mRNA Cancer Vaccines and Therapeutics Market — Strategic Preview for 2026 Decision-Makers

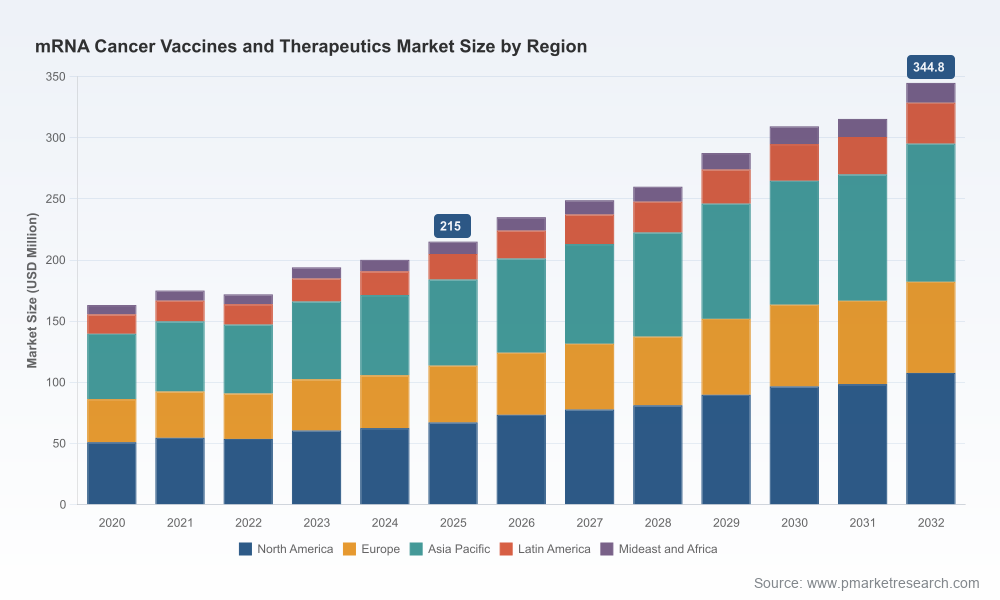

As mRNA technologies transition from pandemic response to precision oncology, companies face a concentrated set of strategic inflection points in 2026: late‑stage trial readouts, first commercial launches, decentralized manufacturing rollouts and payer negotiations. Our PW Consulting market study places this industry in context — the global mRNA cancer vaccines and therapeutics market, valued at approximately USD 215.0 Million in 2025, is forecast to grow at a compound annual growth rate (CAGR) of 6.98% through 2032, reaching roughly USD 344.8 Million by the end of the forecast window. This preview explains why that trajectory matters for near‑term corporate decisions, what operational capabilities gate commercial success, and how leading and emerging players are positioning themselves.

mRNA Cancer Vaccines and Therapeutics Market

What the full study delivers — a practical toolkit for 2026

- Actionable market sizing and growth scenarios calibrated to pivotal clinical timelines and likely regulatory milestones for 2026–2027 (including sensitivity analyses for accelerated vs. delayed approvals).

- End‑to‑end go‑to‑market frameworks: launch sequencing, commercial access playbooks, payer engagement roadmaps and HTA evidence requirements tailored to personalized vs. off‑the‑shelf models.

- Manufacturing and supply chain playbook covering centralized vs. decentralized (hospital/academic) GMP production, LNP sourcing strategies, fill‑finish choices and partnership architectures to de‑risk time‑to‑patient.

- Clinical & translational decision support: indication prioritization matrices that weigh unmet need, trial feasibility, biomarker maturity and likely time to reimbursement.

- Competitive and M&A intelligence: mapping of platform overlaps, complementary capabilities (sequencing, tumor‑profiling, delivery), and a seller/buyer heatmap for 2026‑era consolidation opportunities.

- Commercial scenarios and pricing models that integrate expected efficacy readouts, real‑world evidence (RWE) pathways and innovative contracting options (outcomes‑based, milestone payments) for payers and providers.

Why 2026 is a pivotal decision year

- Clinical inflection points: Several programs are reaching late‑phase readouts or delivering multi‑year follow‑up data that will materially change commercial probabilities. These outcomes determine near‑term regulatory filings and shape launch sequencing.

- Manufacturing readiness: The window to secure LNP suppliers, establish GMP capacity and validate decentralized production workflows must align with anticipated regulatory approvals in late 2026–2027.

- Payer engagement timing: Payers will demand robust value narratives and RWE plans before formulary decisions; companies that begin evidence generation and contract pilots now will shorten time‑to‑reimbursement after approval.

- Strategic capital allocation: With modest absolute market size today but high upside, boards must decide between aggressive platform investment, partnership‑led scale, or targeted niche plays where clinical differentiation is clearest.

Competitive landscape — who matters and why

The market is still early and relatively unconcentrated: leading developer‑manufacturers are setting scientific standards and playbooks rather than dominating commercial share. Key companies to watch and their strategic signals:

mRNA Cancer Vaccines and Therapeutics Market

- Moderna, Inc. (Cambridge, MA) — A platform leader advancing personalized mRNA cancer vaccines with late‑stage programs (notably intismeran autogene / mRNA‑4157). Recent multi‑year follow‑up data (June 2026) demonstrating substantial reductions in recurrence and distant metastasis materially strengthen commercial positioning for adjuvant indications and inform payer value arguments.

