Hemp Market — Strategic Outlook for 2026: A PW Consulting Preview

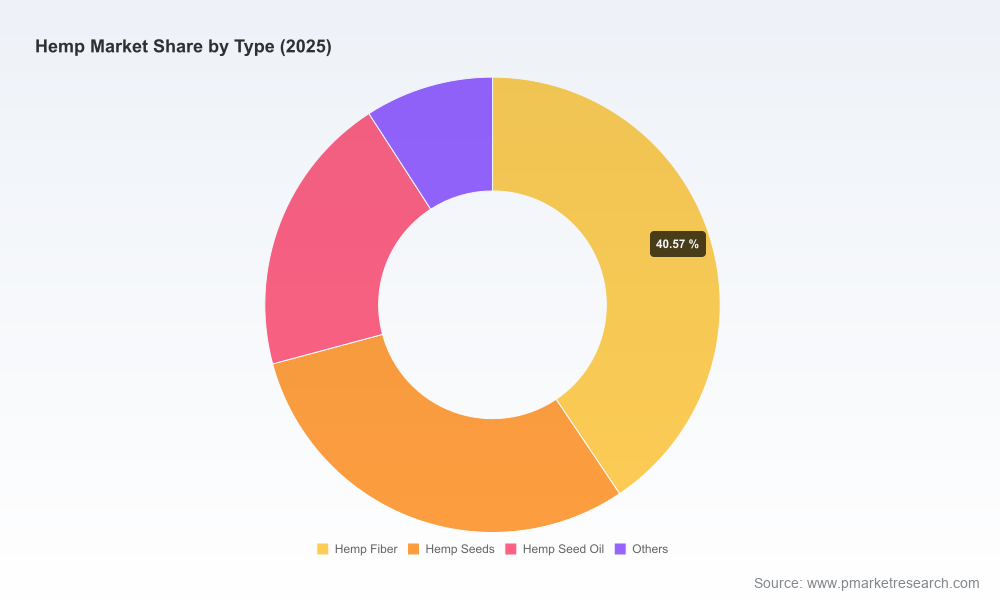

As firms set budgets, capital plans, and partnership roadmaps for 2026, the industrial hemp sector presents a rare combination of rapid expansion, regulatory flux, and fragmented competitive structure. Our new market research (base year 2025; historical window 2020–2025; forecast 2026–2032) quantifies that growth and translates it into practical decision levers for executives considering market entry, scale-up, M&A, or vertical integration. At the headline level, the global hemp market is estimated at USD 255.0 Million in 2025 and is projected to reach approximately USD 721.8 Million by 2032 — a compound annual growth rate (CAGR) of 16.1% over the forecast period. This preview highlights the strategic implications we identify for 2026 decision-making without disclosing the report’s detailed subsegment datapoints, which are reserved for subscribers and purchasers.

Hemp Market

Why 2026 Is a Pivotal Year

- Regulatory inflection points: Policy changes currently scheduled to take effect through late 2026 have direct implications for compliance costs, testing regimes, and product eligibility for mainstream retail channels.

- Operational scale-up window: Several large-scale processing investments commissioned in late 2025 and early 2026 create new capacity and alter bargaining dynamics across the supply chain.

- Fragmented supplier base: Market concentration metrics indicate a highly fragmented landscape (CR3 ~21%; CR5 ~31%), creating M&A opportunities and scope for strategic partnerships that can unlock scale economics.

For commercial leaders, the interaction of these three forces means 2026 will determine who captures the next wave of demand and at what margin.

Hemp Market

Data-driven market trajectory

Between 2020 and 2025 the market experienced a clear acceleration driven by product diversification and greater institutional investment. The market reached USD 255.0 Million in 2025 and, under our base scenario reflecting current regulatory trajectories and adoption trends, expands at a 16.1% CAGR to roughly USD 721.8 Million by 2032. That pace implies a tripling of aggregate market value over seven years — a scale of expansion that will reward early strategic positioning while penalizing firms that delay investments in processing, quality systems, or route-to-market.

