Railway Grease Market — Strategic Imperatives for 2026 Decision-Makers

As PW Consulting’s senior strategy team and chief industry analysis office, we present this executive preview of our full Railway Grease Market study. This briefing is designed to establish the strategic context and operational priorities that will matter most for executives, procurement leaders, product managers, and infrastructure operators in 2026. We intentionally surface high-value, actionable insights while preserving the detailed subsegment tables, supplier scorecards, and scenario models for the full report — the granular intelligence that underpins tactical decisions.

Railway Grease Market

High‑level market trajectory: what the numbers say (and what they imply)

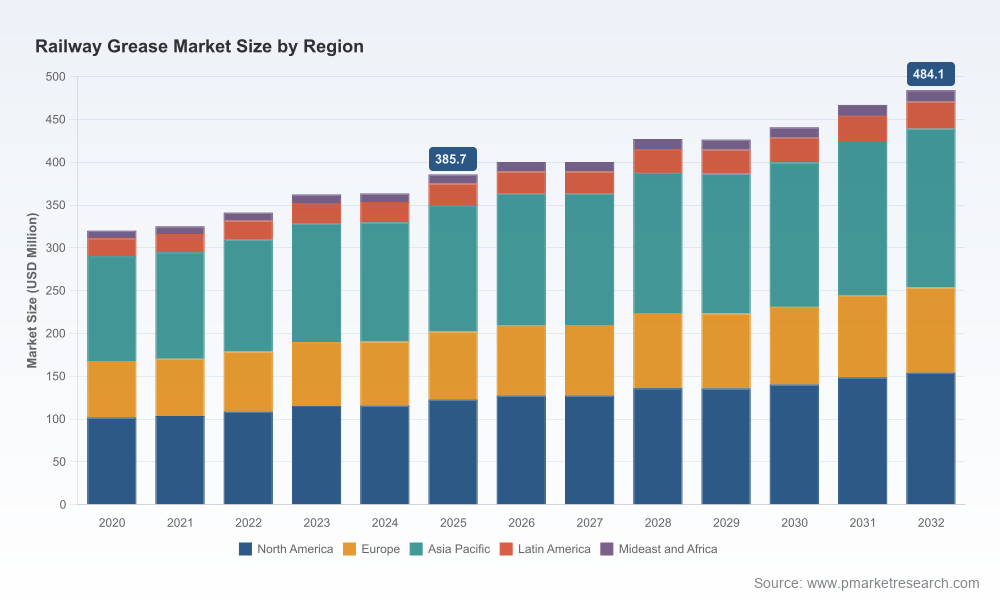

Between 2020 and 2025 the global railway grease market demonstrated steady, low‑to‑mid single‑digit expansion reflecting resilient demand from maintenance, new rolling‑stock manufacturing, and increasing attention to lifecycle costs. In monetary terms the market moved from a solid baseline in 2020 through to a base year value in 2025 (reported in USD Million), and our forecast projects a continued upward path through 2032. Over the forecast horizon from 2026 to 2032 the market is expected to grow at a compound annual growth rate (CAGR) of 3.3%.

Railway Grease Market

What this trajectory means for 2026 strategic planning: growth is steady but not explosive. That profile favors investments which drive margin expansion, operational efficiency, and product differentiation rather than purely volume-driven capacity plays. Buyers and suppliers who can convert modest top‑line growth into sustained margin uplift through formulation innovation, service augmentation, and supply chain optimization will capture disproportionate value.

Railway Grease Market

Strategic implications for executives — a 2026 checklist

- Prioritize product differentiation over price‑only competition. With moderate market expansion, competency in environmental compliance, noise and wear reduction, and long‑interval service greases creates defensible premium positions.

- Embed sustainability as a functional requirement. Biodegradable and ecolabelled formulations are moving from “nice to have” to procurement filters for urban transit contracts and sensitive environments. Expect environmental compliance to be a gating factor in tenders and a lever in public‑private contracts.

- Lock in supply chain resilience for critical inputs. Raw material volatility (thickeners, specialty additives and graphite) can erode margins quickly when demand is stable. Dual‑sourcing strategies, buffer inventories and supplier collaboration agreements reduce disruption risk without large fixed investments.

- Convert product performance into service revenue. Grease selection, application interval optimization, and condition‑based relubrication programs present high ROI opportunities for grease suppliers and maintenance contractors.

- Refine procurement scorecards beyond unit price. Total cost of ownership (TCO), environmental certifications, field application support, and logistics reliability should carry material weight in tender evaluations.

- Prepare for regulatory tightening and local content requirements. Operators and suppliers must model regulatory scenarios (eco‑labelling, biodegradability mandates) into product roadmaps and manufacturing footprints to avoid contract exclusions.

What the full report gives you — practical, transaction‑ready deliverables

Our full Railway Grease Market study is constructed as an operational playbook for 2026 decision cycles. It is organized to move organizations from strategy to execution quickly:

- Robust methodology and demand model. Transparent historicization (2020–2025) and a scenario‑based forecast (2026–2032) that lets you run alternate macro assumptions against demand and price trajectories.

