Chemical Peels in Dubai for Skin Glow Enhancement

Other |

2026-05-06 11:20:08

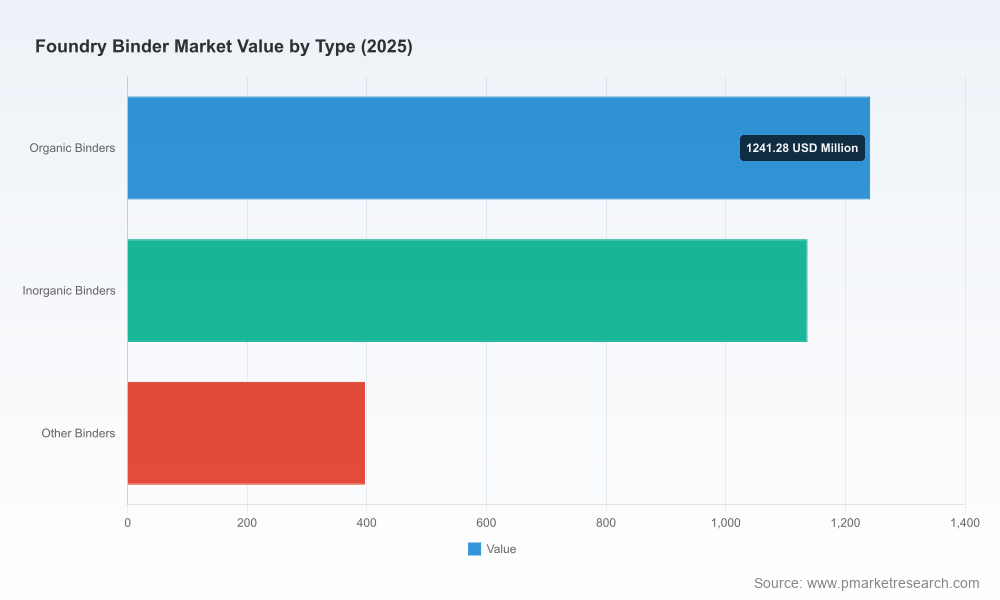

As PW Consulting’s lead industry analyst, I present a concise strategic preview of our Foundry Binder Market study to inform corporate decision-making in 2026. This briefing synthesizes the high‑level, decision‑relevant findings from our base‑year 2025 analysis (historical window 2020–2025, forecast 2026–2032) and explains how executives should translate them into near‑term actions. The research underpinning this note is proprietary and data‑driven: the global foundry binder market was USD 2,775 million in 2025 and is projected to expand at a 4.83% CAGR through the forecast window, reaching roughly USD 3,793 million by 2032. This preview highlights the strategic implications without exposing the granular segment tables and regional splits contained in the full report.

Foundry Binder Market

Input to metallurgical value chains: Foundry binders are a small line item in casting economics but a material determinant of yield, health & safety costs, and end‑part quality across automotive, aerospace and industrial castings. Small percentage improvements in binder selection or process control cascade into meaningful bottom‑line gains for high‑volume casters.

Foundry Binder Market

Transition lever for sustainability and compliance: Environmental regulation and buyer procurement expectations are forcing chemistry-level decisions that affect supplier selection, capital investments, and long-term contracts.

Foundry Binder Market

Consolidation and specialization opportunities: Industry concentration remains moderate—top three and top five suppliers do not dominate the market—creating both M&A and niche leadership pathways for agile players.

Demand fundamentals: The base‑case growth trajectory reflects steady demand from traditional casting sectors, punctuated by cyclical sensitivity to OEM production plans. Our forecast embeds multiple scenarios calibrated to automotive electrification and aerospace production ramps.

Raw material centralization and supply risk: Furfuryl alcohol—the principal feedstock for widely used furan resin systems—remains heavily centralized in China. Independent assessments indicate a remarkable concentration of global capacity and output in that country, creating outsized exposure to geopolitical, logistics, and policy shocks. Procurement teams need to treat furfuryl alcohol as a strategic commodity rather than a routine commodity‑chemical purchase.

Regulatory and buyer pressure: Formaldehyde‑based resins have been materially displaced in certain markets due to emissions and occupational health concerns. Tightening VOC and workplace emission rules are accelerating adoption of low‑emission and inorganic binder solutions. At the same time, REACH‑conform labeling and sustainability certifications (e.g., ISCC PLUS) are becoming procurement gatekeepers in Europe and North America—buyers are increasingly willing to trade higher unit cost for reduced compliance and reputational risk.

Technology and process substitution: Advances in inorganic binder formulations, low‑VOC organics, and process controls (e.g., cold‑box optimizations, alternative curing chemistries) are shifting total cost of ownership calculations. For many foundries, the calculus is no longer just product price but permit risk, worker safety, and scrap reduction.

