Autocrane Market 2026: Strategic Signals for Decision-Makers — A PW Consulting Preview

As companies set budgets, product roadmaps, and M&A watchlists for 2026, autocrane stakeholders face a familiar strategic tension: accelerate technology and service investments now, or preserve capital while waiting for clearer demand signals. PW Consulting’s latest Autocrane Market study — built on a 2025 base year and a 2026–2032 forecast horizon — distills the market dynamics that should shape those choices. This preview outlines the study’s high‑value takeaways for executives and investment committees, while intentionally preserving the report’s proprietary, segment‑level detail to invite a deeper look at the full deliverable.

Autocrane Market

Why 2026 Is a Pivotal Year

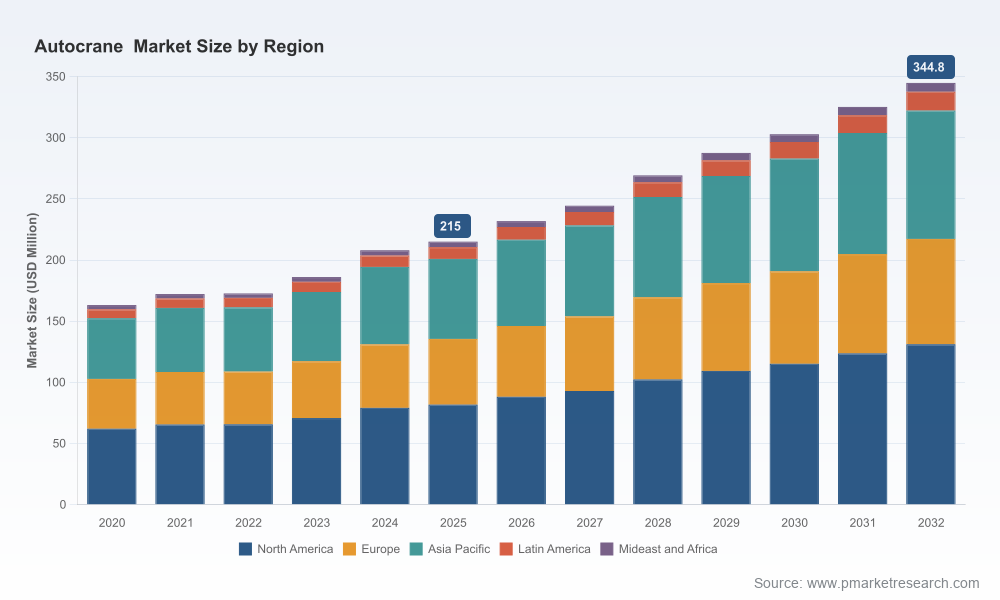

The autocrane market is at an inflection point. After steady expansion through the first half of the decade, the total market value grew from roughly USD 163 million in 2020 to about USD 215 million in 2025. Our forecast points to continued expansion, reaching approximately USD 345 million by 2032 at a compound annual growth rate (CAGR) of 5.2% across the 2026–2032 period. That trajectory reflects a confluence of macro drivers — infrastructure spending cycles, fleet renewal pressures, tighter emissions and safety regulations, and accelerating adoption of telematics and electrified powertrains.

Autocrane Market

For 2026 planning, two implications are immediate:

Autocrane Market

- Balance near‑term service and warranty exposure against medium‑term product investments. Warranty and aftermarket economics are front‑of‑mind as manufacturers extend coverage and customers push for uptime assurances.

- Prioritize modular architectures and digital enablement. Products that simplify electrified powertrain integration and remote diagnostics will gain share as fleets look to reduce total cost of ownership (TCO) and increase utilization.

What the Full Report Gives You (Practical, Actionable Content)

PWC’s Autocrane Market study is designed as an operational decision tool, not just a market narrative. Highlights of the deliverable include:

- Robust market sizing and methodology: historic reconstructions (2020–2025), base‑case projections (2026–2032), and alternative scenario modelling that stress‑tests demand under different macroeconomic, regulatory, and commodity scenarios.

- Demand‑driver frameworks: a mapped view of capex cycles (construction/infrastructure), fleet replacement timing, regulatory shocks (emissions and safety), and aftermarket spend drivers, with quantified sensitivity levers you can apply to your internal forecasts.

- Go‑to‑market playbooks: segmented approaches for OEMs, tier‑1 suppliers, and aftermarket players including channel design, pricing cliffs, warranty structures, and service bundling templates.

- Commercial tooling: downloadable templates for total life‑cycle cost modelling, dealer network optimization, and RFP evaluation matrices to accelerate procurement and product planning cycles.

- M&A and partnership heatmaps: prioritized targets and capability gaps across digital telematics, electrified powertrain partners, and specialized manufacturing assets, with risk‑adjusted valuation heuristics.

- Regulatory and standards horizon: summarized near‑term compliance risks and expected certification timelines that materially affect OEM lead times and product cost structures.

We intentionally omit the granular segment tables and proprietary model outputs in this preview — those are reserved for the full report and interactive dashboards available on our site — but the elements above map directly to the packages executives need to make 2026 investment and operational decisions.

Competitive Landscape — Spotlight: Ramsey Industries

Market concentration remains relatively low, with the top three and top five suppliers accounting for modest shares of the total market. This fragmentation creates opportunity for technology differentiation and consolidation plays. One company that illustrates the current competitive dynamics is Ramsey Industries.

