Intravenous Fluid Bags Market — Strategic Briefing for 2026 Decision-Making

As PW Consulting’s senior strategic advisor and industry lead, I present a focused executive primer on the Intravenous (IV) Fluid Bags market that frames the commercial choices facing manufacturers, health systems, and investors entering 2026. This briefing distills the directional forces, competitive vectors, and operational pinch points that will determine market winners in the coming planning cycle — while reserving the complete, segmented intelligence for our full study.

Intravenous Fluid Bags Market

Market snapshot: trajectory and structural signals

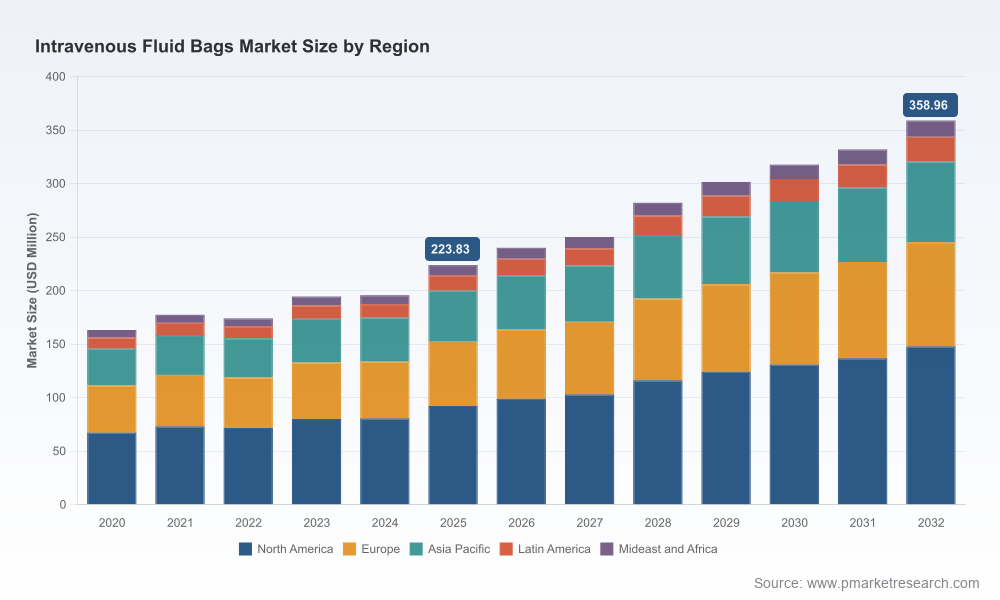

The IV fluid bags market has moved from a mature, largely volume-driven commodity into a dynamic landscape shaped by supplier concentration, material innovation, and regulatory scrutiny. On a macro scale the market’s topline has risen from approximately USD 163.2 Million in 2020 to USD 223.8 Million in 2025 (base year). Under our baseline outlook, steady demand and incremental pricing and product migration underpin a compound annual growth rate of 6.98% across the 2026–2032 forecast window, with the market expanding toward the high hundreds of millions by the end of the period.

Intravenous Fluid Bags Market

These headline numbers mask important operational variability: episodic supply disruptions, shifting preferences toward non‑PVC/DEHP-free systems, and emergent quality/safety vectors tied to extractables and leachables. For decision-makers planning 2026 investments, the combination of healthy topline growth and concentrated supplier dynamics creates both runway and risk — an environment where targeted capability investments can deliver outsized returns if timed and executed correctly.

Intravenous Fluid Bags Market

Why this report matters for 2026 planning

- Actionable foresight, not just forecasts: Our study pairs rigorous demand projections with scenario-based supply continuity modeling and procurement stress tests. That means you can map capital allocation, working capital strategies, and contingency sourcing against plausible shortage and demand scenarios.

- Regulatory risk translated into strategy: Recent regulatory developments — from heightened scrutiny of nitrosamine leachables in infusion packaging to regional bans on DEHP — materially affect material selection, manufacturing validation windows, and product registration timelines. We quantify lead-time and cost impacts so you can prioritize compliance investments versus product-market expansion.

- Competitive playbook for 2026: Leading suppliers are deploying different approaches — capacity expansion, non‑PVC portfolio rollouts, and regional manufacturing footprints to secure public‑sector contracts. Our benchmarking highlights where scale, product differentiation, or nimble niche positioning will win commercial advantage next year.

Key dynamics shaping 2026 decisions

- Supply continuity and resilience: The market’s recent record includes well-publicized shortages of common saline formulations and the subsequent regulatory and buyer responses. Even as acute shortages have been resolved in some regions, the episode exposed single‑source risk and the speed with which procurement teams need validated alternate suppliers.

- Material migration and product differentiation: Buyers are accelerating adoption of non‑PVC, DEHP‑free, and polypropylene bag solutions for both perceived safety and regulatory compliance. Production conversions and new validated lines will be a near‑term capex priority for incumbent suppliers and an entry opportunity for specialized manufacturers.

- Regulatory and quality intensity: Authorities are increasingly focused on leachable small‑molecule impurities and the role of printed overwraps and packaging adhesives. These scientific concerns are triggering additional extractables-and-leachables testing and longer release timelines for new production sites — a hidden cost that materially affects speed‑to‑market.

- Procurement and reimbursement dynamics: Public health agencies have signaled willingness to approve alternate overseas‑registered products to maintain supply continuity; this creates both short‑term relief and long‑term competition pressures as non‑domestic capacity becomes more accessible.

