vRAN Market 2026: Strategic Preview — Why This Research Will Shape Your Next Moves

Executive Summary

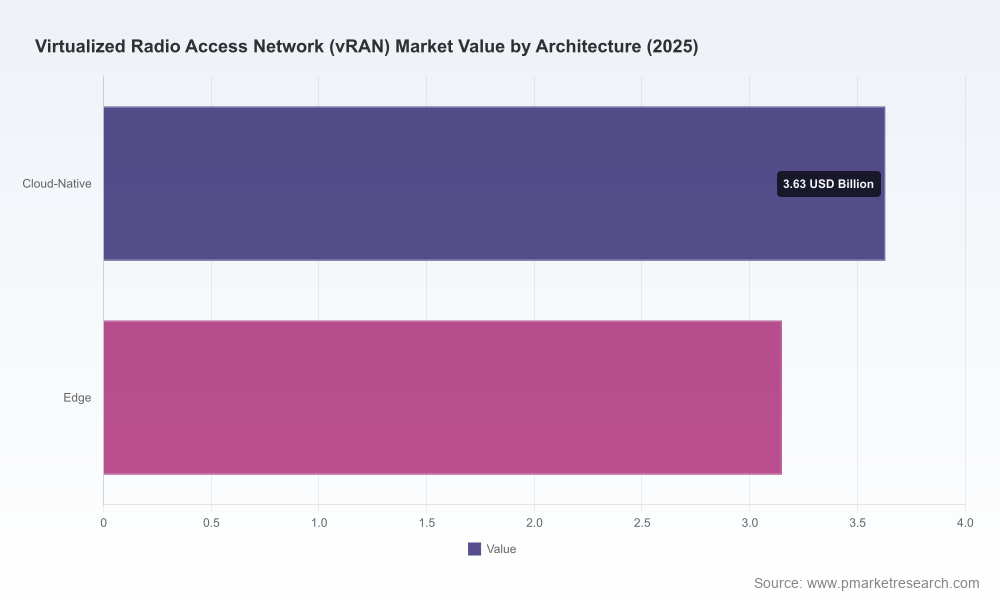

The Virtualized Radio Access Network (vRAN) market is transitioning from proof-of-concept and selective deployments to broad commercial-scale adoption. Building on five years of observable growth through 2025 (base year), our research synthesizes macro trajectories, competitive shifts, technology inflection points, and executable playbooks that matter for strategic decisions in 2026. The market expanded rapidly from the low billions in 2020 to a mid-single-digit total in 2025 (USD, Billion), and—under a sustained compound annual growth rate of 15.65%—is projected to more than double over the 2026–2032 forecast window. This trajectory implies accelerating operator capex allocation to disaggregated, cloud-native, and edge-enabled RAN architectures, and it creates distinct value capture opportunities for vendors, hyperscalers, system integrators, and enterprise private-network integrators.

Virtualized Radio Access Network (vRAN) Market

Why this matters for 2026 decision-makers

- Timing and scale: 2026 is the inflection year where early large-scale pilots convert into significant procurement cycles. Teams that use the right sizing and scenario assumptions in 2026 will secure advantage in vendor selection, spectrum planning, and site modernization budgets.

- Technology strategy: The interplay between cloud-native software, accelerator hardware, and edge-capacity planning will determine both OPEX and energy profiles of next-generation RAN estates. Our analysis isolates the levers that most impact total cost of ownership (TCO) over a 5–7 year horizon.

- Competitive positioning: With moderate-to-high concentration at the top (the three largest vendors do not fully dominate the market), there is room for differentiated entrants and for multi-vendor orchestration models. Strategic alliances—especially around O-RAN conformance and accelerators—will be decisive.

Market trajectory: what the numbers tell you (high-level)

From 2020 through the 2025 base year, the total vRAN market demonstrated sustained expansion driven by 5G rollout, virtualization economics, and operator interest in vendor diversification. The profile of this growth is not linear—investment waves are clustered around large operator refresh cycles and regulatory or ecosystem milestones that validate open-interface interoperability.