- BioNTech SE (Mainz, Germany) — Maintains diversified oncology pipeline spanning individualized and off‑the‑shelf approaches. The December 2025 acquisition of CureVac expands BioNTech’s platform depth and candidate pipeline (notably programs in glioblastoma), accelerating its vertical integration strategy.

- Providence Therapeutics (Calgary, Canada) — Focused on pediatric and high‑unmet‑need niches; their funding and initiation of the PaedNEO‑VAX multi‑site personalized trial (Feb 2026) signals first‑mover intentions in pediatric personalized vaccines.

- Gritstone bio, Inc. (South San Francisco) — Developing neoantigen personalized vaccines (e.g., GRANITE) for solid tumors; their approach highlights the clinical and operational challenges of individualized vaccine workflows and the potential upside where neoantigen targeting is validated.

Strategic takeaway: the competitive picture rewards platform breadth plus execution in manufacturing and payer engagement. Ownership of the sequencing‑to‑vaccine workflow (tumor profiling, neoantigen calling, GMP mRNA production, LNP formulation, and rapid release testing) will be a durable advantage.

mRNA Cancer Vaccines and Therapeutics Market

Market dynamics and operational realities

Four operational realities will shape winners in 2026:

- Decentralized GMP manufacturing: Hospital‑based and academic GMP facilities are already proving they can produce personalized mRNA vaccines and shorten time‑to‑patient. Companies must decide whether to build in‑house hospital partnerships or outsource to regional GMP operators.

- Lipid nanoparticle (LNP) supply and formulation know‑how: LNP capacity and formulation IP remain bottlenecks. Early supplier agreements and formulation transfer plans are non‑negotiable components of launch readiness.

- Regulatory and reimbursement timing: Regulatory filings for first mRNA cancer vaccines are expected around the 2026–2027 window. Payer frameworks will follow quickly for high‑impact adjuvant and metastatic indications; value dossiers and RWE frameworks must be pre‑built.

- Clinical evidence design: Adaptive and hybrid trial designs that incorporate biomarker‑guided cohorts, platform arms and pragmatic endpoints will both de‑risk development and generate the real‑world effectiveness signals payers require.

Scenarios and recommended plays for corporate leaders

We model three pragmatic 2026 scenarios and outline the corresponding strategic responses:

- Accelerated Approval + Positive Long‑Term Data — If pivotal readouts produce strong efficacy signals, prioritize: scaled manufacturing (hybrid centralized + hospital nodes), rapid commercial launch in high‑unmet‑need indications, and outcomes‑based contracts with early adopter centers.

- Mixed Clinical Signals / Heterogeneous Efficacy — Focus resources on indication triage and biomarker refinement. Deprioritize broad commercialization in favor of targeted specialty launches and partnerships to share development risk.

- Regulatory Delay or Reimbursement Pushback — Preserve optionality via platform licensing, consider bolt‑on acquisitions to secure delivery/diagnostics capabilities, and accelerate RWE generation through investigator‑initiated studies and compassionate use programs.

Across all scenarios, six immediate actions improve optionality in 2026:

- Lock LNP and critical reagent supply agreements with staged volume commitments.

- Establish hospital GMP partnerships and pilot runs for personalized workflows.

- Pre‑negotiate reimbursement pilots in high‑value cancer centers and with progressive payers.

- Invest in modular quality systems and digital traceability for rapid batch release.

- Build an RWE plan to collect early effectiveness, safety and health economic outcomes.

- Define M&A thresholds and integration checklists focused on sequencing, delivery and manufacturing capabilities.

How this PW Consulting study adds strategic value for 2026

Boards, corporate development teams and commercial leaders need more than headline growth rates; they need a mapped pathway from R&D signals to payer acceptance and clinic adoption. Our study provides that pathway. Specifically, the report delivers:

- Decision‑grade scenario models that translate clinical probabilities into revenue timing and capital needs across multiple launch timelines.

- Operational checklists and partner scorecards that reduce time‑to‑patient and mitigate single‑supplier risk.

- Negotiation playbooks for early payer pilots and HTA submission sequencing, de‑risking first‑wave commercialization.

- An M&A/partnership heatmap aligned to clinical evidence windows — enabling disciplined capital deployment when valuations and timing converge.

Closing: what to act on now

2026 is a compact window where clinical readouts, regulatory actions and manufacturing scale decisions collide. Executives should (1) finalize supply and manufacturing partnerships, (2) establish payer engagement pilots keyed to expected efficacy outcomes, and (3) prioritize platform integrations that secure sequencing‑to‑vaccine control. The market is growing steadily — a roughly 7% CAGR through 2032 — but early movers who align evidence generation, manufacturing execution and commercial contracting will capture disproportionate strategic upside.

For detailed datasets, scenario models, segmentation by indication and region, and the full set of operational playbooks and M&A targets referenced in this preview, please consult the complete PW Consulting mRNA Cancer Vaccines and Therapeutics Market report available on our website.

For detailed analysis of this topic, please visit the official page:mRNA Cancer Vaccines and Therapeutics Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com