Damper Actuators Market — Strategic Preview for 2026 Decision-Makers

As PW Consulting’s lead strategist and senior industry analyst, I present a concise, actionable preview of our latest Damper Actuators Market research — a targeted briefing designed to inform board-level planning and operational decisions in 2026. This “trailer” distills the study’s strategic implications, demonstrates the analytics that underpin our conclusions, and deliberately withholds certain granular splits to encourage access to the full report for procurement teams, product groups, and corporate development practitioners seeking transaction-level intelligence.

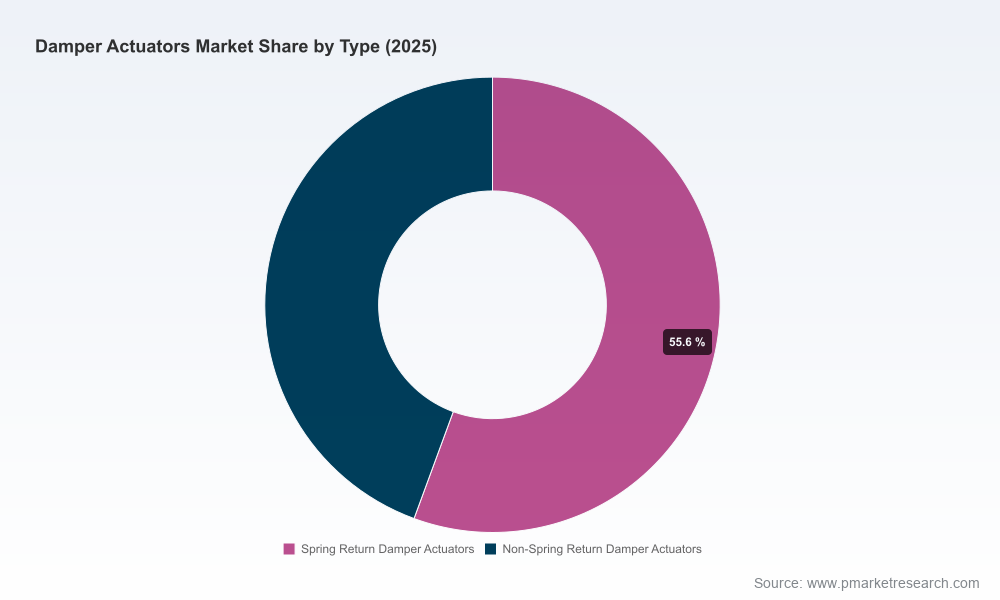

Damper Actuators Market

Why this market matters in 2026

Damper actuators sit at the intersection of building automation, energy efficiency mandates, and industrial process control. Over the 2020–2025 historical period the market demonstrated steady expansion; our base-year assessment for 2025 places the industry at USD 215.0 Million. Under current technology adoption and regulatory assumptions, we project the market to grow at a compound annual growth rate (CAGR) of 5.8% over the 2026–2032 forecast horizon, reaching approximately USD 315.02 Million by 2032. These headline dynamics create a multi-faceted opportunity set for manufacturers, systems integrators, and institutional buyers in 2026:

Damper Actuators Market

- Predictable growth that supports capacity investments and selective consolidation.

- Regulatory and standards-driven demand that privileges compliant, certified solutions.

- Emerging product differentiation driven by digital connectivity, safety certifications, and energy optimization capabilities.

What the report delivers — practical, decision-ready modules

The PW Consulting report is structured for executives to translate insight into action. Key operational modules include:

Damper Actuators Market

- Market sizing and trend analysis: historical time-series (2020–2025), base-year benchmarking (2025), and a granular forecast (2026–2032) by technology, application class, and region — with scenario modeling to stress-test demand under different regulatory and energy-price pathways.

- Commercial playbooks: channel strategies, procurement checklists, and lifecycle cost models for new-build vs retrofit programs, enabling procurement and product teams to weigh CapEx/OpEx trade-offs in a 5-year procurement window.

- Technology and product roadmaps: comparative assessment of spring-return and non-spring designs, digital integration (BACnet, Ethernet/IP), fail-safe mechanisms, and fire/smoke-rated solutions — with implications for product development roadmaps and qualification timelines.

- Competitive due diligence templates: valuation-adjusted comparables and synergy frameworks for M&A, joint ventures, or distribution partnerships focused on building controls and industrial ventilation segments.

- Regulatory and compliance matrix: mapping of UL, NFPA, IEC/EN and regional EMC/CE obligations to product development and testing timelines, plus recommended certification priorities for market entry acceleration.

Each module is accompanied by executable recommendations — e.g., the procurement playbook outlines contracting clauses and warranty terms aligned to lifecycle risk profiles; the M&A template lists immediate cost and revenue synergies to prioritize in diligence.

Competitive landscape: what leaders are doing

The damper actuator market is moderately consolidated (CR3 ≈ 65%; CR5 ≈ 75%), indicating meaningful incumbent scale advantages but also room for focused challengers with differentiated propositions. Our competitive review covers product portfolios, go-to-market approaches, and near-term strategic moves from the following core players:

- Belimo Holding AG (Hinwil, Switzerland): A technology leader in electric actuators with an emphasis on fire and smoke control series. Their strong emphasis on UL-listed products and protocol integrations (e.g., BACnet) has positioned them as a preferred supplier for specification-driven commercial projects. Recent corporate communications indicate ongoing innovation and robust aftermarket engagement.