Virtualized Radio Access Network (vRAN) Market

Projecting forward under our central-case assumptions, the market continues to grow strongly across the 2026–2032 forecast period at a compound annual growth rate of approximately 15.65%. That growth compounds the strategic opportunity set: vendors able to prove multi-vendor interoperability, energy-efficient hardware acceleration, and cloud-native orchestration will capture disproportionate share as service providers transition from brownfield integration to greenfield and hybrid deployments.

Virtualized Radio Access Network (vRAN) Market

Key dynamics shaping the landscape

- Open interfaces and multi-vendor stacks: Compliance with open standards is no longer optional. O-RAN alignment is a gating factor for many Tier-1 procurement teams because it lowers lock-in risk and shortens integration cycles.

- Compute and accelerator convergence: Hardware accelerators and general-purpose server consolidation are reshaping deployment economics. Single-server consolidation of RAN, AI, core, and security workloads is already being demonstrated in live networks and provides meaningful reductions in power and footprint.

- Energy and TCO intensity: Power consumption reductions are a primary driver of near-term ROI in vRAN upgrades. Energy-efficiency claims from vendors change the math for operators who face both sustainability mandates and rising operating costs.

- Edge economics and private networks: While public-network modernization remains the single largest driver of absolute spend, enterprises and neutral-host deployments introduce high-margin, specialized opportunities for edge-native and private vRAN offerings.

Competitive landscape — what to watch

Our competitive analysis profiles vendor capabilities, go-to-market options, and strategic trade-offs. Below are distilled profiles of the core players that will shape procurement and partnership choices in 2026. These summaries highlight strategic intent and practical implications rather than exhaustive technical spec comparisons.

- NEC Corporation (Tokyo, Japan) — NEC has commercialized 5G-compatible vRAN base station software with explicit O-RAN conformance and containerized architectures. The company is targeting large-scale site rollouts in the near term and emphasizes power reduction as a competitive differentiator. Strategic implication: NEC is positioned for operators prioritizing energy and standards-compliant multi-vendor deployments.

- Samsung Electronics (Seoul, South Korea) — Samsung’s vRAN portfolio demonstrates single-server consolidation in live Tier-1 networks using advanced Xeon-class compute, positioning the vendor as a bridge between traditional integrated RAN vendors and cloud-first providers. Strategic implication: Samsung is a strong choice for operators seeking rapid commercialization with consolidated operational profiles and AI-ready roadmaps.

- Mavenir (Santa Clara, USA) — Mavenir champions cloud-native, public-cloud productization and hyperconverged edge AI deployments with validated Open vRAN handovers. Strategic implication: Mavenir is attractive to CSPs and greenfield entrants looking for flexible cloud-hosted models and fast integration with public cloud ecosystems.

- Altiostar (San Jose, USA) — Focused on open virtualized RAN software and disaggregation, Altiostar offers modularity for multi-vendor, cloud-native architectures. Strategic implication: It is a suitable partner for operators building highly disaggregated stacks and needing a software-first integration partner.

- Parallel Wireless (Los Gatos, USA) — Offers software-defined virtualized RAN that supports legacy-to-5G upgrades and emphasizes cost-effective hardware choices. Strategic implication: Parallel Wireless is often considered by operators targeting economical migration paths and by underserved markets where legacy support is a priority.

- Ericsson (Stockholm, Sweden) — Ericsson’s Cloud RAN virtualization portfolio focuses on scalable, cloud-native deployments with emphasis on multi-vendor interoperability. Strategic implication: Ericsson is positioned for large incumbent operators seeking predictable migration paths backed by extensive systems-integration experience.

- Nokia (Espoo, Finland) — Nokia’s virtualized RAN is tailored to integrate with existing infrastructure and offers extensive operator tooling. Strategic implication: Strong for operators balancing legacy asset reuse with modernization ambitions.

