How Alkylate Gasoline Market Demand Surges

Other |

2026-05-15 10:14:57

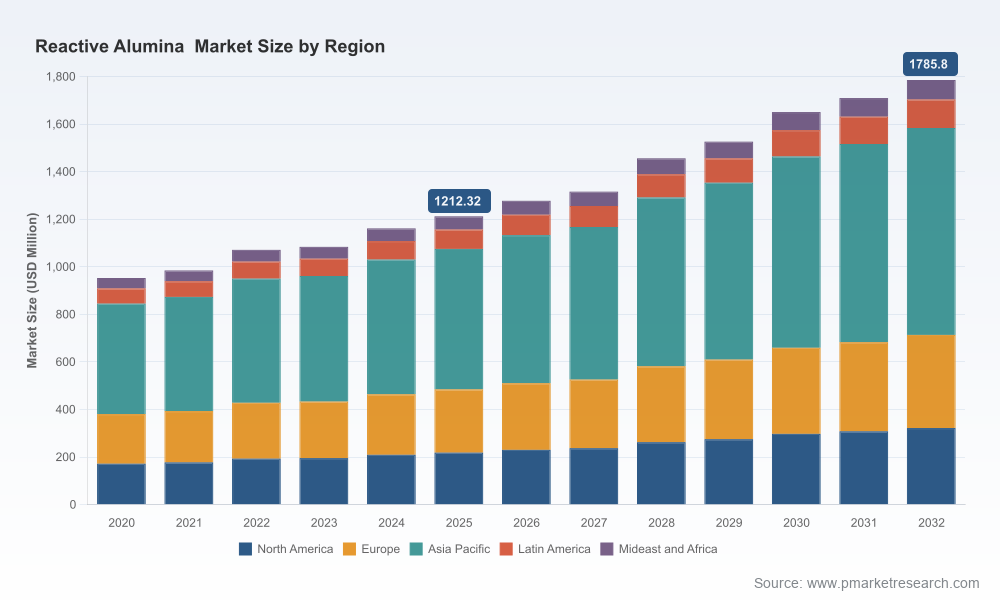

Reactive alumina occupies a compact but strategically important niche in the materials value chain — bridging raw aluminum derivatives and high-value downstream applications such as refractories, catalysts, desiccants and specialty ceramics. For executive teams planning resource allocation, capacity moves, or M&A in 2026, the market is large enough to matter and dynamic enough to reward focused, evidence-based strategies. Our PW Consulting market study uses a 2025 base year and projects through 2032. The global reactive alumina market in 2025 totaled roughly USD 1.21 billion and is forecast to grow at a compound annual growth rate (CAGR) of approximately 5.56% across the 2026–2032 window — reaching about USD 1.79 billion by 2032. These topline dynamics create distinct windows of opportunity and risk that we unpack below.

Reactive Alumina Market

Historical momentum: Between 2020 and 2025 the market expanded materially from under USD 1.0 billion to the 2025 base level, reflecting recovering industrial activity, targeted product innovation and steady demand for refractory and catalyst-grade products.

Reactive Alumina Market

Near-term acceleration: Our 2026–2032 forecast assumes mid-single-digit annual expansion driven by a combination of sustained demand in high-temperature industrial processes, incremental adoption in specialty desiccant and fluoride remediation niches, and modest recovery/reshoring activity in primary and secondary aluminum supply chains.

Reactive Alumina Market

Competitive structure: The market remains fragmented relative to many chemical commodity markets; industry concentration is low–moderate among the top suppliers, leaving room for regional specialists and differentiated product players to capture share through technical differentiation and customer intimacy.

Application-driven differentiation: Reactive alumina is not a monolith — it is specified by morphology (e.g., powdered vs. sphered), surface chemistry and particle-size distribution tailored to applications such as catalyst supports, refractory additions, desiccants and niche water-treatment media. Buyers are increasingly valuing consistent performance attributes (surface area, reactivity, rheology) over lowest-cost sourcing, which favours suppliers that can guarantee narrow specification bands and tight logistics.

Industrial trends: Investment cycles in primary industries that consume reactive alumina (steel, cement, petrochemicals, alumina-based ceramics) will drive demand heterogeneously. For example, refractory demand follows furnace rebuild and capacity expansion cycles, while catalyst demand is tied to refinery and chemical process upgrades — timing matters more than headline growth.

Regulatory and sustainability pressures: The increasing availability of recycled aluminum capacity and the ramp-up of secondary smelting/recycling facilities (as documented in recent mineral commodity summaries) will change feedstock economics and potentially affect quality expectations for downstream alumina-derived intermediates. Separately, environmental rules governing emissions from refractories and catalysts influence material selection and lifecycle cost calculations.

