Helicobacter pylori Diagnostics Market — Strategic Preview for 2026 Corporate Decision-Makers

Introduction

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused, decision-oriented preview of our latest Helicobacter pylori (H. pylori) Diagnostics Market research. This briefing synthesizes the macro trajectory, regulatory inflection points, competitive moves, and the pragmatic commercial playbooks that matter to companies planning budgets, R&D, market access, and M&A activity in 2026. The aim is to demonstrate the analytical depth you will find in the full report while intentionally withholding the granular segmented datasets that are available in the source publication.

Helicobacter Pylori Diagnostics Market

Market snapshot: growth trajectory and what it means

The H. pylori diagnostics market has moved from a mid-single-hundred million USD industry in 2020 into a stronger, expanding market by the 2025 base year. Our topline historical series shows consistent year-on-year expansion driven by a combination of higher testing volumes, broader adoption of non-invasive modalities, and a gradual shift toward molecular and point-of-care (PoC) testing. The market is projected to continue expanding at a compound annual growth rate (CAGR) of approximately 5.9% over the forecast window 2026–2032, reaching materially higher levels by the end of the period.

Helicobacter Pylori Diagnostics Market

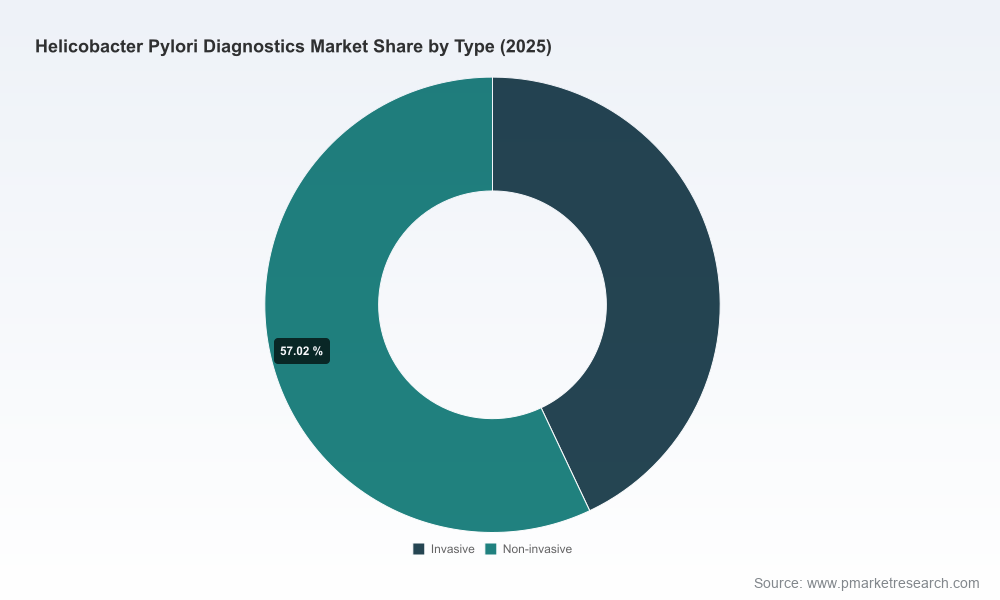

Two structural forces underpin this outlook: first, clinical pathways increasingly emphasize test-and-treat strategies and antimicrobial stewardship (which together raise demand for diagnostics that can detect infection and, where possible, resistance markers); second, technological and commercial innovations — rapid stool antigen tests, breath test systems with simplified workflows, home-use kits, and compact PoC molecular instruments — are expanding addressable care settings beyond specialist gastroenterology units into primary care and at-home testing.

Helicobacter Pylori Diagnostics Market

Regulatory and reimbursement dynamics shaping 2026 plays

- Reimbursement is a gating factor for commercial expansion. Public payer coding updates implemented in recent years have created clearer billing pathways for combined detection and clarithromycin resistance testing using amplified probe techniques. That change materially influences lab adoption and commercialization strategies for molecular diagnostic suppliers.

- Specific HCPCS and CPT code updates remain consequential for product economics: legacy codes for breath test analysis and administration continue to exist in payer fee schedules with modest average Medicare payments. Companies that structure bundles, ancillary services, or differentiated value propositions (e.g., pediatric-friendly devices, home-testing convenience) can offset modest per-test reimbursement through higher volume and integrated revenue models.

- Regulatory approvals and regional registrations — from MHRA clearances to country-level approvals for home use — are accelerating route-to-market options. These regulatory wins matter more than ever because they unlock non-traditional channels (retail pharmacies, direct-to-consumer) and support premium pricing in consumer-facing formats.

Strategic implications for 2026 decision-making

Executives and investors need to translate the market facts into prioritized, time-bound choices. The research frames the following implications that should inform 2026 planning cycles:

- Product prioritization: Prioritize R&D and commercialization of assays that combine diagnostic performance with operational simplicity — rapid stool antigen platforms, resilient PoC molecular assays, and breath systems that minimize clinical overhead.

- Market-access and coding playbook: Build a reimbursement roadmap that targets the most relevant billing codes and identification of payer-specific coverage criteria. Early engagement with payers and centralized labs will shorten adoption cycles.

- Channel strategy: Accelerate partnerships with primary care networks, retail pharmacy chains, and digital health platforms to capture the shift to decentralized testing. Home-use registrations create a distinct commercial channel that can leapfrog traditional distribution constraints.

