Clove Cigarettes Market Size, Share, Diagnostics Trends, and Forecast by 2032

Other |

2026-06-29 10:27:46

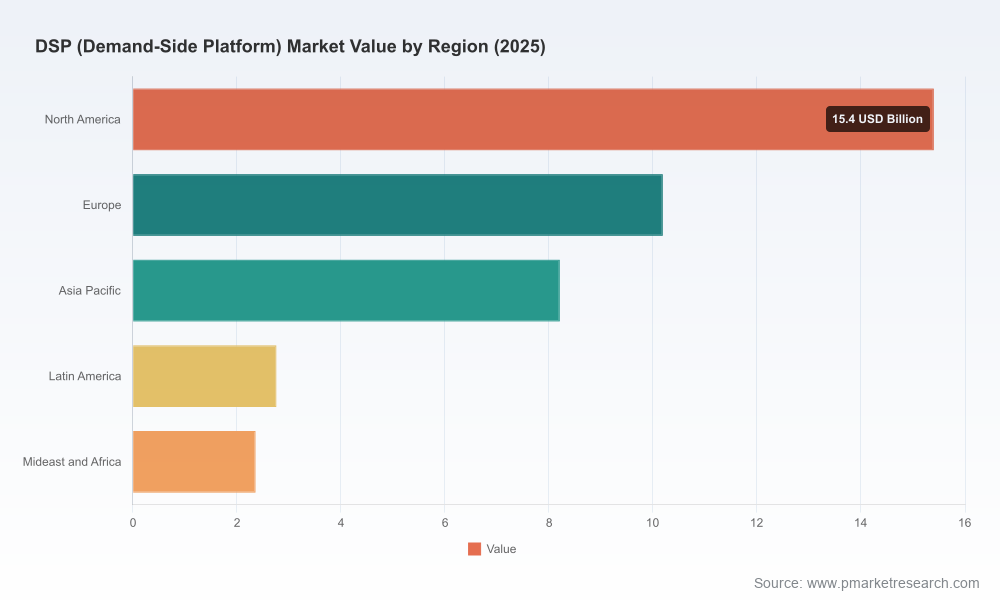

As programmatic advertising moves from tactical buying to strategic media architecture, demand-side platforms (DSPs) are now core components of enterprise marketing stacks. PW Consulting’s latest DSP Market study — anchored on a 2025 base year and projecting through 2032 — quantifies a fast-growing market and unpacks the operational, regulatory, and competitive forces that will determine winners and losers over the next seven years. The market grew from USD 16.31 Billion in 2020 to USD 38.92 Billion in 2025 and is forecast to reach USD 131.52 Billion by 2032, reflecting a 19.0% compound annual growth rate (CAGR) for the forecast period 2026–2032. This “preview” distills the strategic takeaways senior leaders need for 2026 planning while deliberately withholding granular segment tables and vendor scorecards to incentivize direct access to the full research package.

DSP (Demand-Side Platform) Market

Budget allocation and media strategy are converging: DSPs now influence channel mixes, measurement methods, and creative workflows. Choosing the wrong platform can lock teams into outdated identity approaches, limit CTV and video reach, or impose unsustainable compliance costs.

DSP (Demand-Side Platform) Market

Infrastructure and data strategy are becoming core enterprise investments: DSP performance is increasingly driven by compute, first‑party data activation, and model orchestration rather than simple bidding logic. That elevates procurement discussions from “feature checklists” to long‑term architecture choices.

DSP (Demand-Side Platform) Market

Regulation and geopolitics are non-negotiable inputs: Changes in privacy regimes and cross-border data rules now materially impact DSP vendor selection, partnership design, and measurement methodologies.

The DSP market’s trajectory is clear: strong, sustained expansion underpinned by deeper programmatic adoption across video, connected TV (CTV), and omnichannel formats. Our base-year analysis shows that after a five-year expansion from 2020 to 2025, the market accelerates into the forecast window, reaching an estimated USD 44.9 Billion by 2026 and continuing toward USD 131.52 Billion in 2032 (2026–2032 CAGR: 19.0%).

What drives this growth? Three macro forces: (1) media migration toward digital and addressable channels (notably CTV and video), (2) the monetization appetite and infrastructure investment by major platform owners, and (3) technological maturation — particularly the application of AI to yield optimization, identity graphing, and creative personalization. These drivers are uneven across regions and use cases; the full report contains the territorial and application-level granularity enterprise teams use for budgeting and market-entry decisions. In this preview we intentionally omit those segmented tables so readers must consult the source for tactical numbers and vendor maps.

The vendor landscape is multi-modal: global cloud-first independents, vertically integrated platform owners, specialized performance players, and regional full-stack providers each occupy strategic niches. Key dynamics we observed across the competitive set include:

Data ownership and identity strategies are differentiators. Independent DSPs emphasize interoperability and neutral bidding; platform owners leverage proprietary signals and walled‑garden inventory. Enterprises must decide whether to prioritize reach and closed-loop measurement or portability and vendor neutrality.