- Schneider Electric SE (Rueil-Malmaison, France): Markets SmartX actuator platforms that emphasize energy efficiency and systems interoperability. Their strength lies in systems-level offerings and channel depth across large commercial integrators.

- Siemens AG (Munich, Germany): Offers OpenAir and spring-return actuators that are deeply entrenched in both HVAC and life-safety segments. Siemens’ advantage is cross-selling through broader building automation suites and long-term service contracts.

- Rotork plc (Bath, UK): Known for industrial-grade actuators with advanced positioning and Ethernet integration, Rotork competes where process reliability and networked position feedback are critical.

- Harold Beck & Sons, Johnson Controls, Honeywell, Dwyer Instruments, Hansen Corporation, Kele Inc., Neptronic, Oden Control: These firms collectively comprise the mid-tier and niche specialists, each with pockets of strength (precision modulation, building automation integration, solar and residential actuation, industrial process control).

Recent filings and announcements indicate incumbents are pursuing incremental product upgrades, certification expansions, and selective platform rationalization. Notably, several manufacturers have publicly emphasized lifecycle testing and compliance to life-safety standards, which has become an increasingly decisive procurement criterion for institutional buyers.

Regulatory and standards dynamics — drivers of procurement and design

Compliance and certification are central to buyer decisions in 2026. Key regulatory signals we stress in the report include:

- Life-safety testing expectations: several leading actuators exceed UL cycle endurance test requirements and align with UL 555/555S performance protocols for fire and smoke dampers — a procurement differentiator for critical infrastructure projects.

- Code alignment: products meeting NFPA-referenced testing (NFPA 80 / NFPA 105) are increasingly specified in building codes and by inspectors, accelerating adoption in commercial and public utility projects.

- Electromagnetic compatibility and manufacturing quality: recent market entries achieving CE/EN IEC harmonization signal an elevated bar for international OEMs and exporters, while ISO 9001 production processes remain table stakes for institutional procurement.

For buyers and product teams, the implication is clear: certification timelines must be integrated into go-to-market plans, and vendors without validated test pedigrees will see elongated qualification cycles.

Strategic implications for 2026 planning

From a corporate strategy perspective, our analysis leads to a concise set of priorities for 2026:

- Prioritize certified life-safety and protocol-integrated products for commercial and public-infrastructure bids. Certification and interoperability reduce time-to-spec and lower operational integration risk.

- Invest selectively in digital enablement. Actuators that provide reliable position feedback and networked diagnostics meaningfully reduce maintenance costs and enable service-led revenue models.

- Adopt a hybrid approach to growth: incumbents should pursue bolt-on acquisitions and distribution partnerships to close capability gaps, while challengers should target niche verticals (process industries, specialized ventilation) where premium margins and specification lock-in exist.

- Embed supply-chain resilience into procurement strategies. Given steady market growth and concentrated manufacturing, dual-sourcing high-risk components and securing long-lead items will reduce exposure to cyclical shocks.

- Recalibrate pricing models to reflect lifecycle value. Total cost of ownership (installation, commissioning, maintenance, certification) is becoming a competitive battleground; vendors that can quantify and market TCO advantages will win specification processes.

What we hold back here — and why you should read the full report

This preview is intentionally strategic rather than transactional. To protect the actionable value of our research and to direct practitioners toward the full intelligence package, we withhold granular regional and application splits, in-depth price benchmarking, vendor-level shipment volumes, and deal-level comparables. The full PW Consulting report provides:

- Disaggregated forecasts by region, application, and technology, with sensitivity analysis to energy and code-change scenarios.

- Vendor scorecards that quantify product, channel, and service strengths against procurement criteria used by large developers and utilities.

- Transaction playbooks for M&A and strategic partnerships, including modeled synergies, integration roadmaps, and negotiation frameworks.

- Operational checklists and test plans for R&D and quality teams to accelerate certification and product-market fit.

These items are essential for teams executing on product roadmaps, sourcing decisions, or M&A workstreams in 2026. The trailer purposefully demonstrates methodological rigor while reserving the tactical blueprints for subscribers and clients.

Next steps for executives

If you are making 2026 capital allocation, product development, or M&A decisions in the damper actuator space, we recommend the following immediate actions:

- Request the full report and the accompanying due-diligence annex to validate your project timelines against certification and supply-chain lead times.

- Initiate vendor gap-analysis workshops focused on certification, digital integration, and aftermarket service capabilities.

- Prioritize a short-list of strategic partnerships or acquisition targets based on capability overlap and immediate revenue synergies; use the report’s commercial playbooks to structure term sheets and post-merger integration plans.

PW Consulting’s full Damper Actuators Market research translates the high-level growth narrative — from USD 215.0 Million in 2025, expanding at a 5.8% CAGR to a projected USD 315.02 Million by 2032 — into executable strategies and procurement-ready intelligence. For access to the complete dataset, vendor-level analyses, and implementation templates, visit our report page or contact our industry team to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Damper Actuators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com