PVDF Resin Market 2026 Strategic Brief: Navigating Growth, Scarcity and Regulatory Shifts

As PVDF (polyvinylidene fluoride) moves from a specialty polymer into a strategically important material for electrification, chemical processing and high-performance coatings, corporate leaders must translate geopolitical, supply-chain and regulatory noise into measured strategic moves. This briefing — an introduction to PW Consulting’s full PVDF Resin Market research — explains why the 2026 decision window is pivotal, what macro trends will determine winners and losers, and how our analysis transforms raw data into executable options for C-suite teams and investor committees.

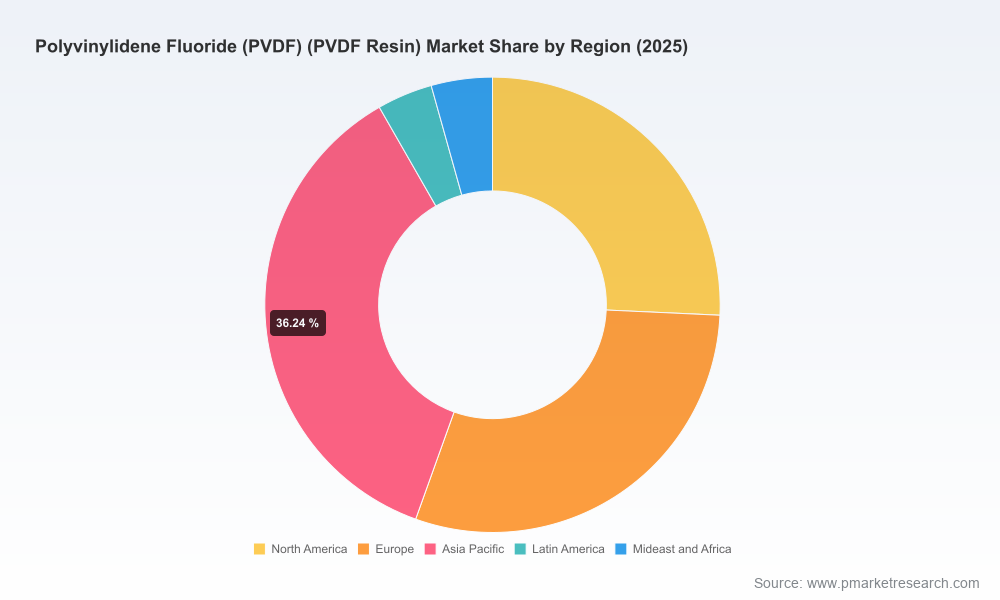

Polyvinylidene Fluoride (PVDF) (PVDF Resin) Market

Market snapshot: trajectory and momentum

Our market model, grounded in five years of historical observation and forward-looking unit-cost analysis, shows the global PVDF resin market accelerating through the mid-decade. The market expanded steadily from the early 2020s and reached USD 215 million (base year 2025). Over the forecast horizon (2026–2032) we project a compound annual growth rate (CAGR) of 7.4%, bringing the market to roughly USD 357 million by 2032. That trajectory reflects durable demand from electrification value chains, membrane and filtration growth, and niche industrial applications where PVDF’s chemical resistance and dielectric properties are irreplaceable.

Polyvinylidene Fluoride (PVDF) (PVDF Resin) Market

Why 2026 is a strategic inflection for PVDF decisions

- Capacity rhythms vs. demand inflection: Several major producers have announced staged capacity projects entering service between 2026 and 2028. These moves will shift marginal supply dynamics and create local price differentials that persist unless end-market demand scales commensurately.

- Supply fragility: Recurrent upstream outages for critical feedstocks have shown that short-term shocks can propagate rapidly into spot-market volatility for PVDF and its monomers. Companies without robust sourcing or hedging strategies experienced outsized cost exposure during 2024–2025.

- Regulatory tightening with compliance calendars: Evolving reporting and oversight of PFAS-related chemistries is creating compliance cliffs in key jurisdictions. Timing for reporting and disclosure obligations into 2026 means procurement, product stewardship and regulatory teams must align now or risk operational disruptions and reputational costs.

- Commercial window for differentiation: The market structure — where a modest number of global suppliers capture a meaningful share — rewards early movers that secure long-term supply contracts, co-develop battery-grade formulations, or vertically integrate critical upstream inputs.

Market dynamics — what’s driving price, availability and adoption

Three paired dynamics are driving near-term strategy:

Polyvinylidene Fluoride (PVDF) (PVDF Resin) Market

- Raw-material and feedstock shocks: Hydrofluoric-acid and VDF monomer supply tightness in 2025 led to production cuts and marked price moves. Regional environmental enforcement in China also pushed feedstock costs higher. For buyers and integrators, this elevates the importance of dual-sourcing, inventory buffers and forward-offtake arrangements.

- Regulatory uncertainty and reporting timelines: Regulatory authorities have accelerated scrutiny on PFAS and related fluoropolymers. Proposed and interim rules announced through 2025 extend reporting deadlines and broaden definitions, creating compliance cost uncertainty for manufacturers and importers. Companies must model regulatory scenarios into both product strategy and M&A diligence.

