Autonomous Robot Market Is Redefining Logistics, Manufacturing, and Human Productivity

Networking |

2026-05-26 11:45:41

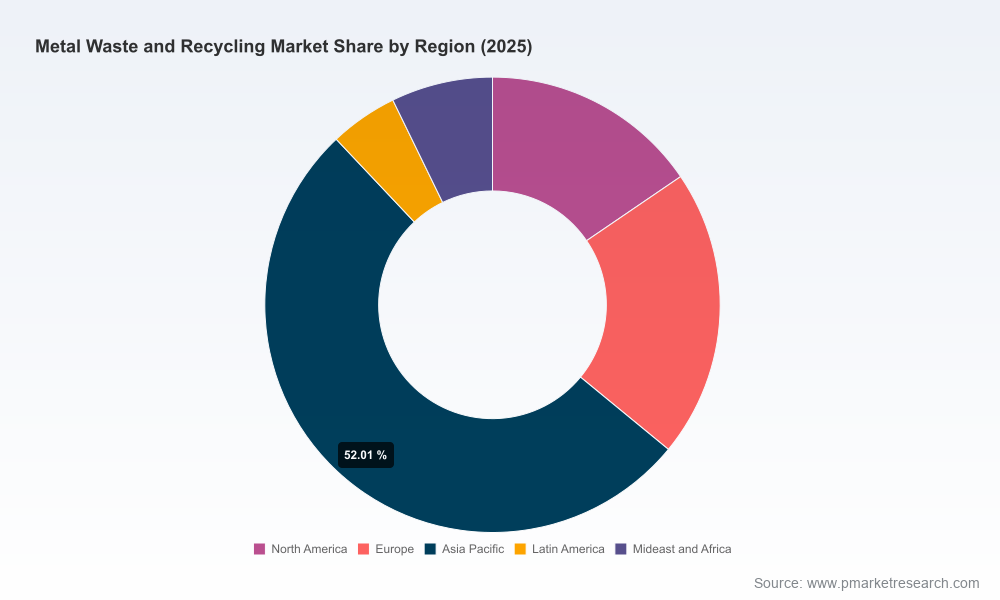

As companies plan capital allocation and supply‑chain strategies for 2026, the metal waste and recycling sector presents a mix of steady expansion, structural disruption and regulatory uncertainty. Our PW Consulting Metal Waste and Recycling Market study—base year 2025, forecast period 2026–2032—shows the market expanding from USD 431.8 Billion in 2025 to an expected USD 576.3 Billion by 2032, underpinned by a 4.2% CAGR across the forecast horizon. Between 2020 and 2025 the industry grew from USD 351.2 Billion to USD 431.8 Billion, reflecting post‑pandemic recovery, increased manufacturing demand and accelerating circularity policies.

Metal Waste and Recycling Market

For manufacturing executives, recyclers, investors and policy teams, 2026 is a pivot year. Macro growth provides a resilient backdrop, but the near‑term strategic environment is shaped by three intersecting forces: technology adoption (sorting, processing, hydrometallurgy and EAF innovations), trade and regulatory actions (tariff regimes and export controls for strategic scrap streams), and evolving supply dynamics (tight ferrous supplies in some markets and differentiated scrap quality profiles). These forces create asymmetric risks and opportunities—rewarding players who move from transactional scrap trading to integrated, technology‑driven value chains.

Metal Waste and Recycling Market

The industry’s expansion is broad‑based yet structurally fragmented. Aggregate market size and mid‑single‑digit CAGR reflect durable end‑use demand (construction, automotive and industrial manufacturing) and rising circularity mandates. At the same time, market concentration remains modest: the top three firms account for under one quarter of global revenue and the top five roughly one third—conditions that encourage local scale plays, selective vertical integration and bolt‑on acquisitions rather than single‑deal global consolidation.

Metal Waste and Recycling Market

These elements are designed to be operational: capex calculators, negotiation levers for long‑term scrap offtake, and an accelerated due‑diligence checklist for acquiring recycling assets.

The competitive field mixes global scrap processors, integrated steelmakers leveraging electric arc furnace (EAF) routes, and specialist non‑ferrous recyclers. Leading names—ranging from large public recyclers to multinational steel groups—pursue three dominant plays: (1) vertical integration into feedstock and production (EAF mills co‑located with scrap yards), (2) multi‑metal processing capability to capture higher‑value scrap streams, and (3) technology differentiation in sorting, contamination removal and metallurgical recovery.

Recent corporate and industry moves underscore these dynamics: multimetal capacity expansions by major copper recyclers and new scrap processing facilities launched in EM/Asia highlight where downstream demand and scrap availability are aligning. At the same time, industry associations and standards bodies are updating specifications and certification programs to improve material quality—and to raise the bar for recyclers that want to access premium markets.

The policy environment has become a first‑order strategic variable. Recent adjustments to import and export rules for strategic metal streams—including expanded tariff measures and calls for export restrictions on certain high‑grade scrap—directly affect economics and supply‑chain design. Firms must assess three realistic policy scenarios for 2026 planning: status quo liberal trade, targeted export controls with domestic content incentives, and broader protection measures paired with domestic capacity subsidies. Each scenario produces materially different price, availability and contract counterparty outcomes modeled in our report.

Beyond tariffs, certification updates and industry studies have immediate operational implications: new specifications for tire wire and other feedstocks affect sorting standards and downstream acceptance; economic analyses that quantify recycling’s contribution to manufacturing increasingly shape subsidy and procurement frameworks.

In line with our “trailer” approach—demonstrating analytical depth while safeguarding the full proprietary modeling—the public summary above integrates aggregate market size, growth rates and high‑impact trends. To preserve competitive value, the report does not disclose granular proprietary splits in this preview: detailed region/application/type revenue shares, unit pricing curves by scrap grade and micro‑segmented demand elasticities are reserved for report subscribers. These core segmentation tables and the full scenario model are central to making project‑level investment decisions and are accessible through the report purchase channel.

The metal waste and recycling market in 2026 is a balance of continuity and change. Robust marketplace growth and expanding end‑use demand coexist with an increasingly strategic policy environment and rapid technical evolution. For firms that invest now in traceability, processing flexibility and thoughtful integration between procurement and production, the sector offers not just cost mitigation but a new source of competitive differentiation. PW Consulting’s full Metal Waste and Recycling Market study provides the actionable detail—financial models, regulatory mappings, and acquisition targets—needed to convert that strategic intent into 2026 outcomes.

Access the full intelligence to move from high‑level insight to executable plan.

For detailed analysis of this topic, please visit the official page:Metal Waste and Recycling Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com