10 Steps To Purchase Old Github Accounts In Bulk (Pva & ...

Film |

2026-07-07 09:19:04

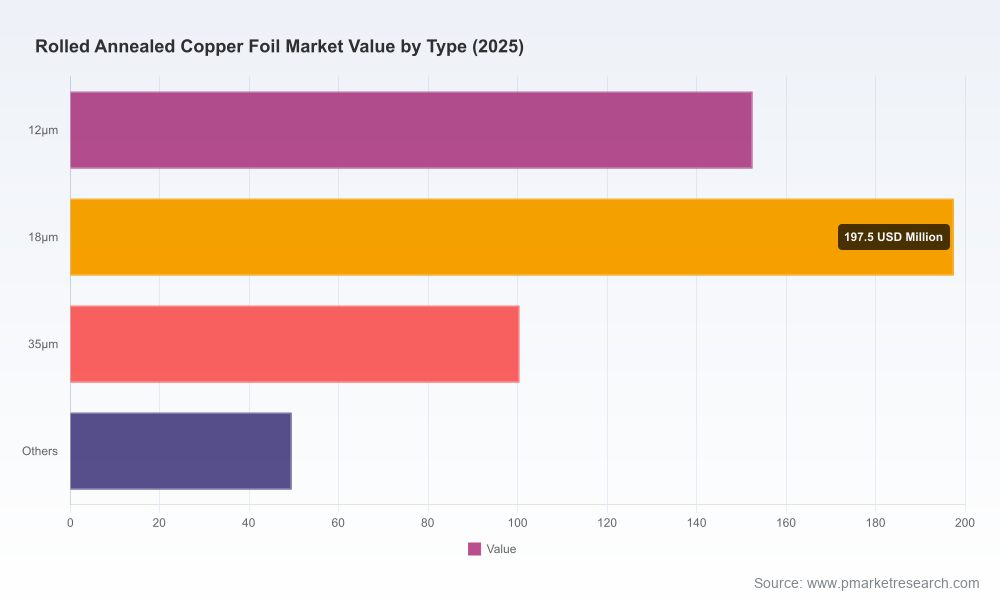

PW Consulting’s latest market study on Rolled Annealed (RA) Copper Foil provides a focused, actionable vantage point for executives making allocation, sourcing, and product strategy decisions in 2026. Grounded in a 2020–2025 historical base and a 2026–2032 forecast horizon, the research combines quantitative market sizing, competitive mapping and scenario-driven dynamics modeling to translate raw industry signals into clear commercial levers. Key headline metrics from the study: the RA copper foil market reached USD 500 Million in 2025 and, at a compound annual growth rate (CAGR) of 4.5%, is projected to expand to an estimated USD 640 Million by 2032. These aggregated numbers frame a steady growth trajectory with episodic volatility driven by raw-material, regulatory and battery-sector forces.

Rolled Annealed Copper Foil Market

Near-term capital discipline: With the market inching past the half‑billion dollar mark in 2025, procurement and operations teams must balance incremental capacity against cyclical price exposure. The report quantifies the sensitivity of revenue and margins to copper-price moves and offers break‑even and utilization scenarios tailored to common RA-foil production profiles.

Rolled Annealed Copper Foil Market

Supplier and concentration risk: The market exhibits moderate consolidation — the top three firms account for a substantial share of supply and the top five further extend that concentration. For corporates evaluating single-source exposure, the study provides supplier risk heatmaps and mitigation pathways suited for 2026 contracting cycles.

Rolled Annealed Copper Foil Market

Technology and application planning: The report translates product-level differentiation (ultra-thin and high‑temperature variants, battery‑grade substrates, roll‑clad hybrids) into go-to-market choices, helping R&D and product management prioritize investments that match demand elasticity across flexible electronics, PCBs and energy-storage segments.

Regulatory and procurement playbook: Growing regulatory tightness (recycled-content rules, export controls, tariff petitions) is reshaping sourcing geographies and compliance costs. The study offers scenario templates that quantify the operational and cost impact of plausible 2026 regulatory outcomes and prescribes procurement contract clauses to protect margins.

From a base of roughly USD 360 Million in 2020, the RA copper foil market has shown resilient expansion through 2025, arriving at approximately USD 500 Million in that base year. Our 4.5% CAGR projection to 2032 signals a market that will grow steadily rather than explosively, implying that winners will be those who optimize unit economics, control input-cost exposure and capture premium applications rather than relying solely on volume growth. The forecast path — with incremental increases year-on-year to an estimated USD 640 Million by 2032 — highlights the importance of multi-year planning for capacity, inventory and long‑lead equipment purchases.

Input-cost volatility: Early 2026 saw copper prices spike, and subsequent intrayear swings have materially impacted foil pricing and procurement budgets. The report models both extreme and mean‑reversion copper price scenarios, showing how operating margins and contract competitiveness respond across common hedging strategies.