Hemp Market

We model multiple scenarios in the full report — from conservative to upside — reflecting sensitivities to regulatory timelines, laboratory testing capacity, and end-market adoption rates. The scenarios are backed by bottom-up capacity analysis, supplier cost curves, and demand elasticities that surface realistic revenue pathways for different business models (e.g., raw-material suppliers, processors, ingredient brands, construction-product OEMs).

Strategic implications for 2026 decision-making

- Compliance-first CapEx and inventory planning. With federal definitions and testing requirements shifting in 2026, capital investments in compliant testing, traceability, and storage systems must be synchronized with regulatory deadlines to avoid stranded inventory or recalls. The short-term delay in enforcement of certain testing requirements provides breathing room, but it should be treated as an opportunity to harden systems rather than as permission to defer investment.

- Secure processing and offtake early. Newly commissioned processing capacity increases throughput but also concentrates bargaining power with firms that control primary processing (gins, decortication, oil extraction). Firms seeking reliable margins should prioritize strategic offtake agreements and co-investment opportunities with capacity owners.

- Channel diversification — act now on retail access. Jurisdictional pilots that expand permitted retail channels (including grocery and convenience formats) open shelf-space opportunities. Companies that can demonstrate compliance and consistent supply will capture first-mover advantage in mainstream retail rollouts.

- M&A and partnership playbook. Given the market’s fragmentation, targeted acquisitions can deliver rapid access to processing, IP, or distribution capability at attractive multiples. However, acquirers should stress-test targets against likely regulatory adjustments and integration complexity tied to agricultural seasonality.

- Product differentiation through sustainability and circularity. Zero-waste operations and low-carbon processing are not just ESG signaling — they materially affect unit economics across higher-value applications (e.g., technical fibers, construction inputs). Investors should value demonstrated circularity as an operational efficiency, not merely marketing optics.

Operational priorities for 2026

- Audit and upgrade traceability and lab-testing workflows to align with anticipated federal definitions and lab accreditation requirements.

- Pursue preferred-supplier or long-term offtake contracts with facilities that can demonstrate low waste and scalable output.

- Accelerate product development for mainstream retail channels where licensing pilots are expanding to grocery and convenience formats.

- Model inventory buffers to account for harvest seasonality and potential delays in lab testing enforcement timelines.

Competitive landscape — what to watch

The sector contains a mix of asset-heavy processors, product innovators, and niche equipment suppliers. Below we offer concise strategic reads on core firms referenced in our analysis and what their positioning implies for potential partners or competitors. The firms profiled are representative, not exhaustive, and our full report contains expanded company dossiers and financial benchmarking.

- IND HEMP (Montana, United States) — A family-owned company that operates along both seed and fiber value chains. Their investment in processing infrastructure makes them a logical partner for brands seeking domestically sourced inputs. Strategic takeaway: access to IND HEMP’s infrastructure can accelerate domestic supply-chain scaling but requires long-term commercial agreements to secure capacity.

- Symbiosis Living (Michigan, United States) — An apparel manufacturer focused on sustainable hemp textiles with international sourcing experience. Their brand-and-design capabilities make them a readymade partner for consumer brands seeking rapid product diversification. Strategic takeaway: consider co-branded capsule collections to validate mass-market appeal before scaling.

- Panda Biotech (Texas, United States) — Commissioned a major zero-waste industrial hemp processing facility in late 2025. This represents a step-change in regional processing throughput and sets a new operational benchmark for circular processing. Strategic takeaway: capacity concentration around large, efficient processors is likely to compress margins for smaller processors and create opportunities for downstream integration.

- Boardwurks (United States) — Specializes in sustainable composite fiberboard using hemp and recycled inputs. Strategic takeaway: firms targeting construction and modular building markets will find differentiated value by partnering with engineered-material suppliers to reduce embodied carbon.

