Could Travel Comfort Trends Accelerate the Inflatable Pillow Market?

Networking |

2026-07-07 11:12:50

As companies calibrate capital allocation and operational strategies for 2026, the GDNASH Market report provides a timely, evidence-based compass. Our base-year assessment (2025) synthesizes historical performance across 2020–2025 and projects the market through 2032. The market has expanded materially since 2020 and—on the trajectory we model—continues to grow at a compound annual growth rate of roughly 7% over the forecast window. By 2032 the market is forecast to be materially larger than it was in 2025, underscoring sustained demand drivers and structural tailwinds that matter to buyers, suppliers, and investors alike.

GDNASH Market

Budgeting and Capex: A near‑7% CAGR implies organizations should plan for steady procurement and maintenance spend increases through the late 2020s. Capital planning that assumes flat demand risks both underinvestment in reliability and missed opportunities to lock favorable pricing.

GDNASH Market

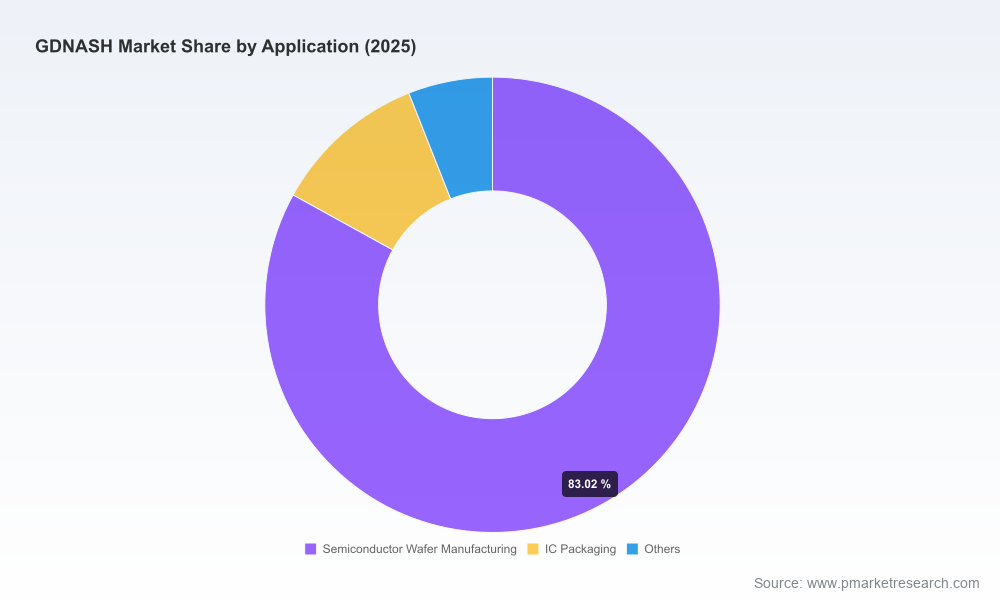

Supply‑chain resilience: The market remains relatively fragmented—leading firms capture only a modest share of total demand—so procurement teams must balance the efficiencies of single‑vendor service models against the resilience benefits of diversified sourcing.

GDNASH Market

Regulatory and energy cost pressure: Compliance regimes and energy cost volatility are already reshaping supplier value propositions (efficiency, explosion-proof certifications, emissions controls). Buyers who prioritize regulatory readiness in 2026 will avoid retrofitting costs and project delays.

Service economics: Long‑term service programs and OEM-backed uptime contracts shift the economic balance from one‑off purchases to predictable lifetime cost models—critical for industrial assets where downtime is a primary margin risk.

PW Consulting’s model captures yearly market sizing from 2020 through the 2025 base and delivers a full forecast to 2032. The pattern from 2020 onwards shows recovery and differentiated growth episodes—reflecting cyclical demand in heavy industrial and environmental applications and step‑changes driven by new compliance requirements and decarbonization initiatives. We present top‑line figures and growth metrics in this preview to inform 2026 strategies, while the report itself contains the granular segmentation that supports transaction‑grade decisions.

Robust market sizing and scenario models: base, upside, and downside pathways calibrated to demand drivers, energy price scenarios, and regulation timelines.

Decision frameworks for buyers: total cost of ownership (TCO) calculators, service vs. capex break‑even analysis, and a procurement playbook for negotiating OEM service programs.

