Professional Concrete Solutions for Durable and Modern Construction

Home |

2026-04-06 21:22:18

As PW Consulting’s lead industry analyst, I present an executive preview of our comprehensive Truck Tonneau Covers Market study — a decision-grade intelligence product designed to shape corporate strategy through 2026 and beyond. This briefing synthesizes the market’s recent trajectory, systemic drivers and disruptors, competitive dynamics, and the pragmatic playbook embedded in the full report. We intentionally surface the critical directional insights and strategic implications while reserving the granular segment-level metrics for the full report to preserve its proprietary value and ensure your team gains exclusive access to the operational detail required for execution.

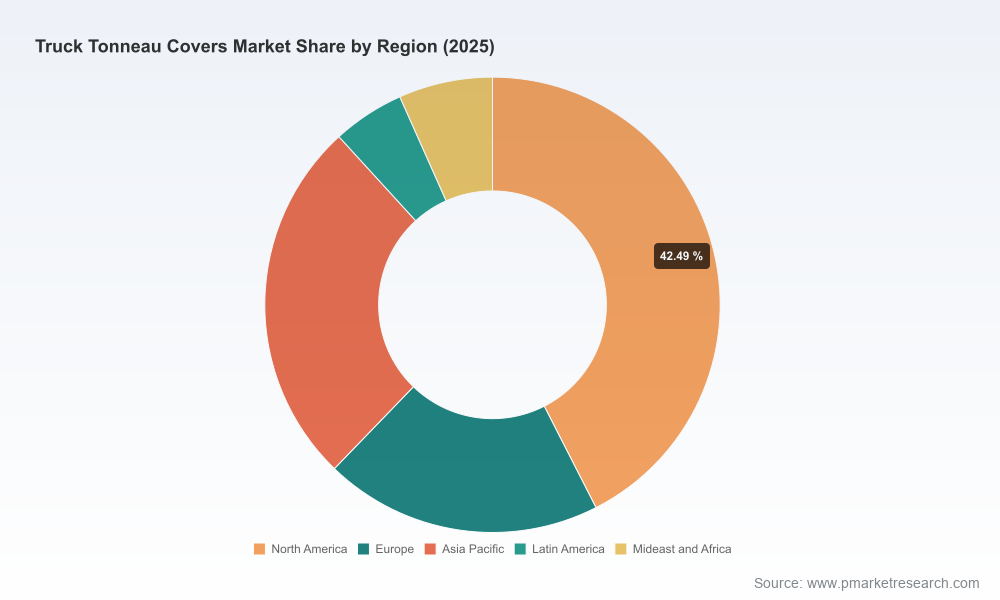

Truck Tonneau Covers Market

The tuck tonneau covers market has demonstrated resilient expansion through the mid-2020s. Using 2025 as the base year, the market is positioned well above pre-pandemic levels and is forecast to continue expanding at a mid-single-digit compound annual growth rate. Our model — grounded in proprietary shipment, pricing and aftermarket replacement curves — projects steady revenue growth across the 2026–2032 forecast horizon, driven by a combination of new-vehicle content penetration, aftermarket upgrades, and product premiumization. For leaders planning capital allocation and product roadmaps in 2026, this trajectory validates near-term investment in capacity, technology differentiation, and channel development while also highlighting the need for targeted risk management.

Truck Tonneau Covers Market

Demand momentum converges with structural supply risks. Recovering consumer spending and an appetite for vehicle personalization are boosting both OEM and aftermarket channels; however, 2026 introduces pronounced trade-policy and supply-chain inflection points that can materially alter sourcing economics and competitive advantage.

Truck Tonneau Covers Market

Premiumization and feature migration are compressing the value chain. Customers increasingly choose hard, retractable and multi-function covers that blend aesthetics, security and utility; this raises average selling prices but requires higher engineering and material sophistication.

Channel complexity intensifies. E-commerce, dealer-installed programs, and large independent installers are fragmenting distribution, demanding more granular channel economics and differentiated marketing strategies from manufacturers and distributors alike.

Product differentiation and feature-led upgrades: Innovations such as low-profile retractables, integrated locking systems, and lightweight aluminum constructions are creating premium tiers and expanding TAM within existing truck owner cohorts.

Aftermarket resilience: Extended replacement cycles and rising discretionary upgrades sustain aftermarket demand even if new-vehicle sales oscillate. That said, success hinges on installer networks and a frictionless digital purchase experience.

Materials and cost pressures: Aluminum and engineered polymer price volatility influences margin profiles, especially for firms with concentrated supplier bases or long lead-time contracts.

Policy and trade friction: Recent trade petition activity and subsequent regulatory action introduce tariff and compliance uncertainty that can rapidly change landed costs and competitive positioning for import-intensive supply chains.

One of the most consequential developments we tracked during our research cycle was a coordinated trade petition filed by a group of domestic manufacturers and distributors early in 2026, followed by the initiation of formal antidumping and countervailing duty investigations by U.S. authorities. These inquiries focus on imports of truck bed covers and have the potential to change cost structures for imported components and finished goods. For executives, this creates a dual-effect scenario: a near-term upside for domestic producers shielded from import pricing pressure, and a medium-term imperative for global players to re-evaluate manufacturing footprints, compliance documentation, and nearshoring opportunities.

