Industrial Hydraulic Shock Absorber Market — Strategic Outlook for 2026 Decision‑Makers

As industrial systems accelerate toward higher speeds, greater payloads, and tighter cycle times, the humble hydraulic shock absorber has re-emerged as a strategic component — not merely a commodity. This industry briefing previews PW Consulting’s full Industrial Hydraulic Shock Absorber Market study (base year 2025, forecast 2026–2032) and explains the concrete ways the report will change how executives allocate capital, structure supply chains, and prioritize product development in 2026. Consider this a trailer: we demonstrate the analytical depth and decision-ready perspectives you will find in the full study while intentionally withholding granular segment tables to guide you to the full dataset.

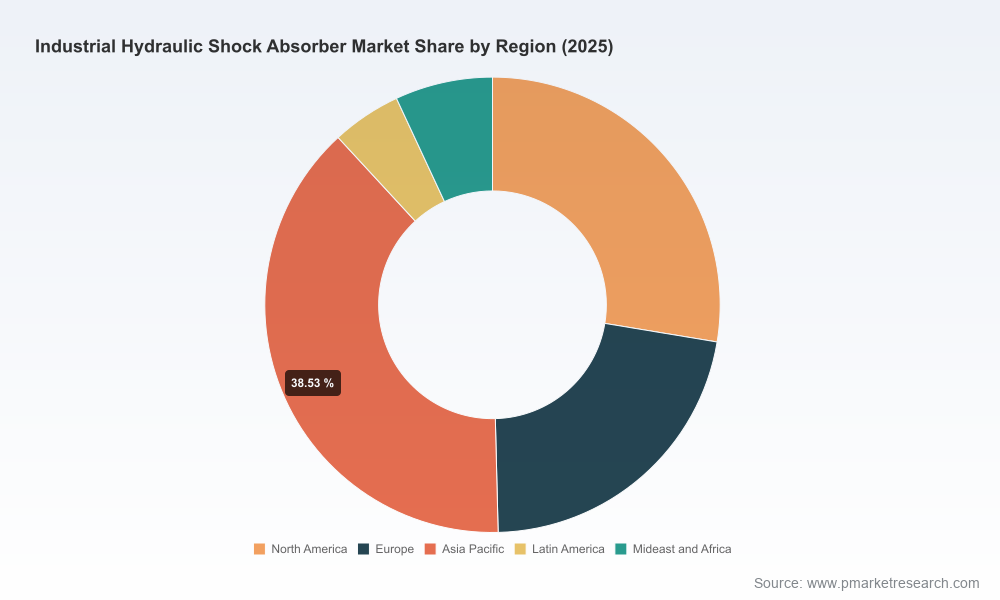

Industrial Hydraulic Shock Absorber Market

Market at a Glance — The Macro Trajectory

Between 2020 and 2025 the market exhibited steady expansion, rising from a modest base and reaching an overall market size of approximately 288 Million USD in 2025. Our forecast projects continued growth through the 2026–2032 horizon at a compound annual growth rate (CAGR) of 3.57%, with the market approaching the high three‑hundreds Million USD by 2032. That trajectory reflects a combination of steady demand from industrial automation, renewal cycles in material‑handling equipment, and incremental specification shifts toward higher-performance, adjustable damping solutions.

Industrial Hydraulic Shock Absorber Market

Why 2026 Is an Inflection Year

- Acceleration in intralogistics and automation: Warehouse automation and robotics continue to require more precise end‑of‑travel deceleration, increasing demand for engineered hydraulic absorbers that balance energy absorption with compact form factors.

- Performance differentiation: Customers increasingly value adjustable and smart damping solutions that reduce machine downtime and extend equipment life — creating higher margin opportunities.

- Cost and supply volatility: Fluctuations in steel, specialty alloys, and hydraulic fluids are pressuring manufacturing margins and forcing procurement and sourcing strategies to become more sophisticated.

- Regulatory and safety expectations: Evolving machine‑safety standards are pushing OEMs to specify certified, validated shock‑absorption solutions rather than make‑do with generalist alternatives.

Taken together, these dynamics make 2026 a strategic planning year: investment windows are opening for targeted R&D, supply‑base rationalization, and aftermarket capture strategies that can secure sustainable margin improvements over the forecast period.

Industrial Hydraulic Shock Absorber Market

What the PW Consulting Report Delivers (Practical, Executable Insights)

- Top‑level market sizing and a validated growth path (2020–2032) with scenario variants for conservative, base, and accelerated adoption curves.

- Demand drivers mapped to product attributes (e.g., adjustable vs non‑adjustable designs, bore sizes, and energy ratings), and the commercial levers that convert technical advantage into price realization.

- Supply‑chain stress testing: raw‑material exposure analysis, cost pass‑through sensitivity, and recommended hedging/dual‑sourcing playbooks to protect margins in 2026 procurement cycles.

- Regulatory impact assessment highlighting certification requirements and design implications for safety-critical applications across major markets.

- Commercial strategy modules — channel segmentation, pricing architecture, aftermarket service propositions, and field retrofit opportunities that prioritize near‑term cash conversion.

- Competitive benchmarking and company capability maps that identify where scale, engineering depth, and channel reach translate into defendable positions.

- Deal origination and valuation frameworks for M&A and partnership activity, including identified archetypes of attractive targets and integration playbooks.

Note: to preserve the “trailer” intent of this overview, we summarize methodological and actionable outputs here but reserve the detailed segment breakouts, regional and application tables, and downloadable financial models for the full report package.

