Fish Collagen Hydrolysate Market Size, Share & Growth Outlook

Art |

2026-07-01 06:51:44

As building façades reassert their strategic role in urban sustainability and brand differentiation, spandrel glass has moved from a niche, commoditized input to a design-and-performance lever for developers, façade contractors, and materials OEMs. PW Consulting’s latest Spandrel Glass Market study — anchored on a 2025 base year with a 2026–2032 forecast horizon — shows a resilient industry trajectory, underpinned by secular demand drivers and a moderate compound annual growth rate (CAGR) of 6.98% through the forecast period. The study quantifies the market’s expansion across the historical 2020–2025 window and projects the market to materially increase from its 2025 base, reaching substantially higher levels by 2032.

Spandrel Glass Market

Investment timing: The sub-7% CAGR suggests steady, capital-efficient growth rather than a hypergrowth environment. That profile favors incremental capacity additions, targeted partnerships, and bolt-on acquisitions over large greenfield builds for most mid-sized players in 2026.

Spandrel Glass Market

Margin management: With predictable volume growth, the margin delta will be driven more by product mix, coating technologies, and vertical integration of frit supply than by topline expansion alone. Companies that control frit formulation or tempering processes are positioned to capture disproportionate margin improvement.

Spandrel Glass Market

Risk calibration: Supply-chain and regulatory risks (see Dynamics) are front-and-center for procurement and operations teams; 2026 should be used to firm up hedging strategies, supplier agreements, and contingency capacity.

Our modeling — using a combination of bottom-up plant-level capacity analysis and top-down demand drivers (construction activity, curtain-wall replacement cycles, and specification shifts) — shows the market evolving in quality and complexity as much as it grows in size. The 2025 base forms a practical springboard into 2026: buyers and manufacturers can expect higher absolute volumes and a steady premiumization of product specifications (performance coatings, insulated panels, and higher-durability frit systems).

For corporate strategists, the near-term choices are clear: prioritize product portfolio rationalization to capture value from higher-spec applications; defend core segments through reliability and lead times; and pursue selective geographic entry where regulatory or specification tailwinds accelerate adoption.

Raw materials and formulations: Spandrel glass production is materially dependent on ceramic frit chemistry and high-solids coating systems. Industry formulations commonly exceed 90% solids by volume, reflecting a concentration on inorganic binders and colorant dispersion technologies to ensure durability and color stability over tempering. Control of frit sourcing and formulation know-how remains a critical margin lever.

Thermal processing and quality control: Precision tempering above 600°C is often required to achieve long-term performance for spandrel panels used in high-rise curtain walls. Thermal processing consistency — and the capital equipment and process controls that deliver it — separates producers who can supply architectural-grade panels from lower-tier suppliers.

Regulatory and sustainability pressures: Building codes and façade fire-safety standards, along with lifecycle assessments used by developers, are prompting tighter specifications for coatings, frits, and insulating cores. In 2026, purchasers will increasingly seek third-party validation for thermal and environmental performance.

Concentration and competition: The market displays moderate concentration — with the three- and five-firm concentration ratios indicating a landscape where national and regional leaders coexist with a meaningful segment of specialized or local producers. This structure creates room for scale-driven margin capture while leaving tactical niches for specialist innovators.

The competitive topology combines large multinational glass manufacturers with specialized spandrel fabricators. Key players profiled in our study include major architectural glass producers and niche panel integrators. Each competitor exhibits differentiated capabilities:

Vitro Architectural Glass (Pittsburgh, PA) — positioned as an innovator with proprietary pre-coated frit products aimed at simplifying façade assembly and reducing on-site variability. Recent product launches signal a push toward marketed, branded spandrel offerings.

Guardian Glass (Dearborn, MI) — emphasizes high-precision coating platforms for uniform color and durability, an attractive proposition for curtain-wall specifiers seeking color consistency over large façade areas.

Insulite Glass Company (Kansas City, MO) — a specialist route-to-market focused on ceramic enamel systems and insulated panel assemblies, catering to projects that prioritize thermal performance alongside concealment.

Mapes Panels (Colorado) and Jersey Tempered Glass (New Jersey) — examples of companies leveraging panel-level integration and tempered glass capabilities to shorten installation cycles and provide turnkey façade components.

Dreamwalls by Gardner Glass, Hartung Glass, Saint-Gobain (Paris), and NSG Group (Tokyo) — represent the broader ecosystem of coating technology suppliers and global glass manufacturers, offering a spectrum from commodity tempered lites to high-performance coated systems.

Notable recent developments tracked in the study include a product launch from a leading North American innovator in early 2025 and a strategic joint venture announced by a major European manufacturer in late 2025 to expand capacity in the Middle East. Both moves underscore two themes: branded product differentiation and regional capacity positioning to capture localized demand growth.

