Rubber Diaphragm Market: Strategic Imperatives for 2026 — PW Consulting Insights

As companies prepare their strategic roadmaps for 2026, the rubber diaphragm market presents a mix of steady expansion, structural change and tactical risk that demands informed, decisive action. PW Consulting’s latest study — built on a 2020–2025 historical base and a 2026–2032 forecast horizon — synthesizes market sizing, cost dynamics, regulatory drivers and competitive moves into a practitioner’s playbook for executive decision-making. Below we highlight the strategic value of the research and the high‑priority implications for procurement leaders, R&D heads, corporate development teams and operations executives. This note demonstrates the report’s analytical depth while intentionally withholding select granular splits to encourage full access to the source models and segment-level scenarios.

Rubber Diaphragm Market

Executive snapshot: where the market stands

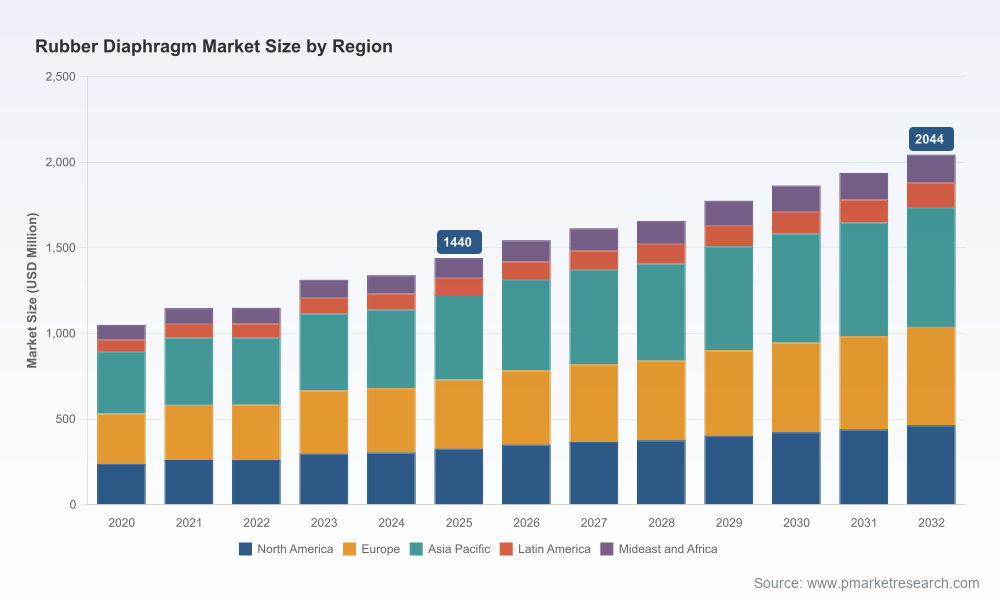

After a period of recovery and structural reorientation, the rubber diaphragm market expanded meaningfully across 2020–2025. Measured in constant USD terms, overall revenue moved from approximately USD 1.05 billion in 2020 to roughly USD 1.44 billion by the 2025 base year. Looking forward, our forecasting model, which embeds raw material volatility, regulatory headwinds, and technology adoption trends, projects a mid-single-digit compound annual growth rate of about 5.16% across the 2026–2032 forecast window — pushing total market size across the forecast to the low‑to‑mid USD 2 billion range by the end of the period.

Rubber Diaphragm Market

Two structural characteristics define the competitive economics: moderate concentration among incumbent suppliers and pronounced product differentiation driven by application‑specific performance and certification requirements. These dynamics create both runway for incumbents to expand margins through value engineering and opportunities for agile specialists to capture premium niches.

Rubber Diaphragm Market

Why this research matters for 2026 corporate decisions

- Prioritizing investment: With predictable, mid‑single‑digit market growth, the critical question for 2026 is not “if” to invest but “where” to allocate scarce engineering, certification and capital resources to maximize ROI. Our study provides the decision filters to rank product, material and geography investments against market growth, margin elasticity and regulatory complexity.

- Supply‑chain resilience: The industry remains sensitive to elastomer feedstock cycles. Historical shocks — for example, a pronounced spike in synthetic rubber and butadiene prices in 2023 that materially increased diaphragm production costs — demonstrate the need for proactive hedging, supplier diversification and design choices that reduce cost exposure without compromising performance.

- Regulatory and certification roadmap: Diaphragms used in safety‑critical domains (aerospace, medical, energy) face rigorous, regionally variable standards. The report maps certification paths, lead times and cost implications — crucial inputs when evaluating time‑to‑market for new applications such as hydrogen systems or high‑vacuum pneumatic controls.

- M&A and partnership targeting: Consolidation activity and capability acquisition are practical levers for scaling technical breadth quickly. The research surfaces acquisition archetypes and commercial synergies that are most value accretive under different growth scenarios.

What’s in the report — practical, decision‑ready deliverables

- Macro market sizing and forecast model (2020–2032) with scenario capability (base, downside, upside) to stress test strategic options.

- Cost and pricing workstreams: detailed bill‑of‑materials and manufacturing cost models, plus margin sensitivity to raw material swings and durometer mix.

- Segment playbooks (by type, material and end‑use) that translate market opportunity into product prioritization matrices and go‑to‑market tactics — presented at an actionable level while omitting proprietary split tables in this summary.

