Shark Fin Antenna Market: Strategic Preview for 2026 Decision-Makers

As PW Consulting’s lead industry analyst, I present a condensed strategic primer on the global shark fin antenna market — a compact, connectivity-critical product family whose trajectory will materially influence automotive platform strategies, Tier‑1 sourcing decisions, and aftermarket economics through the coming decade. This preview distills the study’s most consequential insights for 2026 planning cycles while intentionally reserving granular segment tables and competitive scorecards for the full report.

Shark Fin Antenna Market

Executive snapshot

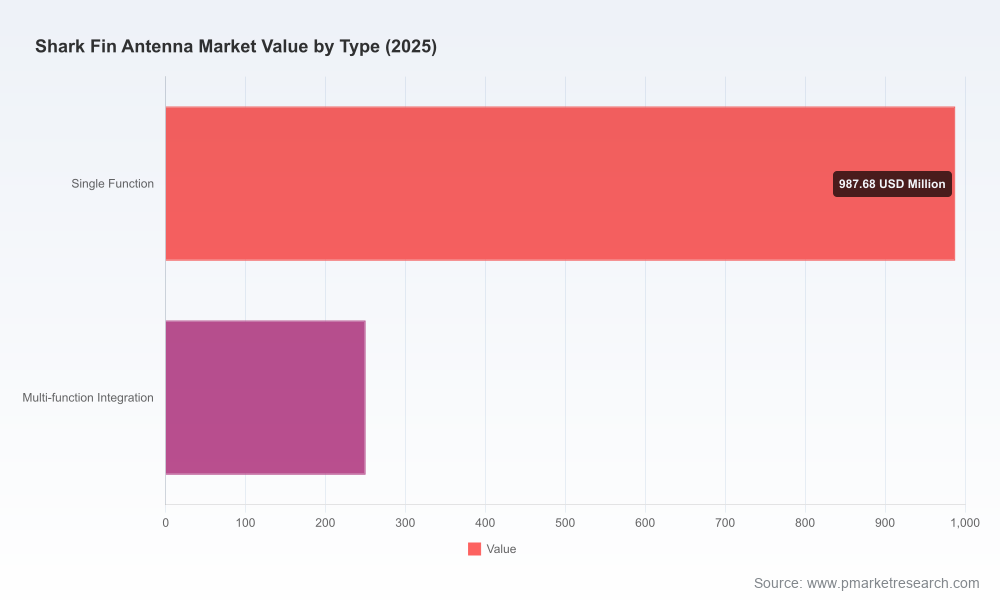

The shark fin antenna market returned to growth following pandemic-era volatility and structural supply shocks. With a 2025 market size in the order of one to two billion USD and a mid-single-digit compound annual growth rate (CAGR) forecast of approximately 7.0% through 2032, the category is expanding under the combined pressure of multi‑radio integration, regulatory testing complexity, and new vehicle architecture choices. Market concentration is meaningful: the top three players control a substantial share of industry revenue, and the top five further consolidate supplier power — a dynamic that shapes pricing, IP, and program-win strategies for OEMs and Tier‑1s alike.

Shark Fin Antenna Market

Why this study matters for 2026 decisions

- Platform design choices: OEMs weighing integrated connectivity hubs versus traditional shark fin modules need a clear view of component cost trends, certification timelines, and aftermarket risk exposure. Our analysis models the economic inflection points where a centralized connectivity hub becomes preferable over distributed antenna modules.

- Sourcing and supply chain resilience: The report quantifies upstream concentration and procurement risk, helping procurement leads design dual‑sourcing and nearshoring strategies that materially reduce lead‑time and cost volatility.

- R&D and product roadmaps: Engineering leaders can prioritize investment (e.g., waterproofing standards, multiband RF front‑end integration, connector robustness) based on technology adoption scenarios and incremental margin analysis included in the study.

- M&A and partnership screening: Corporate development teams gain a pragmatic target shortlist and valuation frameworks for acquisitions or strategic investments in antenna IP, substrate suppliers, and connector specialists.

Market trajectory: what the numbers say (high level)

The category has rebounded from mid‑cycle softness and now projects steady expansion through 2032. This forecast reflects three offsetting forces: increasing functional consolidation (multiband, GNSS, cellular, V2X/5G), OEM platform rationalization that can both depress and reshape module demand, and cyclical aftermarket opportunities tied to vehicle parks and warranty events. PW Consulting’s topline modeling accounts for historical patterns (2020–2025) and generates a base case that shows meaningful growth through 2032 under current macro and technology assumptions.

Shark Fin Antenna Market

Importantly, our scenario framework also models downside outcomes driven by accelerated platform shifts at large OEMs — for example, announced product transitions away from moduleized shark fins towards centralized connectivity hubs — and upside outcomes from accelerated 5G/AV feature uptake and regulatory mandates for connected safety systems.

Dynamics reshaping supplier economics

- Certification friction: Regulatory testing timelines are a critical gating factor. Industry data indicates significant certification delays for 5G and LTE equipment in recent cycles, adding months to program schedules and margin pressure to suppliers that carry pre‑production inventory.

