Desiccant Dryer Market 2026: Strategic Preview for Decision-Makers

As PW Consulting’s Chief Industry Analyst, I present a focused strategic preview of our latest Desiccant Dryer Market study. This briefing distills the data-driven signals that will matter to executive teams planning capital allocation, product roadmaps, M&A, and operational resilience in 2026 — while preserving the granular segment outputs of the full report for subscription access.

Desiccant Dryer Market

Executive snapshot

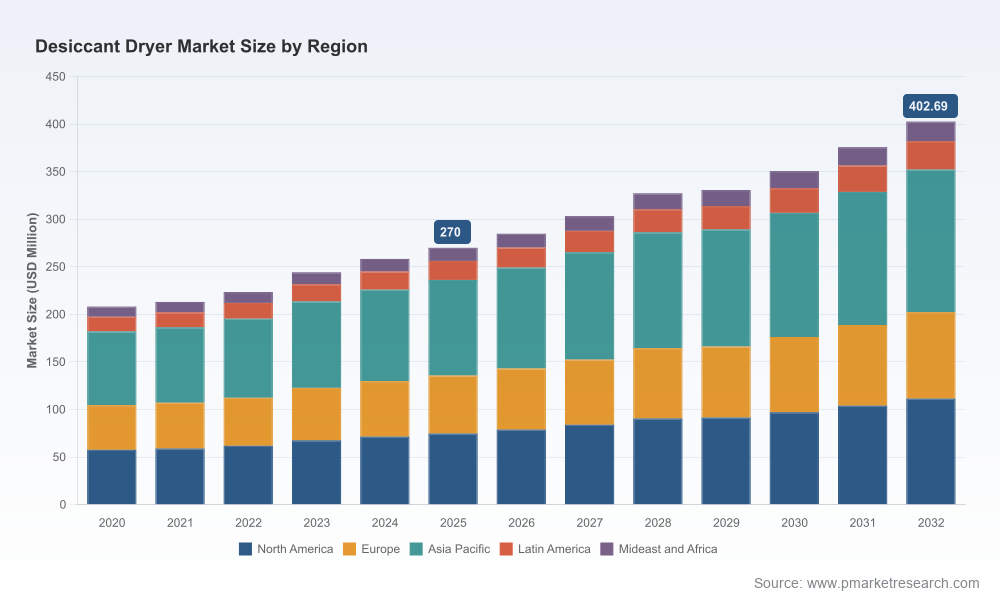

The desiccant dryer market has demonstrated steady expansion through the early 2020s, with our model showing growth from a market size of approximately USD 208.2 million in 2020 to USD 270.0 million in 2025. Looking ahead, the market is projected to expand at a compound annual growth rate (CAGR) of about 6.0% over the 2026–2032 forecast window, reaching roughly USD 402.7 million by 2032. These top-line dynamics reflect a combination of steady industrial demand for high-quality compressed air, regulatory compliance requirements, and selective technology substitution within industrial air-treatment systems.

Desiccant Dryer Market

Why this matters for 2026 strategy

- Portfolio prioritization: A mid-single-digit CAGR in an established capital equipment sector indicates that incremental share gains and margin expansion will come from targeted product differentiation (energy efficiency, uptime guarantees) rather than broad volume swings. Companies must prioritize product features that reduce total cost of ownership and support compliance with ISO 8573-1 air quality expectations.

- Capex vs. Opex trade-offs: Buyers increasingly evaluate dryers on lifecycle economics (energy consumption, desiccant replacement, maintenance downtime). Sellers that can substantiate superior TCO through validated field data will capture a disproportionate share of procurement budgets in 2026.

- M&A and partnership timing: With market concentration indicators showing moderate aggregation (our CR3 at ~52% and CR5 at ~58%), there is room for strategic consolidation. Buyers seeking scale in distribution, aftermarket service, or specific technology stacks should evaluate targets now, before valuations adjust to the mid-cycle growth narrative.

Market dynamics shaping near-term decisions

- Regulatory floor: Compliance with ISO 8573-1 is a persistent baseline for customers across regulated industries. Product claims that explicitly map to ISO classes, backed by third-party verification, shorten sales cycles and reduce procurement pushback.

- Raw material pressure: Input-cost volatility is concentrated in desiccant media supply chains. For example, silica gel pricing in Northeast Asia showed upward movement into late 2025, exerting upward pressure on replacement-cost assumptions. Manufacturers with multi-source procurement, in-house reactivation capabilities, or alternative desiccant chemistries have an immediate cost advantage.

