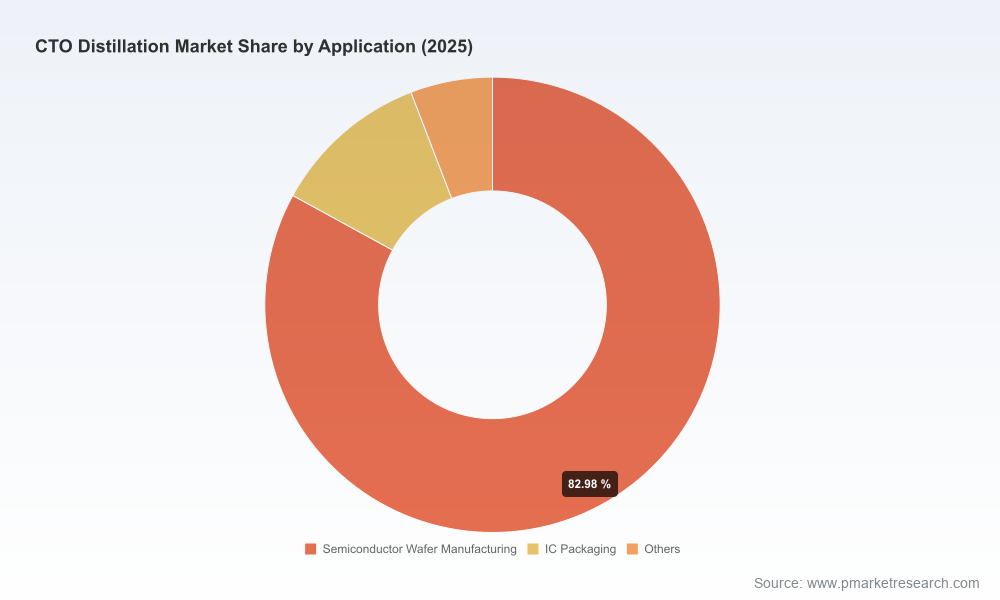

CTO Distillation Market: Strategic Imperatives for 2026 Decision‑Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused preview of our upcoming CTO Distillation Market study. This briefing distills the analysis you need to shape capital allocation, procurement, and go‑to‑market decisions in 2026 — while preserving the granular segment level intelligence that drives transaction‑grade actions for subscribers to the full report.

CTO Distillation Market

Executive snapshot: why CTO distillation matters in 2026

Crude Tall Oil (CTO) distillation sits at the intersection of forest supply chains, specialty chemicals, and decarbonization policy. Our base year is 2025, when the market reached approximately USD 215.0 Million. Under our central projection (2026–2032), the market grows at a compound annual growth rate (CAGR) of 5.6%, reaching roughly USD 344.8 Million by 2032. Those macro dynamics reflect more than organic end‑market growth; they encode regulatory stimuli, feedstock re‑rating, and a wave of asset reconfiguration that will determine competitive returns over the next investment cycle.

CTO Distillation Market

For executives making 2026 decisions, three facts are decisive: demand for CTO‑derived fractions is being re‑positioned by renewable fuel policy and chemical substitution mandates; feedstock volumes for distillation represent a substantial and consolidated flow in the forest products complex; and the incumbent producer base remains fragmented enough to create pockets of arbitrage and selective consolidation. Our study shows how these forces interact and where strategic value will be created.

CTO Distillation Market

Regulatory and market drivers to frame 2026 strategy

- Policy acceleration — CTO is explicitly recognized under several low‑carbon fuel and sustainability frameworks (including RED II and aviation carbon schemes such as CORSIA), creating durable demand corridors for certain fractions used in SAF and renewable diesel pathways.

- Chemical re‑rating — regulatory actions (notably a REACH designation recognizing tall oil fatty acids as a safer alternative to some petroleum‑derived chemicals) are increasing the willingness of formulators and brands to substitute toward CTO‑derived inputs.

- Incentives and support — national climate measures (e.g., U.S. Inflation Reduction Act and European Fit‑for‑55 policy instruments) alter the economics of bio‑based feedstocks and make capital projects and certification efforts commercially attractive in 2026.

- Price & supply volatility — CTO prices have risen since 2020 owing to uptake in biofuels and renewable diesel; this has meaningful consequences for margin management across the value chain.

What the full PW Consulting report delivers (practical contents)

Designed for strategy teams, corporate development, procurement heads and PE investors, the full study is action‑oriented rather than descriptive. Highlights include:

- Proprietary demand model and forecast (2026–2032) with scenario branches for SAF adoption, renewable diesel scale‑up, and polymer/adhesive substitution.

- Price decks and margin models for primary CTO fractions under multiple feedstock and energy price paths.

- Plant‑level economics and retrofit playbooks (vacuum distillation, energy recovery, and ISCC‑style certification pathways), including a template CAPEX/OPEX model for brownfield and greenfield options.

- Comprehensive supplier and asset registry with capability maps, operational KPIs and near‑term capacity shifts (transactions, upgrades, certifications) that alter regional processing balances.

- Regulatory risk matrix and commercial impact assessment (REACH, fuel standards, sustainability certification regimes), plus a stakeholder playbook for engagement.

- M&A & partnership playbook: integration risk checklist, valuation sensitivities, and three archetypal deal structures we see winning in 2026.

