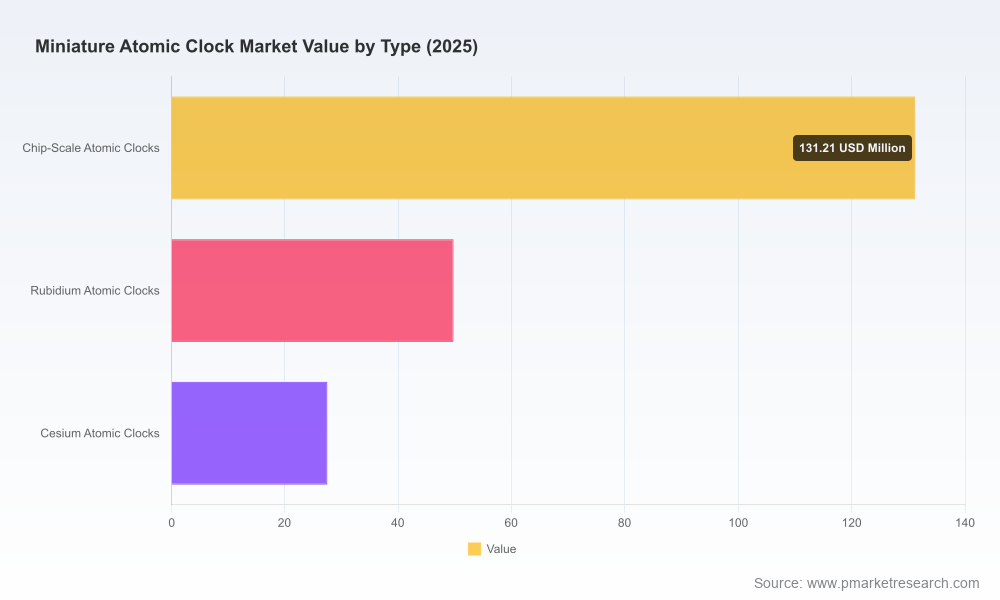

- Technology bifurcation: Chip-scale atomic clocks (CSACs) are enabling ultra-low-power, highly embedded timing, while miniature rubidium variants continue to lead where holdover stability is critical. Each technology path supports different system architectures and procurement strategies.

- Applications set the cadence. The fastest adoption vectors combine persistent timing value and scale potential — e.g., telecom holdover, distributed sensing for infrastructure, and GNSS-resistant navigation for defense and unmanned systems.

- Manufacturing is moving from prototype to volume in pockets. Recent commercial scale-ups and targeted product launches demonstrate that cost curves are improving, but economies of scale remain uneven globally.

- Standards and credentials matter. Professional programs and standardization activities (2025–2026) are raising the bar on deployment readiness and cross-industry interoperability, shortening sales cycles for compliant vendors.

Competitive landscape — what leading players are signalling

- Microchip Technology Inc. (Chandler, AZ) — With a portfolio of embedded rubidium-based clocks and the recent second-generation Low-Noise CSAC (SA65-LN), Microchip is pursuing a platform strategy that blends lower power draw with broader temperature range and integration friendliness. Strategic implications: incumbents and systems integrators should expect shorter qualification times for Microchip products but also increased pricing pressure in the embedded market; partnerships on co-developed modules will be valuable.

- Safran Electronics & Defense (Paris) — Safran’s focus on low-SWaP rubidium clocks (e.g., MIRA) targets defense and telecom holdover segments with tight performance specs. Strategic implications: prime contractors and national programs will treat Safran as a design-win target for high-assurance applications; suppliers should model long procurement cycles but high margins.

- AccuBeat Ltd. (Israel) — Specialist in ruggedized rubidium standards focused on anti-spoofing and space-grade timing. Strategic implications: opportunities for co-development with cyber-resilience teams and defense primes; good fit for niche, high-value programs.

- Chengdu Spaceon & Taitien (China) — Suppliers pushing CSAC and rubidium variants into satellite navigation and embedded applications, with recent scale-up activity in chip-scale production. Strategic implications: global OEMs must assess dual-sourcing strategies and local qualification timelines, while component suppliers may unlock volume wins by supporting these producers.

- T4Science & Oscilloquartz (Europe) — Focused on space/ground-grade frequency standards and optical/rubidium mixes. Strategic implications: these vendors are attractive partners for aerospace primes and telecom carriers seeking upgrade paths beyond legacy oscillators.

