Platinum-Based Cancer Drug Market — Strategic Outlook for 2026 Decision-Makers

PW Consulting’s Platinum Based Cancer Drug Market study is designed as a decision-grade intelligence product for executives planning capital allocation, portfolio positioning, and operational resilience in 2026 and beyond. The study synthesizes primary interviews, proprietary sales audits, and a bottom‑up financial model to deliver both directional foresight and immediately actionable recommendations. Below we outline why this study matters this year, the headline macro trajectory, the competitive dynamics you must plan for, and the practical deliverables inside the full report. This preview demonstrates our analytical depth while withholding the full subsegment tables and share matrices to encourage direct access to the complete dataset.

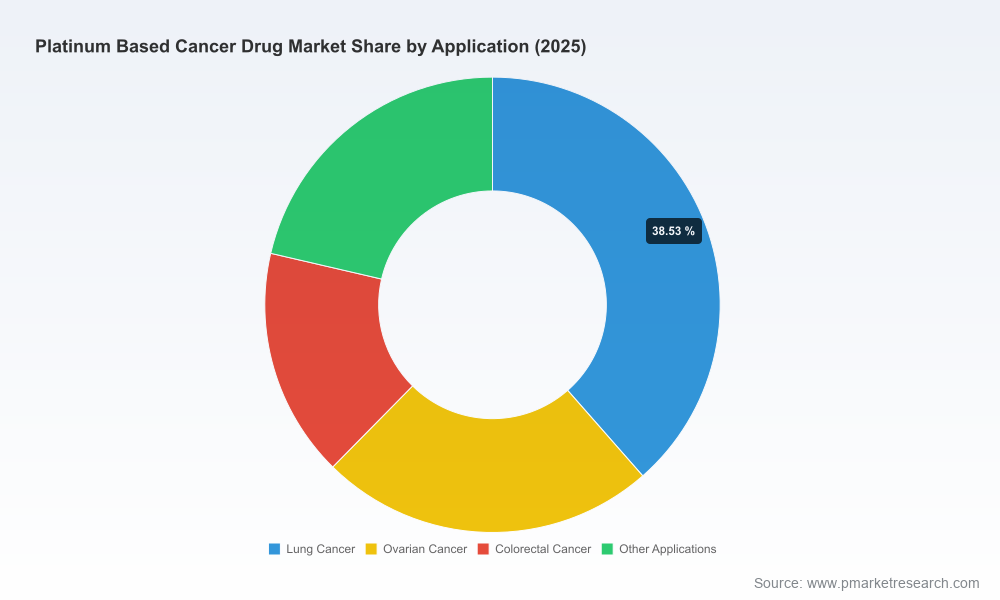

Platinum Based Cancer Drug Market

Headline macro picture — what the numbers say

The platinum‑based oncology market has displayed steady expansion through the early 2020s, reflecting continued clinical reliance on platinum agents across multiple tumour types and a slow-but-persistent re-uptake in volumes following pandemic disruption. Using 2025 as the base year, PW Consulting’s model shows the market expanded from USD 143.25 Million in 2020 to USD 176.75 Million in 2025, and projects steady growth through the forecast window (2026–2032) to reach an estimated USD 224.15 Million by 2032. This projection is driven by a compound annual growth rate (CAGR) of 3.45% over the forecast period (currency: USD, revenue unit: Million).

Platinum Based Cancer Drug Market

For 2026 planning, the implication is straightforward: the market is not returning to hypergrowth, but it is stable and investible. That profile favors disciplined, capital-efficient moves — targeted M&A, contract manufacturing expansions with conditional capacity triggers, and differentiated clinical development that can convert longstanding chemotherapies into higher-value therapeutic combinations or indication‑specific formulations.

Platinum Based Cancer Drug Market

Why this report is strategically valuable in 2026

- Operational resilience planning: The study quantifies supply‑chain fragility and API dependencies that re-emerged in 2025 and recommends risk-mitigating sourcing and inventory strategies.

- Pricing & reimbursement intelligence: We map observed price erosion following generic entry and show breakeven levers for manufacturers at local price caps — essential for decisions on plant upgrades or geographic entry.

- Portfolio prioritization: We provide a scenario framework to assess branded portfolio hold-versus-divest choices and to identify where modest R&D or lifecycle investments can materially improve returns.

- M&A and partnership playbooks: The report contains valuation sensitivity tables that factor in manufacturing viability, regulatory risk, and short‑term supply interruptions — enabling faster, better informed deal gating.

Key market dynamics and risk drivers

Four dynamics dominate risk and opportunity for platinum‑based oncology products in 2026:

- Supply‑chain and API concentration: Shortages reappeared in 2025, tied to a constrained manufacturer base and overseas API bottlenecks. Our operational risk scoring identifies the most critical nodes and quantifies the financial exposure of single‑source dependencies.

- Input cost pressures: Rising platinum metal prices in certain production hubs have already rendered some generic manufacturing economically unviable under local MRP regimes. The result: selective attrition of low-margin producers, and a near-term window where capacity rebalancing creates both disruption and opportunity for players with flexible cost structures.