- Regulatory and certification playbook: step‑by‑step pathways, expected timelines, and capex/OPEX profiles to achieve aerospace, medical and defense approvals.

- Supply‑chain heat maps that identify single‑sourced nodes, substitution options (materials and fabric reinforcements) and recommended contract structures for price and availability protection.

- Competitive landscaping with capability matrices, and a shortlist of strategic moves (partnerships, bolt‑on acquisitions, technology licensing) tailored to three corporate archetypes: incumbent integrator, niche specialist, and private equity/new entrant.

- Executable toolkits: supplier scorecards, unit economics templates, NPV calculators for plant investments, and a 90‑day implementation agenda for market entry or expansion initiatives.

Competitive landscape: trends and tactical implications

The industry mix includes diversified industrial conglomerates, precision specialty manufacturers and targeted niche players. Market concentration is moderate; the top three suppliers account for roughly a third of industry revenue, and the top five approach just under half — a structure that enables both scale advantages and opportunities for differentiated entrants.

Recent moves illustrate the industry’s strategic contours:

- Consolidation for capability: DiaCom’s acquisition of a well‑known molded diaphragm firm in 2025 expanded its portfolio and underlines an M&A playbook focused on integrating engineered seals and accelerating access to critical customer relationships.

- Product innovation aligned with energy transition: DiaCom followed its acquisition with targeted product introductions for hydrogen production, storage and fuel cell applications — a signal that suppliers are prioritizing new materials and elastomer formulations for emerging energy disciplines.

- Certifications as a competitive moat: A leading custom diaphragm manufacturer achieved Department of Defense Joint Certification Program registration and MIL‑SPEC/ASTM compliance in early 2026. These credentials materially change bid eligibility in defense and aerospace procurement and justify premium pricing in those segments.

- End‑market diversification among legacy players: Large sealing technology firms and industrial suppliers are leveraging cross‑sell opportunities into adjacent product families (valves, pumps, measurement devices), creating integrated solutions that raise switching costs for buyers.

For 2026 decisions, this competitive picture suggests three tactical imperatives: (1) pursue targeted capability buys (certifications, hydrogen‑compatible elastomers, fabric‑reinforcement expertise), (2) develop pricing frameworks that reflect contract length and raw material pass‑through mechanics, and (3) invest selectively in branded systems where integrated solutions increase lifetime value.

Market dynamics you cannot ignore

- Raw material volatility: Past feedstock shocks materially widened unit cost dispersion across suppliers. Long‑term contracts, vertical integration of key elastomer inputs, and material substitution R&D are practical mitigants explored in the full study.

- Regulatory complexity: Certification timelines and regional differences can add months and millions to product commercialization. Early engagement with certifying bodies is essential; the report provides archetypal timelines for critical approvals.

- Application‑driven material mix: Specialty elastomers and fabric reinforcements command different cost structures and margin profiles. The strategic choice between focusing on commodity diaphragms versus engineered specialty units is a major determinant of capital intensity and return on invested capital.

Recommended 2026 playbook — five priority moves

- Lock in feedstock resilience: execute multi‑tier supplier contracts and selective financial hedges; evaluate strategic sourcing hubs where cost and regulatory alignment reduce lead‑time risk.

- Accelerate certification for strategic applications: prioritize accreditation for hydrogen, aerospace, and healthcare where market growth and margin uplift are highest.

- Pursue capability M&A selectively: prioritize targets that close capability gaps (fabric reinforcement, high‑vacuum engineering, hydrogen elastomers) and offer immediate cross‑sell paths.

- Rationalize product portfolio with clear margin buckets: focus internal R&D on high‑value, defensible product families while outsourcing commoditized runs to contract manufacturers through tightly governed partnerships.

- Embed agility in operations: scale flexible manufacturing cells and invest in digital quality control to shorten time‑to‑certification and increase yield on complex molded parts.

Scenario planning and KPIs

Our full forecast provides three scenarios (base, downside driven by raw material shocks and regulatory delays, and an upside driven by accelerated hydrogen adoption and faster-than‑expected industrial recovery). Core KPIs we recommend tracking monthly include order backlog by application, time‑to‑certification, supplier lead time variance, material cost per unit, and gross margin by product family. These metrics will allow management to pivot investment and pricing decisions within quarters rather than years.

90‑day operational agenda to capture advantage

- Days 0–30: Rapid assessment — run the report’s diagnostic to map your revenue exposure, certification gaps, and supplier concentration.

- Days 30–60: Tactical planning — finalize supplier hedges, narrow acquisition targets, and create a prioritized certification calendar tied to product launches.

- Days 60–90: Execution — begin contract negotiations, initiate engineering changes for material substitution, and deploy pilot production lines with updated QC metrics.

PW Consulting’s rubber diaphragm study is built to be a working document — not a shelf report. It combines market projection models, hands‑on cost tools and a competitor playbook that together convert market insight into executable plans for 2026 and beyond.

To unlock the full segmentation tables, downloadable financial models, supplier scorecards and the competitive capability matrices referenced here — including the confidential split data that underpins our strategic recommendations — access the complete report and accompanying toolkits on our site or contact your PW Consulting engagement lead.

For detailed analysis of this topic, please visit the official page:Rubber Diaphragm Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com