Rack & Pinion Pneumatic Actuators: Strategic Intelligence Briefing for 2026 Decision-Makers

Executive snapshot

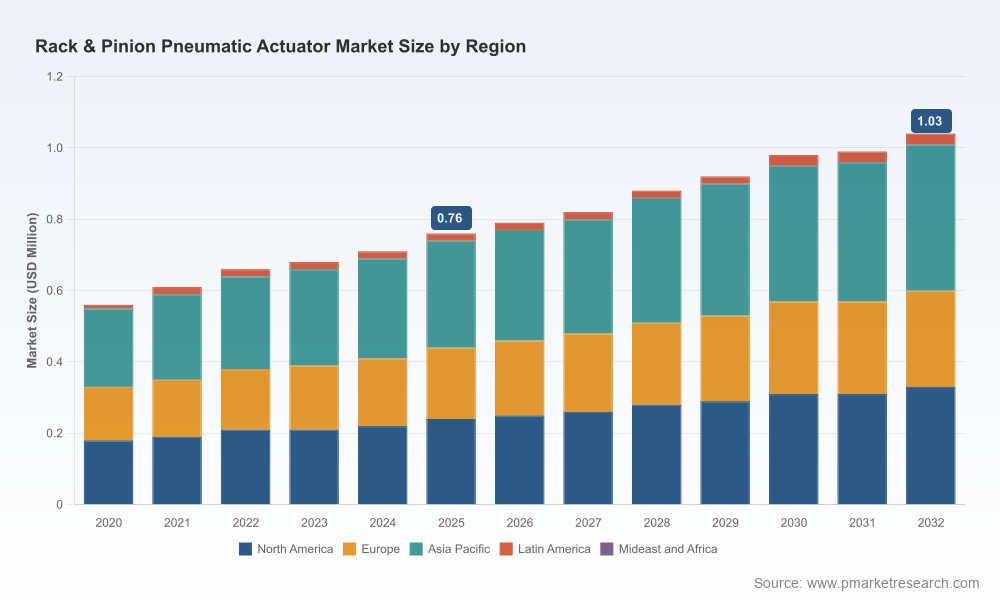

As industrial automation accelerates and process industries re-price reliability, energy, and uptime, rack & pinion pneumatic actuators are reasserting their strategic role in quarter‑turn valve automation. PW Consulting’s latest market study — benchmarked to base year 2025 and projecting through 2032 — quantifies a steady, resilient expansion of the segment. The installed-and-serviceable market expanded from roughly 0.57 (USD Million) in 2020 to about 0.76 (USD Million) in 2025, and our forecast shows growth to approximately 1.03 (USD Million) by 2032 under a blended CAGR of 4.47% for the forecast period.

Rack & Pinion Pneumatic Actuator Market

This briefing synthesizes the aspects of the report that senior executives, product leaders, and corporate strategists must internalize in 2026. It is written to demonstrate the analytical depth behind our conclusions while intentionally withholding detailed sub‑segment breakdowns — the tactical granularity that drives competitive action is available in the full report.

Rack & Pinion Pneumatic Actuator Market

Why this study matters for 2026 decision-making

- Investment clarity: The market’s steady mid‑single‑digit CAGR signals an environment suitable for selective capacity expansion, targeted R&D, and aftermarket services plays — not a free‑for‑all. Capital allocation decisions must be grounded in nuanced torque‑class and application-level dynamics that the full study models.

- Product‑market fit under new constraints: Stricter environmental regulations and sustainability mandates are changing procurement specifications. Buyers increasingly value energy‑efficient, low‑leakage pneumatic solutions and lifecycle emissions reporting. The study translates these regulatory pressures into product feature priorities and procurement criteria.

- Operational risk management: Compressed air infrastructure is a non‑trivial constraint in many brownfield and retrofit projects. Our scenario analysis shows where infrastructure upgrades become gating factors for actuator selection versus systems that prioritize lower energy intensity or hybrid actuation strategies.

- M&A and partnership targeting: With a moderate market concentration (CR3 ~39%), the landscape offers bolt‑on opportunities for niche specialists and selective consolidation for global platform builders. The report’s company benchmarking and valuation proxies identify attractive adjacencies and integration risks.

Market trajectory and what the numbers mean

The segment’s historical path and forecast reflect a pragmatic balance between mature use‑cases (process, oil & gas, chemical processing) and nascent demand drivers (smart retrofit, life‑cycle services). The market increased from 2020 to 2025 and continues on a steady trajectory to 2032, consistent with broader automation spending and replacement cycles in capital‑intensive industries.

Rack & Pinion Pneumatic Actuator Market

Key takeaways from the aggregated market model:

- Growth is driven by replacement and upgrade cycles, not purely new‑build volume — meaning aftermarket and retrofit service models capture a disproportionate share of near‑term value.

- Digital integration (smart positioners, sensorized actuators, predictive diagnostics) is a principal premium feature that accelerates purchasing decisions where downtime costs are high.

- Operating environments matter: actuators optimized for corrosive, high‑cycle, or extreme‑temperature contexts command better margin and longer procurement cycles, creating differentiated routes to market for specialty suppliers.

Competitive landscape: players to watch

The market blends established industrial platform players with regional specialists. Our competitive analysis profiles manufacturers across geographies and product philosophies — from heavy‑duty forged components to compact, high‑cycle designs and intelligent positioner integrators.