Capacity adjustments and resilience: The past 18–24 months have shown that capacity restarts, staged expansions and select refinery closures materially shift regional trade flows and spot availability. These moves illuminate two strategic imperatives for 2026: maintain flexible sourcing options and stress-test procurement under scenarios that include partial restarts and localized shutdowns.

Product innovation as defence: New grades optimized for viscosity control in castables, mono- and multi-modal particle distributions for mechanical performance, and sphered high-purity morphologies for catalyst beads are examples of differentiation that raise switching costs. Companies that accelerate application-led R&D can command premium pricing and create distribution advantages.

Logistics and service layers: Given the material’s technical sensitivity, service offerings — from packaging and moisture control to technical support at the refractories/formulation stage — are increasingly decisive. Suppliers who bundle analytics, specification guarantees and local technical service can outcompete on total landed cost rather than price per kilogram alone.

Fragmentation with pockets of specialization: The top firms include established global purveyors of specialty aluminas and a set of regional specialists. Several players have clear technical niches — for example, providers that focus on high-purity sphered products for catalyst applications, others with broad particle-size portfolios for refractory uses, and some that emphasize viscosity- or rheology-optimized grades for castables.

Representative strategic profiles:

Recent moves to watch: Select launches of viscosity-optimized grades and notable capacity restarts/adjustments in upstream alumina production have implications for supply availability and technical expectations. These developments underscore the need to monitor both product innovation and upstream capacity changes as simultaneous drivers of competitive positioning.

Proprietary demand model and scenario suite: A calibrated market model covering 2020–2025 historicals and 2026–2032 forecasts, including three demand scenarios (baseline, upside, downside) that stress-test industrial capex cycles and recycling penetration.

Supply-mapping and risk heatmaps: Plant-level coverage for key producers, capacity utilization scenarios, and a matrix of geopolitical, operational and raw-material risks that affect short-term availability and long-term contract negotiations.

Segment-sensitive pricing and margin frameworks: Price and margin drivers by product morphology and application class, plus sensitivity analyses for key input costs and freight scenarios to support sourcing decisions and contract negotiation playbooks.

Commercial playbooks and M&A screening: Go-to-market strategies for leaders and challengers, inorganic entry/scale options with quick screening criteria, and integration checklists that reduce execution risk post-acquisition.

Technical appendix: Specification crosswalks, typical formulation impacts by grade, and a library of customer use-cases that help product managers and sales teams accelerate customer qualification cycles.

Procurement: Move from single-year spot-buying to hybrid contracts that combine flexibility (for fluctuating refractory/catalyst demand) with guaranteed minimum volumes for priority grades. Incorporate quality-linked service credits and on-site technical support as part of TCO conversations.

Product strategy: Prioritize investments in grades that demonstrably solve customer pain — lower water demand in castables, consistent bead morphology for catalysts, and robust performance in desiccant or fluoride-removal roles. Small, targeted application trials can unlock outsized premium pricing.

M&A and alliances: Focus on bolt-on assets that fill a capability gap (e.g., sphering capacity or narrow particle-size control) or extend reach geographically in low-cost logistics corridors. Partnerships with recyclers and secondary smelters can secure feedstock optionality as recycled aluminum capacity grows.

Risk management: Build scenario playbooks for partial upstream curtailments, new recycling capacity coming online, and regulatory tightening in key markets. Maintain contingency logistics routes and diversify contract tenors to mitigate single-source risk.

This introduction is designed to give senior teams the strategic context required to prioritize actions in 2026. The full PW Consulting Reactive Alumina Market report contains the detailed models, plant and grade-level intelligence, supplier scorecards, and a downloadable set of commercial negotiation templates that underpin the strategic recommendations summarized here. We intentionally withhold detailed sub-segmentation figures and plant-level financials in this preview to preserve the signal value of the full dataset available on our platform.

Reactive alumina is a specialized, technically differentiated market with a clear, financeable growth path across the next investment cycle. The market’s mid-single-digit CAGR and the current industry structure reward targeted technical differentiation, resilient sourcing strategies and disciplined commercial execution. For leaders making strategic capital, procurement or M&A decisions in 2026, the correct choice is rarely “more of the same.” Instead, success will come to organizations that pair technical product leadership with scenario-ready sourcing and a tight go-to-market discipline. To convert this strategic view into executable actions, access to grade-level, plant-level and contract-level intelligence is required — the full PW Consulting report provides that operational depth.

Request a briefing with PW Consulting’s industry team to walk through scenario outputs and supplier scorecards.

Commission a focused due-diligence module if you’re considering acquisition or capacity investments in 2026.

Subscribe to the full report to unlock the models, technical appendices and commercial playbooks referenced above.

For detailed analysis of this topic, please visit the official page:Reactive Alumina Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com