The full study is designed as an operational toolkit as much as an analytical report. It contains:

Market sizing and validated forecasts (2020–2032) with scenario modeling under alternative construction and regulatory outcomes.

Segment-level analysis (by type, application, and region) with supply-demand balances and elasticity assumptions — presented in an executive-friendly format and with downloadable datasets for in-house modeling.

Raw material cost and availability tracker, including frit formulation sensitivities and a supplier map to assess single-sourcing risk.

Competitor profiles and benchmarking: plant footprints, technology stacks, product portfolios, and go-to-market strategies for the key manufacturers and fabricators.

Procurement and commercial playbooks: tender language recommendations, specification checklists, and pricing negotiation levers tailored for developers and façade contractors.

M&A and partnership heatmaps: target lists and valuation multipliers derived from comparable transactions and scale economics.

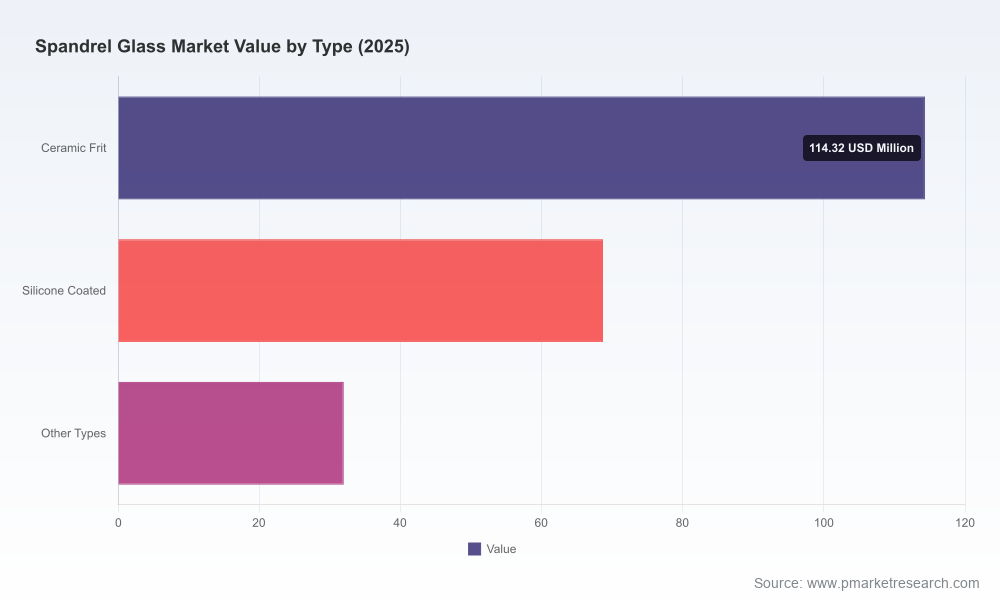

In keeping with our “trailer” approach, the public summary above intentionally omits the granular split values and specific regional/application dollar figures. These are included in the report’s proprietary datasets and interactive dashboards, which are available through the full study.

Manufacturers — Focus on product rationalization: accelerate commercialization of pre-coated and insulated panel systems that reduce on-site labor and specification risk. Invest selectively in tempering capacity upgrades rather than broad-capacity additions.

Suppliers — Lock in frit supply and invest in formulation IP. Given the centrality of high-solids ceramic frit chemistry to performance, owning or partnering on frit formulation can be a sustainable source of differentiation.

Developers and façade contractors — Shift procurement toward performance-based contracts and include lifecycle metrics in bid evaluations to capture long-term cost of ownership advantages.

Private equity and M&A players — Target bolt-on acquisitions that add specialized coating capability or regional delivery density rather than large platform bets; look for assets that close logistics gaps or shorten lead times.

R&D and sustainability teams — Prioritize formulations and tempering processes that reduce energy intensity while maintaining color and fire performance; early movers on validated low-carbon production will gain specification advantage with institutional developers.

Our analysis turns market projections into actionable steps. In 2026, firms will need a clear, prioritized roadmap: where to invest in capex, when to secure raw material supply, which partnerships to pursue, and how to structure commercial agreements to capture premium product economics. The study supplies the data, benchmarked KPIs, and decision frameworks executives need to convert market signals into measurable action plans.

Spandrel glass presents a compelling, mid-growth opportunity in the building materials landscape: growth is steady, technological differentiation matters, and the competitive field rewards both scale and specialized capabilities. For executives planning their 2026 playbook, the imperative is to convert the predictable volume growth indicated by our base-case forecasts into sustainable margin expansion through product engineering, supply-chain control, and targeted partnerships.

PW Consulting’s full Spandrel Glass Market study contains the proprietary datasets, scenario tools, and tactical playbooks necessary to operationalize these strategic imperatives. For executives serious about turning 2026 into a year of decisive positioning, the complete report is the reference manual.

For detailed analysis of this topic, please visit the official page:Spandrel Glass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com