- Reimbursement & pricing pressure: Genericization has materially compressed realized prices in mature markets; in the United States, post‑branded generic pricing has settled into a low monthly cost band for many agents. That dynamic forces strategic choices between competing on price, on-service (supply guarantees, storage), or on added clinical differentiation.

- Regulatory events and clinical re‑positioning: Orphan designations and new indication filings (including a recent Orphan Drug Designation for oxaliplatin in pancreatic cancer in May 2026) can reframe product economics, creating premium value pools for incumbent or enterprising sponsors.

Competitive landscape — how to interpret the players

The market combines large multispecialty originators with a broad base of generic injectables producers. Key firms profiled in the report include both global branded firms and leading generics/CMO names. Each requires a distinct strategic posture:

- Pfizer Inc. (New York, NY): A global branded player with legacy oncology offerings. Strategic advantage: integrated commercialization infrastructure and access to combination therapy trials; challenge: defending margin in mature categories.

- Bristol‑Myers Squibb (New York, NY): Broad oncology portfolio and high regulatory sophistication. Strategic focus: leveraging clinical pipelines to extend the value of legacy chemotherapies within combination regimens.

- Sanofi (Paris): Established presence in chemo portfolios and strong global reach; potential acquirer for manufacturing assets to shore up supply chain resilience.

- Johnson & Johnson Services (New Brunswick, NJ): Large hospital channel footprint; competitive edge in institution-level contracting and long-term supply agreements.

- Teva, Hikma, Mylan (now part of larger generics groups), Accord, Fresenius Kabi, Sun Pharma: These generics and injectable specialists drive price competition and provide the bulk of manufacturing capacity. Strategic implications: high‑value opportunities exist in contract manufacturing, supply guarantees, and geographic arbitrage where local pricing regimes support sustainable margins.

Across this field, the combination of branded R&D muscle and generics manufacturing scale produces a market where strategic wins are often operational rather than purely clinical: securing API supply, ensuring sterile injectable capacity, and structuring long-term hospital or national tender relationships.

Recent developments that matter for boardroom decisions

- 2025 shortages reappeared for cisplatin in several healthcare systems — an early warning sign for procurement and capacity planning.

- Regulatory moves to incentivize new uses for established agents (e.g., orphan designation for oxaliplatin in pancreatic cancer in 2026) can change valuation calculus for product holders or entrants targeting niche, high‑value indications.

- Where local raw material or labor cost inflation makes production uneconomic, expect consolidation among smaller suppliers and potential spot‑market volatility in supply and price.

What’s inside the full PW Consulting study (operational deliverables)

- Comprehensive market sizing and a bottom‑up model (base year 2025; historical 2020–2025; forecast 2026–2032) with downloadable data tables in USD Million.

- Supply‑chain vulnerability map and mitigation playbook, including alternative API sourcing options, critical lead times, and recommended inventory buffers by manufacturing footprint.

- Price and reimbursement overlays by market archetype, with price‑sensitivity elasticities and break‑even models for branded and generic manufacturers.

- Competitive scorecards for leading firms (branded and generics) with capability matrices, commercial levers, and plausible near‑term strategic moves.

- Regulatory & clinical event tracker and value impact estimates (including orphan designations, shortage‑list movements, and generic entry timing scenarios).

- Transaction playbooks: valuation ranges under three scenarios (status quo, consolidation, and clinical re‑positioning) and an M&A due diligence checklist tailored to platinum‑agent assets.

How different stakeholders should use this intelligence in 2026

- Pharmaceutical executives: Use the report to prioritize manufacturing investments and to model the ROI of differentiated formulations or combination trials that can justify premium pricing.

- CMOs and suppliers: Identify where capacity expansions yield the highest margin-adjusted returns, and which contracts to target to secure counter‑party stability.

- Private equity and corporate development: Leverage our valuation scenarios and due diligence checklists to accelerate deal screening and to price contingent liabilities associated with supply‑chain and regulatory risk.

- Hospital procurement and payers: Apply the supply‑chain heatmap and shortfall scenarios to redesign tender strategies and contingency stock plans for chemotherapy continuity.

Next steps — how to get the full dataset

This preview purposefully omits the granular region, type and application splits, and competitor share tables that underpin our financial model. Those subsegment matrices and downloadable datasets are included in the full report and are essential for transaction or procurement execution—particularly if you require regional tender modeling, indication‑level revenue waterfalls, or counterparty concentration metrics.

For 2026 planning, the two pragmatic actions we recommend now are: (1) commission a short‑term supply audit against your product portfolio and counterparties to surface single‑source exposures, and (2) run a price‑sensitivity stress test of your manufacturing footprint versus plausible platinum price and labor‑cost scenarios. PW Consulting’s full Platinum Based Cancer Drug Market study contains the calibrated inputs and scenario models necessary to run both exercises rapidly and to translate outcomes into board‑level recommendations.

To obtain the complete report, including the withheld subsegment tables, playbooks, and downloadable models, visit the PW Consulting publications page or contact your engagement lead. Our analysts are available to run a tailored briefing for executive teams and to convert the findings into a 90‑day action roadmap aligned to your corporate priorities.

For detailed analysis of this topic, please visit the official page:Platinum Based Cancer Drug Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com