- HempWood (Kentucky, United States) — Produces hardwood-alternative building products from hemp. Strategic takeaway: product innovation that substitutes legacy materials is a strong route to premium pricing in sustainable construction projects.

- Americhanvre (United States) — A practitioner in hempcrete and lime-based insulation applications. Strategic takeaway: construction adoption will accelerate with clearer building-code guidance and performance case studies; developers should pilot with proven integrators.

- Hemp Press (Oregon, United States) — Niche but meaningful player in hemp paper and print services; signals opportunities for premium, eco-branded packaging and promotional use-cases.

- Hart Hemp Co. (Maryland, United States) — Industrial grower offering contract cultivation—critical to secure raw-material continuity during scale-up phases.

- Bish Enterprises (Nebraska, United States) — Specialized equipment provider; strategic investments in harvesting and planting technology materially affect unit cost curves for growers.

Collectively, these firms exemplify the industry’s asset and capability heterogeneity: from upstream agricultural services to midstream processing and downstream product manufacture. That heterogeneity drives both competitive friction and collaborative opportunity.

Regulatory and ecosystem dynamics

- Federal definition change: Legislation passed in late 2025 amends the federal hemp definition to a specified THC threshold effective November 12, 2026. Companies should map product portfolios to this timeline to minimize compliance risk.

- Laboratory testing enforcement: The USDA’s delay in enforcing a requirement for DEA-registered laboratory testing until December 31, 2026 creates a transitional window. Use that time to certify partners and establish validated testing protocols rather than deferring quality investments.

- State-level pilots and access: A number of states have begun to open mainstream retail channels to hemp-derived products; firms must localize market-entry plans to leverage early retail slots and avoid misaligned national rollouts.

- Supply-chain networks: State-level directories and industry consortia are strengthening linkages among growers, processors, and manufacturers; engage proactively to reduce sourcing friction and discover partnership leads.

What our full report delivers (practical content)

Our comprehensive study is structured to help commercial, product, and corporate-development teams make executable 12–36 month plans. Key deliverables include:

- Bottom-up market model (2020–2032) with scenario analysis and sensitivity testing.

- Detailed segment modeling and demand drivers by application and product type (note: segment-level figures are available in the full report).

- Supply-side capacity maps, including processing facilities, equipment providers, and lab accreditation pathways.

- Competitive profiling with operational KPIs, strategic risk ratings, and acquisition attractiveness scores.

- Regulatory timeline, compliance playbook, and a practical checklist for 2026 readiness.

- Commercial go-to-market templates for channel pilots, pricing strategies, and long-term offtake negotiations.

We intentionally withhold granular subsegment disclosures in this preview to preserve the tactical value of our proprietary modeling; subscribers receive the full segmentation breakdown and the downloadable data tables needed for financial planning.

How PW Consulting recommends clients act in 2026

- Prioritize investments that buy optionality: traceability systems, flexible processing agreements, and multi-jurisdictional compliance frameworks.

- Use the regulatory transition windows to lock quality-first supply chains rather than postponing testing investments.

- Pursue selective partnerships with large-capacity processors or equipment providers to secure throughput and lower per-unit costs.

- Consider bolt-on acquisitions to accelerate access to engineered-product markets (construction, textiles) where substitution economics are strongest.

Next steps

For teams finalizing 2026 budgets, timing matters. The macro trajectory — a projected rise from USD 255.0 Million in 2025 to ~USD 721.8 Million by 2032 at a 16.1% CAGR — makes a strong quantitative case for early positioning. But success will come down to execution: aligning compliance programs, securing processing capacity, and moving quickly on strategic partnerships.

Our full Hemp Market report provides the granular, actionable intelligence needed to convert these strategic imperatives into executable plans. Contact PW Consulting to arrange a briefing, obtain company-level dossiers, and receive the downloadable datasets that underpin our modeling.

For detailed analysis of this topic, please visit the official page:Hemp Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com