O-Cresol (CAS 95-48-7) Market: Strategic Outlook for 2026 — PW Consulting Industry Brief

As PW Consulting’s senior industry analyst, I present an evidence-based preview of our comprehensive O‑Cresol market study — designed to inform boardroom decisions and commercial strategy for 2026. This brief synthesizes the report’s central implications while intentionally withholding granular sub‑segment tables and plant‑level intelligence to invite direct access to the full study. The aim: demonstrate methodological rigor and decision readiness, while preserving the premium insights that convert analysis into competitive advantage.

O-Cresol (CAS 95-48-7) Market

Executive snapshot: why O‑Cresol matters in 2026

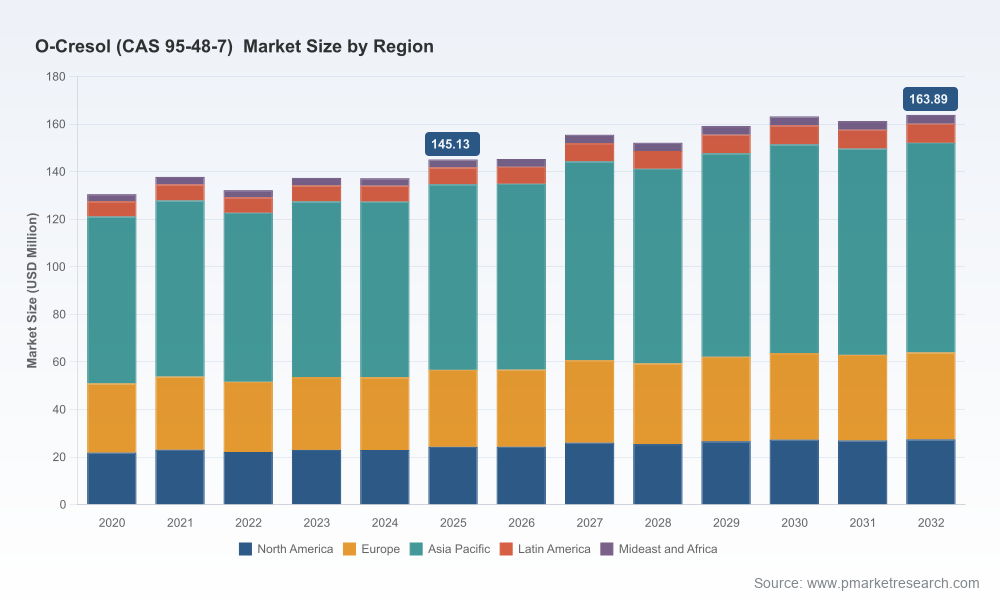

O‑Cresol remains a niche but strategically important intermediate across resins, crop protection chemistries and disinfectants. After a period of modest volatility through 2020–2025, the global market reached approximately USD 145.13 Million in our 2025 base year and is modeled to expand through the 2026–2032 forecast window at a conservative compound annual growth rate (CAGR) of 1.8%. The forecast path shows muted growth with episodic rebounds — a pattern that favors disciplined operators who can optimize cost structures, secure feedstock continuity and selectively pursue value‑chain integration.

O-Cresol (CAS 95-48-7) Market

What this means for 2026 decision making

- Prioritize feedstock governance. Phenol price movement is the single most consequential near‑term cost driver: our sector monitoring flagged rising phenol prices in May 2026 across key regions (Northeast Asia ~USD 1.31/kg; Europe ~USD 1.30/kg; Middle East ~USD 1.12/kg), with month‑over‑month upticks that create short windows for margin recovery or inventory risk. Procurement and hedging strategies must be reassessed now, not later.

- Differentiate around reliability and specialty application support. With modest market growth, suppliers that can deliver technical service (formulation support, regulatory documentation, traceability) will command funding and longer customer tenure.

- Read consolidation opportunistically. The market displays moderate concentration at the top: the three‑firm and five‑firm concentration ratios indicate room for scale benefits without outright domination. Financial sponsors and strategic buyers can target bolt‑ons that unlock downstream access or regional supply security.

- Embed regulatory foresight into commercial planning. Restrictions on certain cresol‑derived pesticides remain active in major jurisdictions (for example, Canada’s export controls continue to constrain specific dinitro‑ortho‑cresol salts). Companies must fold regulatory scenarios into 12–24 month demand forecasting.

Market trajectory and practical interpretation

The 2020–2025 historical window showed oscillations driven by feedstock cycles, demand swings in end‑use industries and episodic capacity shifts. Our base year, 2025, consolidates those effects into a stabilizing market around USD 145 Million. The 2026–2032 forecast — centered on a 1.8% CAGR — signals a market that is unlikely to deliver dramatic topline expansion, but that rewards operational discipline, targeted product premiumization and selective geographic plays.

O-Cresol (CAS 95-48-7) Market

For commercial leaders, this implies shifting emphasis from volume growth to margin expansion: optimize plant utilization, pursue higher‑value grades, and deploy targeted marketing in resilient end‑use segments. For procurement and supply‑chain heads, the immediate priority is converting short‑term phenol price volatility into predictable procurement outcomes via blended sourcing, contract flexibility and, where appropriate, captive upstream integration.