ASK Chemicals GmbH (Hilden, Germany): ASK has structured its portfolio to cover the full technological spectrum—cold‑box, no‑bake and inorganic systems—coupled with branded offerings that emphasize lower emissions and process stability. Their playbook is multi‑pronged: (1) defend core accounts through integrated service and training programs; (2) expand into emissions‑sensitive segments with targeted product lines; and (3) leverage branded formulations as a differentiation point in tender processes.

Hüttenes‑Albertus Chemische Werke GmbH (Düsseldorf, Germany): Hüttenes‑Albertus has a long track record in synthetic resin systems and sodium silicate binders. Their strategic strengths are technical depth in cold‑setting and thermosetting chemistries and end‑to‑end coating solutions. Expect continued emphasis on formulation compliance (REACH, labeling) and selective product innovations that reduce emissions while maintaining casting integrity.

Strategic takeaways: Leading vendors combine product breadth with application engineering services. Smaller specialized suppliers win by moving fast on niche low‑emission chemistries and by partnering with foundries to share development risk. For buyers, supplier evaluation should weight regulatory compliance capabilities and raw‑material risk management as heavily as supply reliability and price.

Concentration signals window for consolidation: The market exhibits moderate concentration—sufficient room for bolt‑on acquisitions and for regional players to scale through capability aggregation. For private equity and strategic acquirers, attractive targets are those with differentiated low‑emission chemistries, established technical services, or direct channels into large casters.

Procurement and supply‑chain playbook: Given raw material centralization, top options for procurement directors include: diversified sourcing contracts (including strategic inventory corridors), contractual hedges with suppliers, qualification of alternative chemistries, and investment in localized feedstock blending or minor integration to reduce single‑source exposures.

R&D and product roadmaps: R&D budgets should prioritize low‑VOC formulations, inorganic binder performance improvements, and faster qualification cycles with OEMs. Where possible, link product development to identifiable procurement pain points (e.g., reduced emissions permitting costs, scrap rate reduction) so pricing can be value‑based rather than commodity‑based.

Robust sizing and scenario models — base‑year 2025 calibration with a 2026–2032 forecast and sensitivity bands tied to OEM production scenarios and regulatory stress tests.

Supply‑chain exposure maps — supplier, feedstock and logistics concentration matrices that identify “single points of failure” and quantify potential EBITDA impacts under disruption scenarios.

Regulatory impact assessment — jurisdictional rule‑sets and procurement thresholds translated into a compliance cost curve for selected binder chemistries.

Vendor scorecard — capability assessments across chemistry breadth, compliance readiness, technical service, and commercial terms (non‑public benchmarking metrics included).

Commercial playbooks — go‑to‑market options for incumbent suppliers, market entrants and foundries (including pricing levers, service bundling, and certification strategies).

M&A and partnership candidate shortlists — target characteristics and validated screening criteria for acquisition or co‑development opportunities (names only in the full report).

Interactive datasets and models — downloadable tables and scenario workbooks that let users test bespoke assumptions for price, feedstock shocks, and regulatory tightening.

Sourcing: Immediately qualify at least one non‑China heavy supplier pathway for furfuryl‑based resins and evaluate inorganic binder suppliers for two‑year contractual pilot programs.

Portfolio management: Rebalance product portfolios to prioritize offerings with demonstrable low‑VOC performance and verifiable sustainability credentials (REACH/ISCC). Tie roadmaps to measured permit and health & safety cost offsets so sales teams can command value pricing.

Commercial & operations: Implement supplier scorecards that weight regulatory compliance and raw‑material transparency at least equally with price and lead time; require suppliers to disclose feedstock origin for critical chemistries.

M&A posture: For strategic acquirers, prioritize targets that provide either (a) proprietary low‑emission chemistries with scalable production, or (b) technical service capability that reduces buyer switching costs.

This preview surfaces the levers that will matter in 2026: raw‑material exposure, regulatory compliance, and the ability to translate chemistry innovations into commercial advantage. The full PW Consulting Foundry Binder Market report contains the underlying datasets, regional and application splits, detailed vendor benchmarking, and the executable playbooks that corporate teams need to convert these insights into measurable outcomes. If you are responsible for procurement, product strategy, or M&A in the casting value chain, our analysis will reduce uncertainty and prioritize high‑impact decisions. Access to the full dataset unlocks the granular scenarios and calibrated models that underpin the strategic recommendations summarized here.

For decision makers requiring a private briefing or customized scenario runs derived from our model, PW Consulting offers tailored advisory sessions that map 2026 operational choices to three quantified financial outcomes. Engage us to translate industry dynamics into a defensible, value‑creating plan.

For detailed analysis of this topic, please visit the official page:Foundry Binder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com