Competitive Landscape — Who Matters and Why

The market is characterized by a meaningful presence of specialist engineering suppliers and product innovators rather than deep consolidation. Our concentration metrics point to a fragmented field in which several well‑established niche players exert outsized influence through technical differentiation and industry relationships (CR3 ≈ 24.6%, CR5 ≈ 26.2%). For 2026 strategy, three types of competitors matter:

- Engineering specialists with heavy‑duty and adjustable portfolios: Firms that supply large‑bore, high‑energy absorption units for heavy machinery and safety applications hold technical credibility and are increasingly sought by OEMs seeking performance over price.

- Automation‑focused producers: Manufacturers offering compact, high‑cycle miniature shock absorbers targeted at factory automation and robotics are competing on integration, servicing, and predictable life‑cycle performance.

- System suppliers for intralogistics: Companies producing end‑stop buffers and buffers tailored for conveyors and stacker cranes are benefiting from warehouse automation investments; product launches in this sub‑segment are creating fast windows for incumbency.

Representative companies to watch (selected profiles are elaborated in the full report):

- Enidine (Orchard Park, NY) — strong credentials in adjustable and large‑bore units, positioning on energy absorption and safety applications.

- ACE Controls Inc. (Ann Arbor, MI) — known for MAGNUM and miniature series with high energy ratings suited to demanding automation controls.

- Taylor Devices, Inc. (North Tonawanda, NY) — focus on self‑adjusting heavy‑duty shock absorbers catering to variable impact conditions in heavy equipment.

- Leben‑Dämpfungstechnik GmbH (Berg, Germany) — product launches targeted at automated warehouses and intralogistics safety elements.

- Zimmer Group (Germany) — spiral‑groove PowerStop technology and recent PowerStop 2.0 launch point toward higher energy absorption and improved adjustability.

- Weforma Dämpfungstechnik GmbH and Bansbach easylift GmbH — representing depth in heavy‑duty deceleration cylinders and precise damping components across machinery engineering segments.

Recent product and market activity (highlights): Leben’s late‑2025 launch of hydraulic buffers for intralogistics and Zimmer’s PowerStop 2.0 introduction in early 2026 underscore how product innovation is concentrated on automation and warehouse exposures. Enidine’s participation at Eurosatory 2026 signals continued emphasis on demonstrating performance and safety credentials to specifiers.

Industry Tailwinds and Risks — What to Build Into 2026 Plans

- Tailwinds: steady adoption in factory automation and intralogistics; retrofit opportunities as operators pursue uptime and equipment life extension; premiumization toward adjustable designs.

- Risks: raw‑material volatility (steel, specialty alloys, hydraulic fluids) that compresses margins unless mitigated; pricing pressure from lower‑cost entrants; and regulatory changes that can both increase specification complexity and raise barriers to entry.

These forces mean companies must balance short‑term margin protection with medium‑term investments in product differentiation and certification. The right mix varies by corporate ambition — growth through market share, margin optimization, or acquisition-led scale.

Concrete Strategic Actions for 2026

- Protect margins now: implement procurement hedges and dual‑sourcing for raw materials, and deploy dynamic pricing frameworks to capture commodity cost pass‑throughs.

- Prioritize product platforms: invest in adjustable and modular absorber platforms that address multiple applications with incremental SKUs rather than bespoke heavy engineering for every customer.

- Capture aftermarket value: design serviceable interfaces, spare‑parts kits, and subscription diagnostics that convert one‑time OEM sales into recurring revenue.

- Targeted M&A: identify bolt‑on suppliers that add either channel access (e.g., intralogistics OEM relationships) or technical differentiation (e.g., spiral‑groove or self‑adjusting technology).

- Certification and safety strategy: accelerate product certification where it unlocks specification by Tier‑1 OEMs and reduces customer switching.

- Commercial model redesign: align sales incentives to higher‑margin adjustable products and retrofit programs; use pilot programs to demonstrate TCO improvements for large accounts.

Where to Place Your 2026 Bets

Decisions should be prioritized by horizon and impact. Near term (0–12 months): secure supply, optimize pricing mechanics, and pilot aftermarket services with high‑value accounts. Medium term (12–36 months): accelerate R&D on adjustable and compact high‑energy designs, pursue targeted acquisitions to fill capability gaps, and scale service delivery. Long term (beyond 36 months): broaden platform architecture to embed sensing and predictive maintenance, thereby moving from passive absorbers to components in connected motion‑control systems.

How PW Consulting Can Accelerate Your 2026 Plan

PW Consulting’s full Industrial Hydraulic Shock Absorber Market study provides the proprietary datasets, supplier maps, and valuation frameworks needed to operationalize the actions above. Our offerings include:

- Data access and interactive dashboards with downloadable market models for scenario planning.

- Bespoke workshops to convert market insight into a 90‑day execution plan and a three‑year product roadmap.

- M&A advisory and target screening using competitive benchmarking and value capture simulations.

- Procurement playbooks for raw‑material risk mitigation and supplier consolidation strategies.

For executives preparing capital allocation and product‑strategy decisions in 2026, the difference between a cautious and a confident move often comes down to segment‑level insight and validated supplier intelligence. This briefing highlights the strategic vectors and tactical plays; the full report supplies the granular segment breakouts, regional and application tables, and downloadable models that will let your team convert insight into measurable outcomes. Visit our report page to access the full dataset and license options.

For detailed analysis of this topic, please visit the official page:Industrial Hydraulic Shock Absorber Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com