Competitive landscape — profile of market participants

The O‑Cresol supplier set blends vertically integrated chemicals groups, regional specialty producers and merchant traders. Key participants we profile in the full study include established captives and majors such as Atul Ltd. (India), Deepak Novochem Technologies Ltd. (India), LANXESS AG (Germany), SABIC (Saudi Arabia), Everchem Inc. (United States) and Sasol Limited (South Africa), alongside regional manufacturers across Asia and Japan (e.g., Nantong Xingchen, JFE Chemical, Nippon Steel & Sumikin Chemical) and several Chinese producers. These players exhibit different strategic postures:

- Captive producers with downstream resin or agrochemical integration benefit from internal demand smoothing and margin capture, but face capital allocation tradeoffs between upgrading existing assets and expanding capacity.

- Large diversified chemical groups leverage global commercial networks and risk management to stabilize margins but encounter complexity in prioritizing smaller intermediates within broader portfolios.

- Regional specialists and merchants compete on responsiveness and logistics, often winning business where speed, local regulatory support and flexible packaging matter most.

Our competitive benchmarking in the full report evaluates plant footprints, technology pathways (extraction vs synthesis routes), service models and channel strategies — and it translates that benchmarking into concrete scenarios for market entry, capacity rationalization, and price leadership. Note that the summary above purposely omits the granular segment shares and plant‑level metrics available only in the full subscription product.

Dynamics shaping 2026 strategy

- Feedstock inflation and short‑cycle risk: As noted, phenol spikes in May 2026 across multiple regions created immediate cost pressure. The geographic pattern of these moves matters for tolling economics and cross‑border arbitrage. Tactical responses include time‑phased contracts, strategic inventory buffers and selectively passing through costs in long‑term supply arrangements.

- Regulatory and trade oversight: Continued restrictions on certain cresol‑derived compounds in jurisdictions such as Canada increase compliance complexity for exporters and place a premium on regulatory intelligence. Upstream and downstream players must invest in documentation controls and alternate routing for sensitive products.

- Customer consolidation and formulary shifts: End‑use buyers — manufacturers of resins, disinfectants and crop protection chemistries — are optimizing procurement to fewer, higher‑service suppliers. For suppliers, the commercial playbook is to convert technical capability into preferred‑supplier status through joint cost‑of‑ownership workstreams.

- Moderate market concentration + fragmentation opportunities: The measured CR3/CR5 ratios show leading suppliers command meaningfully but not overwhelmingly large shares. This creates simultaneous pressure (price competition) and opportunity (accretive roll‑ups, service differentiation).

Strategic playbook for 2026 — actionable priorities

- For incumbents: Accelerate margin engineering. Reassess catalytic routes, heat integration and waste reduction projects with prioritized payback thresholds to offset feedstock headwinds. Build tiered commercial offers that monetize technical support.

- For regional players: Lock in logistics and regulatory arbitrage. Localized service and faster documentation throughput can justify a premium and defend against import competition during feedstock shocks.

- For potential acquirers: Pursue precision M&A. Target assets that deliver downstream access to resilient end uses, close feedstock linkages, or provide captive demand. Avoid value traps in purely commoditized capacity without service differentiation.

- For procurement and supply chain leaders: Implement a phenol‑price playbook. Combine short‑term tactical buys with medium‑term supplier partnerships, and evaluate limited vertical integration where feedstock volatility materially affects margins.

- For R&D and product teams: Prioritize formulation work that increases O‑Cresol value capture — for instance by enabling higher‑margin resin chemistries or disinfectant formulations with proven performance claims that justify price premiums.

What the full PW Consulting report contains (high‑value deliverables)

Our full market study is structured to convert insight into executable plans. Deliverables include:

- Transparent market sizing and methodology for the 2020–2025 historical window and the 2026–2032 forecast horizon (base year 2025). The report documents assumptions, scenario alternatives and sensitivity testing around feedstock pricing and regulatory shocks.

- Supply‑side forensic: plant‑level capacity mapping, operating rates, route economics (extraction vs synthesis), and trade flow analysis.

- Customer and application intelligence: end‑use demand trends, product laddering and technical service expectations (note: detailed application splits are available only in the full study).

- Competitive benchmarking: strategic profiles for each major supplier, capability matrices and M&A heatmaps.

- Risk register and decision tree: regulatory, feedstock, logistics and demand risks with quantified upside/downside scenarios and mitigation playbooks.

- A 12‑ to 18‑month commercial playbook tailored to company archetypes (captive producer, global major, regional merchant, private equity owner).

How to use this brief to shape 2026 plans

Use this brief to prioritize internal review areas: procurement contracts, plant optimization programs, and customer retention strategies. If your organization is contemplating capital expenditure, M&A or a new commercial model in 2026, the full report supplies the critical segmentation, plant economics and competitor moves that convert hypothesis into investment grade strategy.

Closing — the strategic edge

O‑Cresol is not a high‑growth headline chemical, but it is strategically significant within several value chains where formulation performance and supply reliability command premium returns. In a low‑growth, intermittently volatile environment, disciplined operators who combine technical service, feedstock governance and targeted M&A will outpace the market. PW Consulting’s full study delivers the granular intelligence and execution templates needed to make those moves confidently in 2026.

To access the complete dataset, segmentation tables, plant‑level maps and the customised 12–18 month playbook, please contact PW Consulting. The full suite contains the proprietary insights that translate the signals described above into market‑winning action.

For detailed analysis of this topic, please visit the official page:O-Cresol (CAS 95-48-7) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com