Notable near-term developments include Microchip’s January 2025 launch of an LN-CSAC with reduced profile and improved power consumption, Safran’s October 2025 MIRA product setting new holdover benchmarks, and a 2026 commercial-scale production milestone by a Chinese CSAC manufacturer. Collectively these moves indicate a shift from early-adopter projects to productized, scalable offerings.

Miniature Atomic Clock Market

What the full report contains — practical, operational deliverables

- Transparent market-sizing methodology and a 2020–2032 revenue model (base year 2025), with scenario-adjustable levers for component cost, adoption rate, and policy interventions.

- Action-oriented use-case mapping and buyer personas: telecom operators, defense primes, satellite integrators, drone/swarm architects, and scientific platforms.

- Competitive supplier profiles with capability matrices, recent contract activity, and product lineage (technical trade-offs, SWaP, holdover characteristics).

- Go-to-market playbook: OEM sourcing decisions, system integration pathways, design-win accelerators, and a procurement checklist for qualification and sustainment.

- Supply-chain risk & mitigation framework: critical-component heat maps (lasers, vacuum packaging), alternate sourcing strategies, and inventory tactics for 2026 shocks.

- M&A and partnership heatmap highlighting targets for vertical integration (laser suppliers, packaging specialists) and horizontal expansion (embedded timing modules).

- Regulatory and standards watch with recommended engagement plans for 2026 industry bodies and credential programs.

Note: This public-facing summary intentionally omits detailed regional and application-level revenue tables and company-level revenue splits (these are included in the full PW Consulting report). The omission is deliberate: the granular segmentation is central to operational decisions and is available through our full dataset and interactive dashboards.

Miniature Atomic Clock Market

Strategic recommendations for executives in 2026

- Incumbent vendors — Prioritize product lines that trade power and form-factor improvements for broader market penetration. Shorten time-to-market by qualifying components with dual suppliers and locking in long-lead items (miniature lasers, vacuum packages).

- New entrants & startups — Focus on narrow, high-value use cases (anti-spoofing, LEO inter-satellite sync, telecom holdover) where the fragmented market lowers barriers to entry. Seek co-development agreements with systems integrators rather than competing on end-to-end platforms.

- Component suppliers — Laser and packaging firms should accelerate capacity and consider licensing / JV opportunities with clock OEMs to secure volume and capture upstream margins.

- Systems integrators & defense primes — Incorporate timing requirements into early design phases and allocate budget for redundancy (hybrid timing architectures). Insist on interoperability testing and supplier roadmaps that cover 10+ year sustainment.

- Telcos & critical-infrastructure operators — Initiate pilot deployments to validate holdover strategies and quantify TCO improvements from embedded atomic timing versus classical GPS-dependent designs.

Scenario planning — triggers and contingency playbooks

- Base case (our core forecast) — Continued steady adoption across telecom and defense; cost reductions from targeted scale-ups; market grows at ~9.9% CAGR through 2032. Recommended posture: accelerate qualification and establish multi-sourcing.

- Upside (accelerated adoption) — Rapid LEO deployments, regulatory mandates for GNSS resilience, or breakthrough cost reductions for lasers could compress time-to-adoption and expand addressable market materially. Recommended posture: aggressive market share capture, deepen partnerships, and accelerate manufacturing scale.

- Downside (supply constraints/geopolitics) — Component bottlenecks or export controls impede global sourcing, delaying designs and increasing costs. Recommended posture: localize critical supply, pursue strategic stockpiles, and accelerate licensing to alternative tech routes.

Conclusion — the 2026 strategic window

2026 represents a pivotal year for companies who want to translate timing technology advances into durable business advantage. The market’s near-10% CAGR and the projected doubling of revenue over the 2025–2032 horizon create a multi-year window to establish design wins, secure supply chains, and define standards. Yet the landscape is fragmented and component constraints mean first-mover advantage is conditional: it depends on execution across engineering, procurement, and commercial channels.

PW Consulting’s full Miniature Atomic Clock Market report delivers the granular segmentation tables, supplier revenue splits, and interactive scenario models that corporate strategists and product leaders need to convert this market potential into profit. For a data-driven playbook and the complete set of operational tools, access the full report via our client portal.

For detailed analysis of this topic, please visit the official page:Miniature Atomic Clock Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com