Competitive landscape — what we observed

The industry is anchored by a small set of global incumbents with vertically integrated manufacturing and validated supply chains, alongside a cohort of regional specialists and film/packaging suppliers. Below are concise strategic profiles illustrating the competitive geometry that will matter in 2026.

- Baxter International Inc. (Deerfield, IL; https://baxter.com) — A recognized leader with significant flexible IV bag production capacity. Baxter’s scale and North American manufacturing footprint provide supply reliability and leverage in institutional contracting. Strategic implication: scale affords pricing and contractual advantage, but incumbency must be paired with material innovation to defend share against non‑PVC entrants.

- B. Braun Melsungen AG (Melsungen, Germany; https://www.bbraun.com) — A full‑line IV solutions provider with an active portfolio of DEHP/PVC‑free options and U.S. manufacturing presence. Strategic implication: compliance‑forward positioning and diversified manufacturing reduce regulatory exposure and make B. Braun a preferred partner for health systems prioritizing safer plastics.

- Fresenius Kabi AG (Bad Homburg; https://www.fresenius-kabi.com) — Notable for its freeflex non‑PVC IV bags and recent expansion of U.S.-registered capacity. Strategic implication: quickly commercializing non‑PVC capacity post‑facility launch strengthens Fresenius’ bid position for supply contracts seeking DEHP‑free solutions.

- ICU Medical, Inc. (San Clemente, CA; https://www.icumed.com) — Integrates IV containers with administration systems, enabling bundled value propositions. Strategic implication: systems-level offerings can capture procurement rationalization initiatives by hospitals seeking simplified vendor stacks.

- Specialized manufacturers and material suppliers (e.g., Sippex, Technoflex, Wipak, Renolit, PolyCine, Grifols, Mitra Industries) — These players supply differentiated bag technologies, multi‑chamber formats, and polymer films. Strategic implication: partnerships or supply agreements with these specialists are efficient ways for larger firms to diversify materials and accelerate product conversions without large capex outlays.

Collectively, incumbents and specialists form an ecosystem where scale, validated quality systems, and material innovation determine commercial leverage. For 2026, market advantage will accrue to organizations that pair production resilience with regulatory foresight and procurement agility.

Recent regulatory and market events that matter for 2026

- Regulatory focus on small‑molecule nitrosamines in infusion packaging has intensified. This affects packaging material selection, supplier qualification, and E&L testing regimes — all of which add time and incremental cost to qualification pathways.

- Legislation banning DEHP in certain medical devices has moved more buyers toward alternative polymers, compressing timelines for production conversions and increasing demand for validated non‑PVC supply.

- Regulatory agencies have shown pragmatic flexibility during shortages by approving overseas‑registered alternatives to maintain continuity of care — an important precedent that buyers and suppliers will reference when designing rapid qualification strategies.

- Public agencies have signaled the resolution of recent acute saline shortages in some jurisdictions, but the structural lessons about redundancy, distributed capacity, and validated second‑source lists remain.

What our report delivers — practical, decision‑ready intelligence

The full PW Consulting study is designed as an operational playbook for 2026. It includes:

- Demand and price forecasts (2026–2032) with scenario variations tied to shortage recurrence, material migration, and inflationary regimes.

- Supplier and site‑level risk maps showing validated vs. non‑validated capacity, typical qualification lead times, and contingency sourcing options.

- Regulatory compendium translating leachables guidance, DEHP restrictions, and approval pathways into actionable timelines and testing budgets.

- Competitive benchmarking with capability heatmaps, product portfolio analyses, and go‑to‑market playbooks for incumbent defense and challenger entry.

- Procurement optimization models for health systems, showing how multi‑supplier contracting, safety stock policy, and near‑shoring can reduce shortage risk while controlling total cost of ownership.

- M&A and partnership screen for corporates and private equity — identifying targets by strategic fit, speed of capacity addition, and regulatory readiness.

Immediate strategic recommendations for 2026

- Prioritize validated non‑PVC capacity if your customer base or procurement partners cite DEHP restrictions or heightened leachables scrutiny; early movers capture preferred‑supplier status.

- Establish a two‑tier supplier qualification process: a rapid provisional qualification path for emergency sourcing, and a full qualification path for long‑term supply. This balances speed and quality.

- Invest in extractables-and-leachables testing capabilities or partnerships now. Regulatory attention to small‑molecule nitrosamines means delayed testing will slow releases and contracts.

- For buyers, implement supply continuity scorecards that combine financial, regulatory, and operational metrics — and include contractual clauses for rapid transfer of validated formulations across sites.

- For investors, prioritize assets that either add validated non‑PVC capacity quickly or that offer differentiated materials/packaging with defendable IP or regulatory tractability.

Next steps

This briefing establishes the strategic contours you need for 2026 planning. Our full Intravenous Fluid Bags Market report contains the underlying data tables, supplier‑level assessments, and actionable templates referenced here. It is intended as an operational tool for procurement directors, manufacturing planners, corporate strategists, and investors planning capital or M&A moves next year.

Contact PW Consulting to obtain the complete report and a tailored briefing workshop — we will walk your leadership team through scenario modeling, supplier selection frameworks, and a prioritized set of actions to secure market advantage in 2026.

For detailed analysis of this topic, please visit the official page:Intravenous Fluid Bags Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com