Export and trade policy shifts: Tighter export controls in key producing countries and active lobbying by downstream semi‑fabricators over tariff exemptions are already changing the calculus for global sourcing. PwC-style scenario matrices in the study enable decision-makers to stress-test sourcing networks under alternative trade-policy regimes.

Regulatory sustainability pressures: European OEMs are increasingly requiring higher recycled-content certifications in alignment with evolving battery and product-directive regulations. For manufacturers and converters, compliance is becoming a commercial differentiator — the report quantifies premium capture potential for certified recycled products.

Strategic partnerships and vertical integration: Recent agreements and partnerships across the value chain signal a trend toward integrated supply solutions for battery and EV OEMs. The study evaluates the economics and timing of strategic supply agreements, roll-to-roll partnerships and selective vertical moves.

The RA copper foil market blends global incumbents with regional leaders. Our competitive profiling focuses on capabilities that matter to 2026 buyers: ultra-thin foil production, battery-grade substrate supply, treated/high‑tensile alloys, and certification/compliance readiness.

Wieland Rolled Products NA (USA) — Strength in rolled and surface-treated foils across a broad thickness range and global roll/sheet logistics. Attractive for partners who need scale and consistent supply in the Americas.

Targray (Canada) — A leading North American supplier of battery‑grade RA foils and high‑tensile variants; strong positioning for energy‑storage and EV cell manufacturers seeking certified substrates and reliable roll-clad supply.

JX Nippon Mining & Metals (Japan) — Specialist in ultra‑thin RA foils (12 μm, 18 μm) for flexible electronics and premium consumer and aerospace applications. Their technical focus makes them a preferred supplier where electrical performance and thinness are differentiators.

Furukawa Electric, Mitsui Kinzoku and Sumitomo Metal Mining (Japan) — Collectively, these firms bring advanced specialty grades (high-temperature elongation, micro‑thin variants) and deep downstream relationships with PCB and automotive OEMs; they are strategic partners for customers prioritizing reliability under thermal stress.

Olin Corporation (USA) and select Chinese producers — Provide broad industrial and electronics-grade rolled foils, with some regional advantages in cost and proximity. Chinese producers, in particular, contribute substantial capacity for Asia‑Pacific demand, though export controls and quality stratification are evolving factors.

Fukuda Metal Foil & Powder — Notable for certified 100% recycled copper foil offerings, responding directly to European OEM regulatory demands and potentially commanding a premium in regulated supply chains.

Collectively, the three largest suppliers capture a dominant portion of market supply and the top five extend that dominance further. That concentration means strategic supplier selection, long-term agreements and dual-sourcing constructs will be deciding factors for buyers working to secure continuity and leverage.

Granular, validated market sizing and a downloadable dataset for 2020–2032 (aggregate and by report-defined commercial buckets), plus a transparent methodology that senior procurement and strategy teams can audit.

Supplier scorecards and a procurement playbook — including negotiation benchmarks, contract structures (take-or-pay, indexation to copper benchmarks), and lead-time/quality risk matrices.

Price-sensitivity and margin-impact models tied to realistic copper-price scenarios, with recommended hedging and inventory strategies aligned to corporate risk tolerances.

Regulatory scenario maps that quantify the operational and cost impact of export-control regimes and recycled-content mandates, with recommended compliance architectures for near-term implementation.

Commercial go-to-market guidance for capturing premium segments (ultra‑thin, HTE, battery-grade) and a product roadmap to prioritize engineering investments that yield the highest near-term ROI.

Portfolio-level acquisition and partnership screening tools — for buy, build or partner decisions — including payback timelines, integration risk checklists and sample term-sheets used by leading PE and strategic acquirers.

Reassess supplier portfolios now — model the P&L impact of single-supplier disruptions and put dual‑source contingency plans in place for high‑criticality feeds.

Lock in strategic pricing mechanisms — use indexation to copper benchmarks combined with collars or caps to protect margins during the current price volatility cycle.

Prioritize certification and sustainability claims — secure recycled-content chain-of-custody documentation if you sell into regulated OEMs in Europe.

Run selective make-versus-buy exercises for premium foil grades where intellectual property and process control materially differentiate product performance.

Monitor policy developments and maintain a regulatory playbook — build clauses into contracts that protect against material changes in export or trade policy.

Between 2026 and 2032 the RA copper foil market will reward firms that convert scale and technical differentiation into repeatable commercial advantage. The growth path is steady, not runaway; therefore, strategic advantage will more likely come from operational excellence, disciplined procurement and targeted product innovation than from speculative capacity expansion. PW Consulting’s study equips executives with the quantitative tools and scenario-tested playbooks to make those calls with conviction.

Note: This article highlights the study’s strategic frames and topline market trajectory. Detailed segment-level splits, company share tables and the full dataset are intentionally withheld here to preserve the report’s commercial core — access to the complete analysis, granular segmentation and downloadable models is available in the full PW Consulting Rolled Annealed Copper Foil Market report.

For detailed analysis of this topic, please visit the official page:Rolled Annealed Copper Foil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com