- Platform incumbents: Global OEMs provide broad portfolios that combine actuators with integrated valve automation systems, aftermarket networks, and global supply chains. Their strengths are scale, service coverage, and established channel relationships; their strategic challenge is maintaining differentiation in a segment where functional parity can be achieved by smaller, agile players.

- Engineering specialists: Several firms prioritize torque density, corrosion resistance, or cycle life, enabling premium positioning in oil & gas, chemical, and harsh‑service applications. These companies are the logical targets for OEMs seeking to accelerate product roadmaps or enter high‑margin niches via acquisition or distribution partnerships.

- Controls and intelligence providers: Companies producing intelligent valve positioners and diagnostics modules are changing the value equation. Recent product launches underscore the competitive shift toward contactless feedback, pressure diagnostics, and integrated telemetry — features that extract more lifecycle value than raw hardware alone.

Notable corporate developments in late‑2025 reinforce these dynamics. Leading positioner manufacturers announced new intelligent units with contactless feedback and advanced diagnostics; major automation catalog updates highlight integration and sustainability tools for pneumatic valves. These moves confirm that digital and material innovations are converging to redefine differentiation.

Strategic playbook for 2026: tactical actions that matter

Based on the study’s cross‑cutting scenarios and company benchmarks, we advise executive teams to prioritize the following actions in 2026:

- Prioritize retrofit aftermarket offerings. Build modular upgrade kits (positioner + sensors + seals) and bundled service agreements; these capture high margin share as operators defer full system replacements.

- Invest selectively in digital capabilities. Integrate contactless position feedback, on‑board diagnostics, and secure telemetry into key product lines. Provide plug‑and‑play interoperability with dominant control ecosystems to lower buyer switching costs.

- Differentiate by environment. Offer qualified product families for corrosive, high‑cycle, and hygienic installations. Supplement with validated installation packages to reduce field integration uncertainty for buyers.

- Reconfigure supply and risk: map your critical raw‑material and machining bottlenecks, and use multi‑sourcing or regional distribution centers to improve lead times without inflating inventory. Compressed air infrastructure constraints should be assessed as part of pre‑sales engineering to avoid specification mismatches.

- Use M&A to fill capability gaps. Targets that bring specialty metallurgy, premium sealing systems, or compact high‑torque designs accelerate go‑to‑market at lower organic R&D cycles. The market concentration profile suggests room for value‑creating consolidation — but diligence must prioritize integration of aftersales networks and digital backends.

Report contents — practical tools inside the full study

The complete PW Consulting market study is designed as an executable playbook, not a descriptive survey. Highlights include:

- A transparent, auditable market model (2020–2025 historical; 2026–2032 forecast) with sensitivity levers for macro scenarios (energy price shocks, regulatory tightening, automation capex cycles).

- A buyer‑level decision matrix that translates technical specifications (torque, cycle life, ingress protection, materials) into total cost of ownership and mean time between failures by typical application classes.

- Competitive benchmarking and product feature mapping across the leading manufacturers, with technical performance proxies and go‑to‑market assessments.

- Supply‑chain and procurement playbooks: lead‑time risk matrices, single‑sourcing stress tests, and recommended contract clauses for uptime guarantees and spare‑parts logistics.

- M&A and partnership screening tools: valuation multiples by revenue bucket, integration checklists, and a prioritized target universe for strategic and financial buyers.

- Implementation resources: sample retrofit kits, diagnostic spec templates for buyers, and an onboarding checklist for aftersales teams moving into predictive maintenance services.

To preserve the tactical edge for clients, detailed sub‑segment tables (regional & application splits, torque‑class revenue breakdowns, customer price elasticities) are intentionally summarized in this briefing — they are included in full within the report package and underpin all our recommendations.

Risk map and regulatory context

Critical external variables that materially affect outcomes include environmental regulation, energy pricing, and digital security standards. Our dynamics analysis highlights that tighter emissions and energy‑efficiency standards are nudging buyers towards actuators and control packages that provide verifiable reduced energy consumption and leak‑minimizing operation. Additionally, the shift to predictive maintenance elevates cybersecurity and data‑integrity as procurement criteria for intelligent actuator deployments.

Operationally, compressed air infrastructure remains a gating constraint in many retrofit contexts. Projects that fail to account for required air flow and pressure reserves encounter rework and warranty disputes; the report includes an infrastructure assessment framework that links pneumatic system capacity to viable actuator choices.

How to use this intelligence in 90 days

- Week 1–4: Run the report’s buyer decision matrix against your top 20 accounts to identify retrofit opportunities and immediate cross‑sell candidates.

- Week 5–8: Use the competitive benchmark to reprice service packages and to define a one‑page RFP package for high‑value prospects including diagnostics and uptime SLAs.

- Week 9–12: Execute a shortlist of tactical partnerships or acquisitions identified by the M&A screen; deploy pilot digital retrofit in a prioritized plant and measure lifecycle metrics against our TCO model.

Next steps

PW Consulting’s Rack & Pinion Pneumatic Actuator Market study blends rigorous, auditable market sizing with actionable tools for commercial, product, and corporate strategy teams. The summary here demonstrates the strategic lens and the types of operational prescriptions available; however, the granular segmentation and the executable datasets that underpin procurement decisions, M&A diligence, and product roadmaps are contained only in the full report.

Clients planning capital allocation, product launches, or M&A activity in 2026 should consult the full study to access the detailed sub‑segment economics, regional and application level demand drivers, and the downloadable models that power our recommendations.

For detailed analysis of this topic, please visit the official page:Rack & Pinion Pneumatic Actuator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com