Our scenarios model the potential range of policy outcomes and the sensitivity of corporate P&L to duty shocks, enabling leaders to craft staged responses — from tactical inventory management and hedging to strategic reshoring and contract re-negotiation.

The competitive set in this market combines established OEM suppliers, specialty aftermarket brands, and a contingent of vertically integrated players. Market concentration metrics indicate a moderately consolidated top tier — large enough to influence pricing and distribution dynamics, but with sufficient fragmentation to allow nimble entrants and differentiated niche players to win share.

RealTruck, Inc. (United States) — known for retractable and aluminum/steel offerings under established sub-brands. Their portfolio underscores a strategy of platform breadth plus channel depth.

Worksport Ltd. (Canada) — focuses on hard tri-fold aluminum designs with quick-latch and low-profile differentiation, targeting owners who prioritize both function and low visual impact.

Agri-Cover, Inc. (United States) — emphasizes climate durability in roll-up configurations, playing to customers in extreme-weather geographies and commercial applications.

Truck Hero (United States) — offers a broad series spanning soft and hard covers, representing a mass-market, multi-channel approach.

Extang Corporation (United States) — specializes in hard folding solutions with a focus on utility and durability for pickup users.

BAK Industries (United States) — known for foldable soft tri-fold designs with strong OEM and aftermarket recognition.

Truxedo, Inc. (United States) — roll-up solutions oriented to low-profile and easy-use segments.

A.R.E. Accessories LLC (United States) — markets retractable and solid covers with an emphasis on premium finishes and dealer-fit programs.

These players illustrate three viable strategic archetypes: (1) scale-focused incumbents that compete on breadth and distribution; (2) specialization-focused innovators that win on product differentiation; and (3) integrated-service providers that bundle installation, accessories and warranty for higher lifetime value. Our competitive maps include supplier-by-supplier profiles, channel footprint analyses, and go-to-market packages that reveal where consolidation, alliance or white-label opportunities are most attractive.

The full study is structured as a practitioner’s toolkit for executives who must translate market trends into 2026 action plans. Highlights include:

Robust forecasting module: bottom-up revenue models and demand scenarios across 2026–2032 with sensitivity to commodity prices, tariffs and new-vehicle trends.

Go-to-market playbooks: differentiated approaches for OEM partnerships, national distributor agreements, and digital-first aftermarket channels, with recommended economics by channel type.

Product roadmap implications: prioritization matrices for hard vs. soft, retractable vs. roll-up, and accessory integration that balance engineering cost and price elasticity.

Supply chain & procurement guidance: supplier risk heatmaps, dual-sourcing templates, and nearshoring build-vs-buy decision frameworks.

Regulatory response playbooks: scenario-based actions for tariff imposition, including inventory staging, contract clauses, and cost pass-through strategies.

M&A and partnership targets: a curated list of targets and rationale across the value chain for bolt-on consolidation, vertical integration, or capability acquisition (engineering, coating, extrusion).

Commercial levers and pricing tools: elasticity estimates, promotional calendar templates, and channel margin models to inform discounting and dealer incentives.

Implementation roadmap: quarter-by-quarter milestones and KPIs for 6–18 month program execution to capture share or de-risk exposure.

Prioritize supply-chain optionality: Establish alternative sourcing lanes and localize critical subassemblies where feasible. Even modest nearshoring can materially reduce tariff and logistics exposure under adverse trade rulings.

Segment product investment: Allocate R&D and capex toward high-margin premium tiers and multifunctional covers, while using scale manufacturing to protect value in the mainstream segments.

Channel economics overhaul: Rebalance investments toward direct-to-consumer digital platforms and franchisee installer networks, while renegotiating distributor terms to reflect changing inventory and service expectations.

Proactive regulatory engagement: Documented audit trails, robust country-of-origin controls, and pre-emptive compliance statements will reduce disruption in the event of duties or import restrictions.

Commercial differentiation through service: Warranties, installation guarantees, and modular accessory ecosystems increase retention and create recurring revenue streams.

Scenario-based M&A posture: Prepare short lists and financing readiness for opportunistic acquisitions if duties materially increase domestic valuations or fragment competitor balance sheets.

For 2026 planning cycles, this market is neither a speculative gamble nor a slow-moving commodity: it is a measured growth opportunity with time-bound risks that require actionable mitigation. The strategy choices you make this year — around sourcing architecture, product mix, channel engineering and regulatory preparedness — will determine whether you capture value from expanding demand or merely survive a period of policy-driven disruption.

PW Consulting’s full report contains the granular segmentation, competitive scorecards, and executable templates that corporate leadership teams require to convert these strategic priorities into measurable outcomes. Access to the complete dataset and implementation playbooks will enable you to align 2026 budget cycles, capital deployments and commercial incentives to the highest-probability scenarios.

Request the full study to obtain the detailed segmentation and the scenario-level financial models that underpin our forecasts.

Schedule a consultative workshop with PW Consulting to translate findings into a bespoke 18-month execution plan for your business or portfolio companies.

For detailed analysis of this topic, please visit the official page:Truck Tonneau Covers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com