- Fujitsu (Tokyo, Japan) — Fujitsu emphasizes orchestration, automation, and integration with enterprise and carrier ecosystems. Strategic implication: Fujitsu is a fit where automation and tailored managed-services playbooks are required.

- Qualcomm Technologies (San Diego, USA) — Qualcomm’s role is primarily as an enabler through hardware accelerators that optimize vRAN data-plane workloads. Strategic implication: Vendors incorporating mature accelerator technology benefit from improved performance/power trade-offs—an increasingly decisive factor in RAN procurement decisions.

Notable recent developments to factor into 2026 plans

- NEC’s 2025 commercialization of 5G-compatible vRAN base station software with strong O-RAN alignment and reported power-consumption reductions highlights how software innovation can translate into rapid site-level efficiency gains.

- Samsung’s 2026 commercial call on a Tier-1 US live network using Intel Xeon 6 SoC on a single COTS server demonstrates pragmatic consolidation of workloads (RAN, AI, core) and significantly tightens the deployment case for AI-native, 6G-ready architectures.

What the report delivers — practical, actionable modules

The full report is designed as an operational toolkit for 2026 planning cycles. Highlights include:

- Proprietary market-sizing and demand scenarios (base, upside, downside) that reconcile historical 2020–2025 trajectories with policy, supply-chain, and macroeconomic variables for 2026–2032 planning.

- Vendor heat-maps and decision matrices that map capability (O-RAN compliance, accelerator support, cloud-native maturity) against procurement needs and operator risk appetite.

- Deployment TCO models and sensitivity analyses that quantify the impact of server consolidation, accelerator adoption, and energy-efficiency gains on multi-year economics.

- Go-to-market playbooks for vendors, integrators, and hyperscalers—covering partnership models, commercial contracting templates, and proof-of-concept (PoC) design blueprints.

- Operational checklists for operators (integration sequencing, performance SLAs, orchestration KPIs) and an executive briefing pack tailored to board-level decision timelines in 2026.

- Case studies of early large-scale rollouts and migration patterns, demonstrating the practical risks and mitigation techniques that matter to deployment success.

Strategic recommendations for 2026

- Prioritize O-RAN conformance and accelerator roadmaps in vendor shortlists—these two factors most materially affect integration timelines and TCO.

- Run parallel TCO scenarios that explicitly model energy savings from accelerated vRAN deployments; small percentage improvements compound significantly across large site estates.

- Design procurement in modular phases: validate interoperability and SLA governance in controlled PoCs before fast-follow scale—and budget accordingly for multivendor orchestration.

- For vendors and integrators: focus on certified interoperability and pre-integrated reference stacks that reduce operator integration burden; for hyperscalers: offer clear edge-onboarding pathways and predictable connectivity SLAs.

- Maintain strategic optionality: the market is consolidating at the top, but room exists for specialized players that deliver demonstrable energy, performance, or integration advantages.

Closing — a trailer, not the full film

This preview surfaces the trends, vendor dynamics, and pragmatic modules that senior leaders must consider in 2026. It intentionally highlights strategic levers and illustrative metrics while withholding the full segment-level tables and granular regional or application splits that underlie procurement-ready models. Those detailed worksheets, vendor scorecards, and downloadable TCO models are available in the full PW Consulting vRAN market research package—designed to be directly plug-and-play into your 2026 budgeting, procurement, and technology roadmaps.

For teams preparing board materials, RFP scopes, or strategic partnerships this year, the combination of high-growth market dynamics, shifting competitive advantage toward open and energy-efficient stacks, and the practical playbooks we provide will materially reduce execution risk and accelerate value capture. Engage with the full report to convert these insights into deterministic actions for 2026.

For detailed analysis of this topic, please visit the official page:Virtualized Radio Access Network (vRAN) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com