AI and autonomy are table stakes. Providers are embedding real-time decisioning and autonomous campaign optimization into their stacks. Recent vendor moves demonstrate this trend: Viant rolled out advanced AI autonomous features to enhance real-time decisioning in 2026, while StackAdapt launched integrated email and a Data Hub capability the same month, blurring martech and adtech boundaries.

Infrastructure investment drives differentiated service. Adform’s announcement of full-stack infrastructure for next‑generation DSP operations signals that control over the processing stack — from bidding latency to data throughput — will be a competitive lever going forward.

CTV partnerships and inventory access are pivotal. Platform-to-platform deals (for example, major cloud and media platform integrations) materially change reach and measurement potential; examples from 2025–2026 show vendors locking in CTV distribution through strategic alliances and product launches.

Representative vendor archetypes in the study include independent cloud DSPs focused on real‑time bidding and neutrality, AI‑first performance DSPs, omnichannel solution providers aligned with full-stack martech, and hyperscale platform owners offering first‑party data integration. The full report includes discrete profiles and comparative scorecards for the named players (The Trade Desk, Viant, Adform, SmartyAds, StackAdapt, Google, Amazon, Adobe, Microsoft/Xandr), but this introduction highlights strategic posture rather than numerical rankings.

External forces are reshaping operating models. Three immediate implications for enterprises:

Privacy-first identity models require modernization. Industry reports and recent federal rules (including a 2025 U.S. Department of Justice ruling affecting cross-border sensitive data flows) are forcing DSPs to re-architect data ingestion, storage, and signal enrichment pipelines. Enterprises must factor legal-admissibility and technical portability into vendor contracts.

Compliance costs are increasing. Geopolitical tensions and evolving broadcaster and regulator positions have raised the cost of handling international inventory. This changes total cost of ownership calculations across DSP vendors with different global footprints.

Platform economics are shifting. Major platform operators are investing heavily in ad infrastructure — Amazon’s sustained ad revenue and its strategic integrations are an example — which increases supply competition but also raises questions about measurement sovereignty and competitive neutrality.

To convert market momentum into durable advantage, organizations should translate this market intelligence into six practical actions:

Run an architecture-first vendor selection: prioritize vendors whose technical architecture aligns with your identity roadmap, data governance constraints, and scale needs. Demand proof-of-performance under your data and compliance settings.

Prioritize first‑party data activation: accelerate investments in data clean rooms, unified customer profiles, and consented identity graphs. DSP selection should support seamless activation of these assets.

Adopt a scenario-based procurement posture: evaluate DSPs under alternative regulatory and inventory-access scenarios — including stricter cross‑border rules and expanded CTV adoption — rather than a single-point forecast.

Insist on transparent measurement and independent verification: given rising scrutiny, require vendors to support independent auditing and cross-platform attribution standards to avoid measurement bias.

Design for interoperability and exit: negotiate contract terms that preserve data portability and avoid technical lock-in. This preserves strategic optionality as market dynamics change.

Scan for M&A and partnership triggers: for enterprises with advertising-driven monetization, consider partnerships or selective investments in specialist DSPs to secure strategic capabilities (e.g., CTV, first‑party enrichment, or autonomous optimization engines).

Run a two-week technical proof-of-concept focusing on latency, identity matching rates, and data ingestion limits.

Validate the vendor’s compliance framework against your legal and engineering requirements (data residency, cross-border flows, consent capture).

Map integration touchpoints into your martech stack and estimate implementation timelines and engineering effort.

Establish KPIs that reflect both performance and governance (e.g., viewability-adjusted ROI, identity resolution rate, auditability index).

The comprehensive study — built on a 2025 base year and forecasting 2026–2032 — includes:

Methodology and modeling assumptions, including scenario variants for regulatory and inventory access changes.

Full historical series and granular forecasts by region, format, and application, with a transparent reconciliation to market revenue totals.

Vendor benchmarking and scorecards across technical, commercial, and regulatory dimensions for leading DSPs, including product roadmaps and recent developments.

Actionable procurement templates, a technical proof-of-concept guide, and negotiation playbooks designed for enterprise buyers.

M&A heatmaps, partnership opportunity maps, and a prioritized list of capability bets for enterprises building in-house programmatic capabilities.

Note: this preview intentionally omits the detailed region-by-region, application-level splits and the vendor-level revenue tables that underpin our forecasts. Those tables and raw datasets are available with the full report.

For 2026, DSP strategy is no longer an implementation detail — it is a core business decision with consequences for brand reach, customer data strategy, and compliance posture. The market’s compound expansion trajectory through 2032 signals both opportunity and complexity: rapid growth attracts capital and innovation, but also amplifies regulatory risk and competitive concentration in inventory and identity. PW Consulting’s full DSP Market report equips leaders with the numbers, the vendor intelligence, and the operating playbooks needed to make confident choices in this environment. To access the complete segmented forecasts, vendor scorecards, and procurement templates, consult the full research package available on our website.

For detailed analysis of this topic, please visit the official page:DSP (Demand-Side Platform) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com