North America's Advanced Manufacturing Sector Boosts Roll-to-Roll Printing Adoption

Other |

2026-06-10 10:14:31

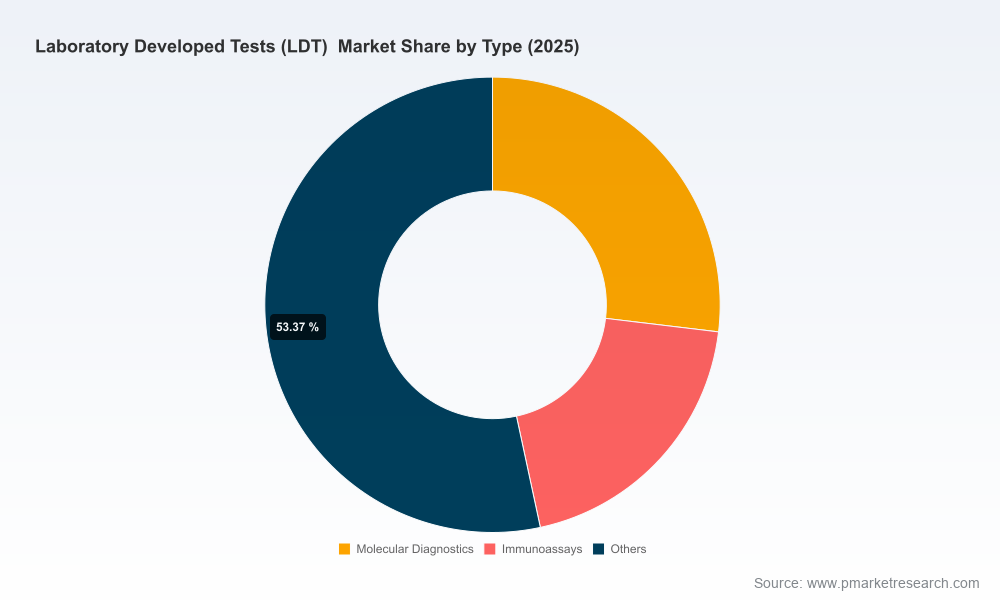

By 2025 the global Laboratory Developed Tests (LDT) market reached approximately USD 5,800 Million (base year 2025). Our modeled baseline shows the market expanding through the forecast window (2026–2032) at a compound annual growth rate (CAGR) of roughly 6.6%, reaching an estimated USD 9,086 Million by 2032. That trajectory reflects persistent clinical demand, accelerating adoption of advanced molecular and genomic methods, and a competitive structure in which a handful of large laboratory networks coexist with a long tail of specialist providers.

Laboratory Developed Tests (LDT) Market

For executive teams making capital allocation, product strategy, partnership or M&A decisions in 2026, the combination of steady market growth and elevated regulatory uncertainty creates both opportunity and risk. This study is designed to be the decision engine for that moment: it translates market size and growth into actionable scenarios, operational plans, and commercial playbooks that map directly to board-level choices across diagnostics companies, reference labs, health systems, and investors.

Laboratory Developed Tests (LDT) Market

The regulatory environment shifted materially in 2025, producing a new operating baseline for 2026. A federal court vacated the 2024 FDA rule that had reclassified many LDT activities under device regulation, and the FDA subsequently reverted the regulatory language in its own rulemaking. These developments reasserted CMS/CLIA as the primary regulatory authority for LDTs. However, as of 2026, no broad enforcement-discretion policies have been reintroduced to fill the immediate guidance gap.

Laboratory Developed Tests (LDT) Market

Concurrently, reimbursement mechanics continue to evolve — for example, updates to the Clinical Laboratory Fee Schedule (CLFS) in 2026 adjusted several clinical laboratory travel codes. The combined regulatory-reimbursement dynamic means that market participants must plan for a multi-year period of legal and policy uncertainty: the practical consequence is that test innovators, laboratory operators, and payers will rely more heavily on contractual solutions, supplemental evidence generation, and staged commercialization plans rather than assuming a stable regulatory endpoint.

Our report contains a regulatory-impact modeling engine that quantifies the revenue and EBITDA sensitivity to changes in (a) oversight assignment, (b) time-to-coverage by major payers, and (c) incremental evidence costs required to achieve reimbursable status.

The LDT market in 2026 exhibits meaningful concentration among established operators while leaving strategic room for specialist innovators. Market-concentration measures indicate that the top three players account for roughly 60% of the market, and the top five approach roughly 80% — a structure that rewards scale in network effects, payer relationships, and lab logistics, while leaving adjacent niches for differentiated, higher-margin tests.

Key strategic profiles we examined in detail:

Strategically, incumbents with scale will focus on margin defense, payer contracting, and lab-network optimization. Specialist innovators must emphasize clinical differentiation, path-to-coverage playbooks, and selective partnerships with larger lab networks to achieve commercial scale without ceding pricing control.

We expect continued M&A activity characterized by three archetypes: bolt-on acquisitions that fill capability gaps (e.g., adding a niche sequencing capability), platform roll-ups that aggregate regional labs to capture scale economics, and strategic JVs between diagnostic innovators and payer/health-system partners to embed tests into care pathways. Valuation multiples in 2026 will be sensitive to the perceived regulatory tail-risk and to near-term payer coverage prospects. Our transaction models quantify how changes in time-to-coverage and evidence spend change net present value and payback periods for each archetype.

Investors should seek assets with demonstrable clinical differentiation, defensible data assets, and credible commercialization pathways with phased reimbursement outcomes. Strategic buyers should prioritize targets that enable cross-selling, improve margin structure, or accelerate entry into priority clinical segments.

This research is built to convert market projections into board-room certainty. It combines a transparent macro forecast (2020–2025 historicals and a 2026–2032 forecast), scenario-based risk modeling tied to regulatory and reimbursement shocks, and operational playbooks that translate high-level strategy into executable 90‑ to 720‑day plans. Critically, while this article outlines the market shape and competitive dynamics, the full report contains granular segmentation, country- and payer-level matrices, downloadable financial models, and complete company dossiers that are necessary to execute transactions and board-level decisions.

We intentionally preserve certain granular segment-level figures and regional splits for the full report: that level of detail is where transaction valuation, contract negotiation, and tactical planning derive their precision. Treat this piece as a strategic trailer — it demonstrates the depth of our work, the rigor of the models, and the immediate paths to action, and it points you to the full dataset and playbooks you will need to operationalize decisions in 2026.

For access to the complete report, segmented forecasts, and the downloadable financial and regulatory models that underpin these conclusions, visit PW Consulting’s Laboratory Developed Tests market research page or contact our diagnostics strategy team. The full intelligence package is structured to move you from insight to decision within weeks — not quarters.

For detailed analysis of this topic, please visit the official page:Laboratory Developed Tests (LDT) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com