- Profile: U.S.-based, American‑owned manufacturer with domestic manufacturing and a legacy product portfolio that includes the Auto Crane line, winches, crane bodies, and accessories. Ramsey’s product families include the NexStar and the 6‑Series, offered across electric, hydraulic, and hybrid powertrain configurations.

- Digital and product developments (2026): Ramsey debuted Ramsey Connect™, a rugged industrial IoT platform, at high‑visibility industry shows in March 2026, demonstrating live fleet visibility and field testing. Concurrently, Ramsey introduced the NexStar HC‑6 and EHC‑6 models focused on weight reduction, zero‑emission power options, and embedded smart diagnostics to improve safety and uptime.

- Warranty posture: In May 2026 Ramsey extended standard warranty coverage up to 36 months on qualifying products shipped on or after March 1, 2026 — a strategic move that reshapes aftermarket economics and buyer expectations regarding service risk and lifecycle costs.

Why these moves matter strategically: Ramsey’s combined emphasis on telematics, electrification readiness, and extended warranty is emblematic of broader competitive tensions. OEMs are using digital platforms both as retention levers (data‑driven maintenance contracts) and as differentiators in procurement cycles. Warranty expansion transfers certain performance risks to manufacturers and creates near‑term margin pressure while supporting higher recurring aftermarket revenue if executed with efficient parts and service networks.

Key Strategic Implications for 2026 Decision-Makers

The interplay of product innovation, digital enablement, and aftermarket economics yields several crisp choices for firms operating across the autocrane value chain.

- For OEM leadership: accelerate modular electrification and telematics roadmaps. Allocate R&D to scalable subsystems that can be configured across crane families rather than bespoke, single‑model investments. This reduces manufacturing complexity while speeding time‑to‑market for zero‑emission options.

- For aftermarket and service organizations: invest in predictive maintenance capabilities and parts logistics optimization. Extended warranties raise the importance of repair cycle time and first‑time fix rates; telematics data should be integrated into field scheduling and parts forecasting to lower service costs and protect margins.

- For private equity and corporate development teams: favor targets with recurring revenue footprints, digital assets, or manufacturing flexibility. Given the market’s moderate fragmentation, bolt‑on acquisitions that add telematics capabilities, localized service footprints, or lightweight structural expertise can yield scale advantages.

- For procurement and fleet owners: update procurement specs to include digital interoperability, modular battery or hybrid compatibility, and clear service level agreements for uptime and diagnostics. Re‑negotiate supplier contracts to align with performance outcomes rather than pure unit price.

Risk and Contingency Considerations

Several downside risks warrant explicit contingency planning in 2026:

- Warranty and labor cost dynamics: Extended warranty policies, such as Ramsey’s move to 36‑month coverage, can materially affect manufacturer P&Ls if not matched with improvements in reliability or service efficiency. Plan for warranty reserve impacts and scenario closures where labor inflation compresses service margins.

- Supply chain volatility: Component concentration (e.g., specialized winches, control electronics, or battery modules) can introduce lead time and price risk. Dual‑sourcing and the use of standardized subassemblies reduce exposure.

- Regulatory shocks: Accelerated emissions or safety regulations can force product reworks; maintain modularity to shorten compliance cycles and reduce retrofit costs.

- Technology adoption risk: Rapid telematics rollouts improve uptime but require data governance and integration investments. Poorly executed digital rollouts can damage customer relationships and increase churn.

Top 5 Tactical Moves for 2026

- Embed telematics into warranty economics. Tie extended warranty offers to verified telematics data and maintenance compliance to reduce moral hazard.

- Standardize modular interfaces for electrification. Reduce time to certify new powerplants across model lines by defining electrical and mechanical interface standards.

- Create a parts‑availability KPI tied to service contracts. Use telematics to drive proactive parts replenishment, reducing truck rolls and downtime.

- Implement a value‑based sales motion. For fleet customers, sell uptime guarantees and TCO outcomes rather than equipment alone.

- Pursue focused M&A for digital talent and manufacturing flexibility. Small tuck‑ins that bring cloud telematics, rugged displays, or lightweight metallurgy capability are high ROI targets.

How PW Consulting Can Help

Our full Autocrane Market report provides the granular inputs and scenario models needed to operationalize the strategic moves above. Subscribers receive:

- Interactive dashboards with historic and forecast market sizing by segment, region, and application (note: segment‑level figures are included in the full product package but are intentionally withheld in this preview).

- Risk‑adjusted M&A target lists with valuation frameworks, integration playbooks, and expected synergies mapped to product and service lineups.

- Custom workshops to translate market scenarios into actionable 12–36 month product and service roadmaps.

To translate the market’s 5.2% CAGR and the projected growth from a mid‑decade USD ~215 million base into an executable plan for 2026, firms need both the big picture and the detailed levers. This preview surfaces the strategic priorities; the full report supplies the granular segment data, proprietary scoring algorithms, and downloadable tools to execute with confidence.

For immediate access to the full dataset, interactive models, and tailored consulting support, please visit the PW Consulting Autocrane Market page — the only place where the segment‑level tables, regional breakdowns, and company scorecards are published in full.

For detailed analysis of this topic, please visit the official page:Autocrane Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com