- Supplier capacity churn: Announcements from key producers signal meaningful additions to available capacity over the next three years. Combined with contract signings by specialty suppliers, these expansions will alter negotiation leverage for buyers — particularly in battery materials — but only if demand growth keeps pace.

Competitive landscape — what the leading players tell us

The PVDF value chain is characterized by a mix of legacy chemical majors and regional specialists. Market leadership is concentrated enough that moves by a top-tier producer reshuffle supply balances globally.

- Arkema S.A. (France) — A long-standing leader with strong positioning in battery-grade resin and performance coatings. Its announced capacity projects in North America and Asia reflect a deliberate strategy to be proximate to large battery and industrial markets.

- Syensqo S.A. (Belgium) and Solvay S.A. (Belgium) — Both supply established PVDF portfolios including battery-grade offerings; contract wins and regional plant restarts by these firms will be consequential in the near term for battery supply chains.

- Kureha Corporation & Daikin Industries (Japan) — Technology-focused producers with deep experience in high-performance grades; their product breadth supports premium-margin segments where performance justifies price resilience.

- 3M (United States) and Gujarat Fluorochemicals (India) — Provide complementary market access and local-production capabilities in specialty applications and emerging markets, respectively.

Collectively, the market is neither a classic monopoly nor atomized: top players capture a material share of revenue, leaving space for regional and application-focused specialists to prosper through customer intimacy and formulation know-how. Our full report contains supplier scorecards, capacity timelines, and a play-by-play of recent commercial developments that influence 2026 supplier selection strategies.

What PW Consulting’s full report delivers — practical outputs for 2026 decisions

We designed the research not as an academic exercise, but as a decision-useful toolkit for executives. Highlights include:

- Forward demand model with scenario branches (base, constrained feedstock, accelerated EV adoption) to stress-test capacity plans and contract tenure assumptions.

- Pricing & margin ladder that reconstructs cost drivers from VDF feedstock through polymerization, capturing energy, environmental compliance and logistics inputs — enabling procurement to calibrate negotiating targets.

- Supplier risk matrix integrating operational, regulatory and geo-political risks, scored to prioritize contractual counterparties and contingency stock levels.

- Regulatory impact analysis that translates PFAS and chemical reporting timelines into direct financial and operational exposures, with step-by-step compliance checkpoints for manufacturers and importers.

- Commercial playbooks tailored to battery-material buyers, membrane manufacturers and coatings integrators — including term-sheet archetypes, penalty-and-incentive clauses for force majeure, and dual-sourcing templates.

- M&A & capex lens that identifies strategic acquisition profiles, greenfield timing windows, and ROI thresholds under different feedstock-price scenarios.

Each deliverable is accompanied by downloadable models and a decision checklist that boards can use in Q1–Q2 2026 to lock in supply lines or initiate expansion projects.

Actionable strategic moves for 2026

Based on our synthesis of market and supplier developments, we recommend leadership teams prioritize the following actions in 2026:

- Negotiate staged offtake agreements: Secure partial long-term volumes with flexible take-or-pay tranches to balance certainty with optionality as capacity additions come online.

- Hedge upstream exposure: Where possible, lock forward contracts or financial hedges on monomer feedstocks and critical intermediates to de-risk sudden spot spikes tied to HF or VDF supply disruptions.

- Accelerate product stewardship governance: Implement a cross-functional PFAS-response team to map product portfolios against evolving reporting requirements and to prepare substitution or disclosure strategies.

- Prioritize co-development for battery binders: Buyers and cellmakers that co-invest in formulation optimization with PVDF suppliers can secure preferential supply and incremental performance gains.

- Build regional buffers: For manufacturers operating throughput-sensitive lines, short-term inventory buffers or local sourcing in multiple jurisdictions reduce outage exposure from single-region environmental enforcement.

Why executives should read the full PW Consulting PVDF report

This article surfaces the high-level market dynamics, supplier movements and regulatory forces that make 2026 a decisive year. Our complete report translates these forces into executable tactics — with gated, proprietary segmentation-level forecasts, supplier market shares, and contract-play templates that are intentionally not reproduced here. That level of granularity is what materially alters procurement bids, capex timing and M&A valuation assumptions.

Next steps

For boards, strategic procurement teams, and investors evaluating plastics and battery-material exposure, the full PW Consulting PVDF Resin Market report is structured to accelerate informed decisions in 2026: scenario-modeled demand forecasts, supplier scorecards, tactical contracting artifacts, and compliance roadmaps. Accessing the complete dataset and model will convert this strategic briefing into a prioritized operational plan tailored to your portfolio.

Contact PW Consulting to schedule a briefing and receive the gated datasets, or to commission a tailored workshop that applies our models directly to your supply chain and product roadmaps.

For detailed analysis of this topic, please visit the official page:Polyvinylidene Fluoride (PVDF) (PVDF Resin) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com