- Component shortages and pricing: RFIC and other semiconductor shortages materially increased procurement costs in recent years — our cost model surfaces where those increases concentrated margin erosion and which supplier practices limited pass‑through to OEMs.

- Material and geopolitical exposure: A large share of critical substrate and flexible printed circuit supply is regionally concentrated, creating meaningful exposure to trade controls and export restrictions. The study quantifies the potential cost and lead‑time impact under different trade policy scenarios.

- Quality and warranty risk: Field reliability issues (notably water intrusion) have prompted extended warranty actions for some vehicle cohorts, creating both reputational risk and a near‑term aftermarket replacement opportunity. Our warranty‑cost scenarios help estimate P&L impact by platform vintage.

Competitive landscape — who matters and why

The shark fin antenna value chain mixes specialized antenna houses, connector specialists, and diversified electrical suppliers. Competitive advantage today is built from three capabilities: RF systems integration, robust manufacturing and quality processes for automotive environmental requirements, and program management scale for complex OEM validation cycles. Key players analyzed in the report include established antenna integrators and component specialists, each with distinct strategic positions:

- Companies with deep RF and multiband packaging expertise — leaders in combined AM/FM, GNSS, cellular and satellite offerings — remain favored for full‑system wins on volume platforms.

- Large diversified connector and interconnect manufacturers have leveraged scale and multi‑domain relationships (vehicle body, power, and connectivity) to integrate shark fin assemblies into broader connectivity packages.

- Specialist vendors of micro RF connectors and precision interface components serve as critical enablers; their supply constraints can become program blockers when vehicle launches are tight.

The study provides vendor scorecards that synthesize technical capability, program delivery history, cost competitiveness and intellectual property posture — essential inputs for Tier‑1 selection and OEM preferred‑vendor lists.

Recent market signals that matter for 2026 strategy

- OEM platform shifts: Some OEMs have publicly signaled transitions from discrete shark fin modules towards centralized connectivity hubs on new platforms. This trend reduces per‑vehicle antenna unit count but may increase demand for higher‑function central modules and new sensor integration strategies.

- Technology enablement: Reference designs and product introductions that meet higher ingress protection ratings (e.g., IP69K) and integrate multiple radios in a single compact housing lower the barrier to fleet and high‑performance deployments.

- Product innovation: Multi‑radio “supercombo” antennas with up to eight integrated functions are moving from concept to commercial availability, shifting competitive dynamics toward suppliers that can deliver validated multiband performance at scale.

Strategic playbook for 2026 (practical moves)

- Scenario planning: Build three investment scenarios (core, accelerated hub adoption, and aftermarket‑led) to stress-test R&D budgets, manufacturing footprints, and pricing strategies.

- Supply risk hedging: Negotiate capacity commitments with critical connector and substrate suppliers, secure long‑lead RFIC allocations, and establish second‑source pathways for high‑risk components.

- Product modularity: Prioritize modular designs that enable field‑replaceable RF subassemblies and permit graceful migration to centralized architectures without stranded inventory.

- Warranty and quality focus: Invest in accelerated environmental testing and rooted design‑for‑service practices to reduce the probability of extended warranty exposure that can erode program economics.

- Commercial leverage: Use consolidated program bundles (antenna + harness + connector) to extract value from OEMs while insulating margins across commodity cost cycles.

What the full PW Consulting study delivers

For decision‑makers who require executable intelligence, the full market research provides:

- Detailed market sizing and forecasting models (2026–2032) with downloadable scenario variants and sensitivity tables;

- Comprehensive competitive benchmarking, including capability matrices, recent program wins, and supplier scorecards;

- Component‑level cost breakdowns and procurement playbooks to model the pass‑through of semiconductor and substrate price swings;

- Regulatory and certification timelines with mitigation templates for program schedule risk;

- Actionable go‑to‑market strategies for OEMs, Tier‑1s, and aftermarket specialists, plus a prioritized M&A/partnership shortlist; and

- Executive briefings and spreadsheet models that translate market forecasts into P&L, cash‑flow and inventory capital requirements for 12‑ and 36‑month planning horizons.

Closing perspective

The shark fin antenna market sits at a strategic crossroad in 2026. On one axis, consolidation and technological integration favor suppliers that can deliver validated, multi‑function modules at automotive scale. On the other, OEM architecture choices — whether to retain distributed antenna modules or centralize connectivity functions — will reshape unit demand and margin pools. For procurement, engineering, and corporate development teams, the imperative is to convert this uncertainty into structured options: de‑risk supply, modularize product platforms, and pursue targeted partnerships that preserve both market access and flexibility.

PW Consulting’s full report equips leaders with the quantitative models, supplier assessments, and tactical playbooks to act decisively. Access to the complete dataset and vendor benchmarking is available through our subscription portal — contact PW Consulting to arrange a briefing and download the full study.

For detailed analysis of this topic, please visit the official page:Shark Fin Antenna Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com