- Ten executable strategic moves for buyers, sellers and midstream processors tailored to 12‑ and 36‑month time horizons.

To preserve the utility of these near‑term actions for subscribers, we intentionally withhold the granular regional and application splits in this preview. The full report contains those tables and downloadable models.

Competitive landscape — what we see and what it implies

The CTO distillation producer set includes integrated chemical majors, specialized pine‑chemicals players, and focused refiners. Market concentration is modest: the top three players account for roughly a quarter of market revenue, and the top five scarcely increase that share — a structural signal that the sector remains fragmented and open to aggregation where scale and logistics create advantage (CR3 ≈ 24.6%, CR5 ≈ 26.2%).

Selected strategic observations on core suppliers (full company dossiers included in the report):

- Kraton Corporation — Following a material upgrade at its Panama City, Florida biorefinery towers (completed 2024) and subsequent ISCC PLUS certification in early 2026, Kraton has repositioned itself as a sustainability‑certified supplier of CTO fractions. Expect Kraton to target premium channels where certified bio‑feedstocks command a price premium and to pursue feedstock security strategies.

- Harima Chemicals Group — Harima’s closed‑loop tall oil distillation capability provides clear energy‑efficiency and lifecycle advantages. Their operational model is a useful benchmark for buyers seeking low‑GHG product profiles and stable operating costs.

- Forchem Oyj — Advanced vacuum distillation and fractionation expertise make Forchem a technological reference point; licensing or JV structures with regional players are likely routes for capacity expansion.

- Georgia‑Pacific Chemicals and Eastman Chemical — Both leverage scale, downstream channels and integration into coatings/adhesives value chains. Their move set is oriented toward product differentiation and long‑term contracts with formulators.

- DRT and Segezha Group — European and Eurasian specialists with deep access to pine‑chemicals markets. Their role is pivotal in regional supply continuity and in potential trade flows if policy or transport economics shift.

- Mainstream Pine Products — The completed acquisition of the North Charleston CTO refinery in January 2026 is a reminder that opportunistic consolidation is underway; buyers should model the economics of large single‑site additions carefully, especially when industrial specialties lines are included.

For investors, the fragmentation provides acquisition optionality; for corporates, it creates a buyer’s market in select geographies but a premium supply environment for certified and low‑GHG fractions.

Operational priorities and playbook for 2026

Our research translates into six immediate priorities for management teams:

- Secure feedstock: pursue medium‑term off‑take or co‑sourcing agreements tied to sustainability credentials to mitigate price shocks and regulatory risk.

- Certification strategy: evaluate ISCC/ISCC PLUS and equivalent schemes early — certification outcomes materially affect access to renewable fuel and premium chemical markets.

- Targeted CAPEX: prioritize energy recovery and vacuum distillation retrofits that raise yields and lower carbon intensity; use the PW CAPEX/OPEX template to stress test returns.

- Value capture: focus on higher‑value fractions and specialty derivatives where formulation demand and regulatory substitution dynamics favor CTO inputs.

- M&A discipline: look for bolt‑on assets with logistic synergies rather than trophy assets that require extensive integration capital.

- Policy engagement: actively shape fuel and feedstock policy at national and regional levels where certification definitions and counting rules are still being finalized.

Risks, sensitivities and unresolved questions

No projection is immune to volatility. Key exposure points we model explicitly are:

- Feedstock price spikes or shortages tied to competing biofuel markets;

- Regulatory reversals or reinterpretations that alter counting under fuel mandates;

- Trade or sanctions dynamics affecting timber and chemical flows in certain geographies;

- Technological disruption (e.g., alternative bio‑routes or synthetic substitutes) that compress margins.

Our full scenario suite quantifies profit‑and‑loss and NPV impacts for each risk and includes contingency hedging and procurement playbooks.

Methodology and data integrity

The analysis leverages a multi‑method approach: primary interviews with plant operators and large buyers, bottom‑up plant capacity and utilization modelling, trade and price data triangulated with company filings, and policy tracking. Historical coverage spans 2020–2025 with the forecast window 2026–2032; scenario branches capture divergent policy and demand outcomes. Where we present top‑line market revenue and concentration metrics in this preview, the granular segment tables, region/application splits and downloadable financial models are reserved for report subscribers to preserve commercial utility.

How PW Consulting can accelerate your 2026 program

We use the report as a launchpad for tailored engagements: bespoke forecasts for procurement tenders, acquisition target screening and valuation, certification roadmaps, or plant economic revaluations under client‑specific price assumptions. If you are evaluating capital projects, negotiating feedstock contracts, or preparing for an M&A play in 2026, our analysts can convert the report’s models into client‑specific decision‑support tools within a 2–4 week advisory engagement.

To access the full CTO Distillation Market report, the plant‑level asset register, and the downloadable CAPEX/OPEX models that underpin our forecasts, please visit PW Consulting’s insight portal or contact our industry team to request a briefing. The full report contains the detailed regional and application splits, unit economics, and transaction comparables that we have intentionally withheld in this preview to protect the actionable insight for subscribers.

In a market where policy choices, certification status and feedstock strategy determine premium access, 2026 will be a year of irreversible positioning. Use this preview as your operational checklist — then access the full report to convert strategy into execution.

For detailed analysis of this topic, please visit the official page:CTO Distillation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com