- M&A and partnership targeting: Use scenario-based valuation models to screen acquisition targets that offer adjacent capabilities (e.g., pediatric-clearance breath systems, rapid urease biopsy assays, or validated home antigen kits), given the market’s moderate concentration and continuing consolidation trends.

- Commercial model optimization: Given modest per-test reimbursement in some payer systems, volume-driven strategies, bundled service offerings, and recurring-revenue consumable models will deliver healthier unit economics than one-off capital equipment sales.

- Clinical positioning and stewardship: Align product claims and evidence generation with antimicrobial stewardship initiatives and clinical guideline updates that prioritize resistance detection — this materially improves the value narrative for payers and hospital formularies.

Competitive landscape — who to watch and why

The market combines established diagnostic suppliers with focused niche players. Competitive positioning varies across technology modalities (stool antigen, breath testing, rapid urease tests, molecular diagnostics) and across go-to-market models (lab channel, PoC, home use). A few illustrative company positions and strategic moves captured in our research:

- Meridian Bioscience (Cincinnati, Ohio) maintains a diversified product set across stool antigen and urea breath modalities. Their offerings emphasize preserved-sample compatibility and clinically validated workflows that appeal to centralized labs and reference testing networks.

- Gulf Coast Scientific (USA) has differentiated through pediatric-focused regulatory clearance for its PyloPlus breath test system — a commercially valuable niche that opens partnerships with pediatric care providers and children’s hospitals.

- Biomerica (Irvine, California) is actively expanding market access and consumer reach: recent approvals for home-use formats in select markets and MHRA registration for key products point to an explicit strategy to commercialize direct-to-consumer and retail channels.

- Alpha Laboratories (United Kingdom) has invested in rapid stool-based EIA technology that targets fast turnaround in outpatient settings; product launches focused on 10‑minute results are tailored to busy primary-care workflows.

- BIOHIT (Finland) offers a surgical/biopsy-oriented rapid urease test with extremely fast readouts, serving endoscopy suites and surgical diagnostics where time-to-result at biopsy matters.

Collectively, market concentration metrics indicate a moderately consolidated market at the top (CR3 and CR5 in our analysis), which presents both a barrier and an opportunity: barriers in terms of established distribution and scale, and opportunity for nimble entrants to capture high-growth niches (pediatrics, home testing, PoC molecular). The full report juxtaposes firm-level scorecards, pipeline maps, and win-loss analyses that are essential for benchmarking.

Illustrative recent developments and their strategic read

- Regulatory approvals for home-use and regional registrations have begun to shift the market from facility-bound testing toward consumer-accessible formats — a dynamic that favors companies with regulatory prowess and retail partnerships.

- New rapid stool antigen products and ultra-fast biopsy urease tests lower clinical friction and shorten care pathways; these can reconfigure procurement decisions in clinics and endoscopy units.

- Payer code updates for detection plus clarithromycin resistance materially raise the commercial value of molecular platforms that can deliver resistance information, which in turn makes targeted investment in multiplexed assays more defensible.

What the full report delivers (practical, actionable assets)

The complete PW Consulting report is structured to support operational decision-making in 2026. Highlights include:

- Validated topline market sizing and history (2020–2025) with scenario-based forecasts (2026–2032) and sensitivity analyses keyed to utilization, pricing, and reimbursement variables.

- Technology and product taxonomy with adoption curves, time-to-adoption estimates by care setting, and impairment-risk scoring for legacy modalities.

- Regulatory and reimbursement playbooks: step-by-step market-entry checklists, payer engagement templates, and a coding-impact model tailored to major public payers.

- Competitor benchmark dossiers: product portfolios, price-positioning matrices, clinical evidence comparators, distribution footprints, and recent strategic moves mapped to tactical recommendations.

- Commercial due diligence modules for investors: EBITDA impact scenarios, acquisition integration checklists, and five-year synergies playbooks.

- Customer and channel playbooks: procurement negotiation points, laboratory adoption decision trees, and retail pharmacy roll-out templates.

How to use this intelligence in 2026 planning cycles

Practical next steps for leadership teams and investors:

- Run three internal scenarios (base, accelerated adoption, technology-disruption) using the report’s forecast model to stress-test investment cases and capital allocation for 2026.

- Prioritize reimbursement initiatives early in product development; align clinical trials and evidence generation with payer decision criteria identified in the report.

- Pursue targeted partnerships for home-use and pediatric channels where regulatory clearance speed confers outsized commercial advantage.

- If M&A is on the table, use the provided screening criteria and scorecards to shortlist tuck-in assets that close capability gaps (e.g., PoC molecular, pediatric breath systems, or validated home antigen kits).

- Update sales incentives and distributor agreements to reflect volume-led economics and the shift to consumable-driven margins.

Conclusion — why this matters right now

Entering 2026, the H. pylori diagnostics market is no longer a niche lab business: it is evolving into a multi-channel, clinically important category influenced by stewardship priorities, payer coding updates, and technological diversification. Strategic decisions made this year — about product roadmaps, regulatory investments, channel partnerships, and acquisition targets — will determine who captures the higher-growth segments over the next five years.

This preview is designed to show the kind of actionable depth contained in our full study while preserving the granular segmented intelligence that drives precise go-to-market plans. For the complete datasets, product-level forecasts, competitive market shares, and the downloadable financial and scenario models required to execute on the strategies outlined here, please consult the full PW Consulting Helicobacter pylori Diagnostics Market report and schedule a tailored executive briefing.

For detailed analysis of this topic, please visit the official page:Helicobacter Pylori Diagnostics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com