- Supply chain and cost build‑ups. Bill‑of‑materials and manufacturing cost models for common grease families, highlighting the sensitivity of margins to feedstock and additive price swings.

- Buyer’s toolkit. Ready‑to‑use procurement templates: tender scoring matrices, specimen contract clauses (warranties, service levels, environmental KPIs), and negotiation playbooks prioritized by deal size and region type.

- Technical decision support. Application mapping (rolling stock elements, trackside components, switches), recommended architectures for formulation selection and relubrication intervals, and a specification checklist to harmonize engineering and procurement language.

- Competitive benchmarking and supplier scorecards. Confidential quantitative assessments and qualitative SWOTs for leading suppliers; procurement leaders can plug these into sourcing decisions immediately.

- Case studies and implementation roadmaps. Operational pilots that reduced lifecycle wear, cut maintenance windows, or lowered environmental discharge risks — with stepwise guidance to replicate outcomes at scale.

- Regulatory and sustainability matrix. Cross‑jurisdictional mapping of environmental standards, biodegradability tests, and labeling rules that affect product acceptance in major markets.

Competitive landscape: how vendors are positioning (high‑level)

The market is moderately concentrated: the top three suppliers account for a meaningful share of market revenues, and the top five widen that concentration further. This concentration dynamic makes competitive differentiation a blend of formulation excellence and after‑sales service.

- RS Clare (United Kingdom) — Ecolabel and metro‑focused solutions. The supplier emphasizes ecolabel‑accredited curved‑rail greases, bio‑formulations for metro networks, and high‑mobility greases targeting noise and vibration mitigation at the trackside.

- Whitmore / The Whitmore Group (United States) — Rail‑specific lithium complex grades with graphite and bio‑based options. Offers railmaster families of greases engineered for points, wheels, flanges and trackside components with an emphasis on rail operator usability and safety.

- Royal Manufacturing (United States) — Curve‑rail specialists and certified production. Focused on curve‑rail formulations designed to reduce friction and wheel wear, produced under ISO‑compliant processes.

- Klüber Lubrication (Germany) — Engineering‑led performance formulations. Recognized for high‑performance industrial lubricants adapted for track and rail systems, with strong technical support and OEM relationships.

- Q8Oils (Denmark) — Biodegradable switch‑track fluids. Marketed biodegradable NLGI fluid‑grade greases for switches and sensitive trackside locations, suited to environmentally constrained applications.

- Midlands Lubricants Ltd (United Kingdom) — Blended rail greases with biodegradable and high‑performance options tailored for points, wheels and trackside lubrication.

Implications: suppliers that couple validated performance (field trials, ISO processes) with sustainability credentials and on‑site support gain preferential access to urban transit contracts and major infrastructure maintenance frameworks. For buyers, the vendor landscape means source diversification is feasible without sacrificing technical coherence.

Risks, uncertainties and where to stress‑test plans

- Feedstock volatility. Shifts in commodity inputs and specialty additives can compress supplier margins or force reformulation; stress‑test supplier commitments and cost‑pass clauses for contracts beyond twelve months.

- Regulatory shifts. Faster adoption of biodegradability standards or local environmental mandates can change approved product lists rapidly; scenario‑based regulatory modeling is table stakes for product roadmaps.

- Technological substitution. Advances in solid lubrication, additive metallurgy, or sensor‑based condition monitoring could change relubrication cadences; invest selectively in pilots to understand TCO impacts.

- Consolidation dynamics. Moderate market concentration suggests M&A activity could accelerate; buyers should anticipate integration‑related supplier continuity risks and pricing resets in the event of consolidation.

How to use our findings in 90‑, 180‑ and 360‑day plans

- 90 days. Align procurement scorecards with TCO and environmental criteria; initiate bilateral supplier audits for continuity and compliance; select 1–2 candidate greases for field evaluation.

- 180 days. Run operational pilots on targeted asset classes, finalize procurement contracts with performance and sustainability KPIs, and implement a supplier performance dashboard.

- 360 days. Scale successful pilots, renegotiate portfolio pricing on volume and lifecycle guarantees, and update asset maintenance schedules to reflect condition‑based lubrication insights.

Next steps — where to find the granular intelligence

This executive preview outlines the decision levers and operational playbooks that will matter most in 2026. For the granular datasets — including detailed regional and application splits, full supplier scorecards, price‑by‑type curves, and downloadable procurement templates — consult the full PW Consulting Railway Grease Market report. The complete study contains the segment‑level figures, comparator matrices and downloadable tools required to execute sourcing, product, and MRO strategies with precision.

PW Consulting is prepared to run customized workshops to translate the report’s insights into a tailored action plan for your organization — from tender design through to pilot deployment and supplier integration. For organizations preparing capital and operating plans in 2026, early access to the full dataset and scenario analyses will materially improve negotiation outcomes and reduce execution risk.

For detailed analysis of this topic, please visit the official page:Railway Grease Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com