Supplier diagnostic tools: scorecards for performance, compliance readiness, and aftermarket capability—designed for rapid comparison during RFPs and pre‑bid diligence.

M&A and investment filters: a shortlist methodology that ranks targets by technology defensibility, installed base quality, and growth adjacencies.

Operations guidance: reliability‑centered maintenance templates, digital sensor adoption roadmaps, and retrofit decision trees that show when to renew vs. replace.

The competitive topology is shaped by a combination of global OEMs, long‑standing regional specialists, and service‑focused players. Notably, Gardner Denver Nash LLC (headquartered in Trumbull, Connecticut) remains a highly visible incumbent. Their product breadth—liquid ring vacuum pumps, liquid ring compressors, steam jet ejectors, hybrid vacuum systems, and engineered process vacuum & compressor systems—positions them strongly across chemical, power, environmental, and wastewater treatment applications. Their installed base and systems integration capability are strategic assets when buyers prioritize turnkey solutions and integration into process automation.

Recent commercial developments illustrate tactical moves that matter to 2026 planning: late‑2025 intent notices in municipal wastewater procurement signal momentum for bundled supply and service agreements, while case studies from large OEMs demonstrate the role of classic technologies in decarbonization use cases (for example, evolving carbon capture pilot applications). For procurement leaders, these developments underscore the need to assess both product technical fit and the commercial terms that govern aftermarket availability and spare parts sourcing.

Efficiency and energy intensity: Suppliers are increasingly competing on operating cost reduction. Equipment choices that reduce power draw and simplify routine maintenance materially improve project economics for industrial buyers—especially where energy costs are a dominant line item.

Certification and safety: Explosion‑proof and industry‑specific certifications (e.g., ATEX) are non‑negotiable in hazardous environments. Buyers should require certification roadmaps and audit trails as part of procurement evaluation criteria.

Standards and integration: Compliance with recognized industry standards—together with the ability to integrate steam ejectors and vacuum systems into automation stacks—lowers installation cost and shortens commissioning timelines.

Service and workforce: OEM programs that combine remote diagnostics, preventive maintenance, and predictable parts supply reduce unplanned downtime and labor intensity—a decisive advantage where skilled technicians are scarce or costly.

Vendor concentration risk: Where single‑source intentions become de facto policies, buyers should secure robust contractual protections (SLA’s, parts escrow, transition assistance) to avoid operational dependency shocks.

Commodity and energy shocks: Scenario plans should include energy price hedging for high‑intensity sites and clauses to renegotiate long‑term supply contracts if input costs materially diverge from budget assumptions.

Regulatory catch‑up: Projects that assume lenient regulatory timelines face rework; include regulatory contingency buffers in project schedules and budgets.

Technology obsolescence: Prioritize modular and upgradeable architectures so capacity and control upgrades can be phased without full system replacement.

For corporate procurement: Build a two‑track sourcing strategy—short‑term tactical agreements to secure parts and service, plus a medium‑term competitive process that evaluates lifecycle costs and resilience metrics.

For operations leaders: Launch pilots that couple energy‑efficiency upgrades with remote monitoring to validate TCO improvements before full roll‑out.

For OEMs and service providers: Expand certified aftermarket programs, publish transparent uptime commitments, and invest in digital OEM‑assisted maintenance services as a recurring revenue lever.

For investors and M&A teams: Use the report’s filter to identify targets with high retrofit potential and durable service revenues rather than cyclical new‑equipment sales alone.

The GDNASH Market report balances empirical market sizing with operational, procurement, and competitive intelligence tailored for 2026 decision cycles. The macro trajectory—steady growth from our 2025 base and consistent mid‑single‑digit CAGR through 2032—provides a strategic backdrop. However, the value for practitioners lies in the report’s actionable deliverables: scenario models, supplier scorecards, and procurement playbooks designed to be applied directly to live decisions.

This preview deliberately highlights themes and strategic implications while withholding the full set of granular segment tables and supplier benchmarking data to preserve the practical leverage of the underlying intelligence. For the complete datasets, downloadable models, and the supplier benchmarking dashboard that supports transaction‑grade work, access the full GDNASH Market report on our publication page.

For detailed analysis of this topic, please visit the official page:GDNASH Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com