- Energy efficiency as de-risking: Energy-conscious buyers — driven by both corporate sustainability targets and utility cost inflation — favor heated-regenerative and blower-purge architectures only when their energy profile is demonstrably superior across operating regimes. Expect procurement RFQs in 2026 to demand lifecycle energy modelling.

Competitive landscape — what the major players signal

The competitive field blends large industrial conglomerates and specialized OEMs. Our report profiles the leading suppliers to illuminate strategic positioning and capability gaps that matter to partners and acquirers. Highlights from the vendor map include:

Desiccant Dryer Market

- Parker Hannifin Corporation (Cleveland, Ohio) — a broad industrial systems player emphasizing ISO-certified solutions and modular TW/TWP series product lines. Strengths: brand trust, system integration expertise. Strategic focus: leveraging compressed-air expertise to upsell integrated filtration/dryer bundles. (See: ph.parker.com)

- Ingersoll Rand (Davidson, North Carolina) — positions its Hankison line across heatless and heat-regenerative technologies to serve diverse capacities. Strengths: channel reach and service networks. Strategic focus: cross-sell to existing compressor customers to secure lifecycle revenues. (See: ingersollrand.com)

- KAESER KOMPRESSOREN (Coburg, Germany) — offers KAD/KED/KBD regenerative lines oriented to industrial compressed-air systems. Strengths: European engineering pedigree and aftermarket service. Strategic focus: energy-optimized packages tailored to industrial controls integration. (See: kaeser.com)

- Atlas Copco (Stockholm, Sweden) — markets structured-desiccant solutions (CD+/CDR+ with Cerades™). Strengths: R&D resources and global service footprint. Strategic focus: branded desiccant media and portable dryer segments. (See: atlascopco.com)

- BEKO TECHNOLOGIES (Neuss, Germany) — promotes energy-saving and heatless series (DRYPOINT XC and RA). Strengths: niche efficiency claims and European market position. Strategic focus: energy-sensitive customers and lifecycle optimization services. (See: beko-technologies.us)

- Van Air Systems (Lancaster, Pennsylvania) — targets harsh-environment applications with HL and HLSXA regenerative heatless dryers. Strengths: ruggedization and corrosion resistance. Strategic focus: downstream aftermarket and OEM partnerships for specialty applications. (See: vanairsystems.com)

- Zeks Compressed Air Solutions (Pennsylvania) — differentiates with deep-dewpoint capability (−40°F to −100°F pressure dew points). Strengths: performance differentiation for critical-process buyers. Strategic focus: high-spec segments such as pharmaceuticals and electronics. (See: zeks.com)

- Aircel LLC (Naples, Florida) — emphasizes blower purge and heated designs with corrosion-resistant construction. Strengths: materials engineering and niche product customization. Strategic focus: aftermarket replacement and retrofit markets. (See: aircel.com)

Together, these profiles reveal a market where engineering differentiation (desiccant type, regeneration strategy, dew-point performance) and service reach determine competitive advantage more than commoditized pricing.

What the full report delivers — practical content for 2026 action

Our full study is designed as a decision-support toolkit. Key deliverables include:

- An interactive market model (historical 2020–2025 and forecast 2026–2032) with scenario toggles for energy prices, raw material shocks, and regulatory stress tests.

- Segment-level narratives and sizing (by product architecture and end-use) that translate into addressable market and TAM/SAM/SOM matrices — note: segmented datapoints are available in the full report only.

- Supplier scorecards and a commercialization heat-map that benchmark companies across R&D, channel coverage, after-sales services, and price-to-performance.

- Buyers’ procurement playbooks and TCO calculators that reflect maintenance, desiccant replacement cycles, energy burn, and expected uptime impact.

- M&A target shortlists and diligence checklists emphasizing bolt-on capabilities (service networks, controls/IP, desiccant supply security).

- Regulatory compliance checklists and certification pathways mapped to ISO 8573-1 and related quality regimes for critical industries.

Risk matrix and sensitivity highlights

- Desiccant supply risk: Price movements and single-source dependence can compress aftermarket margins and increase buyer resistance. Scenario-testing in the report models silica gel price volatility and substitution pathways.

- Technology risk: Advances in alternative moisture control (e.g., membrane dryers for certain applications) could erode low-end heatless volumes. Firms should monitor cross-technology substitution thresholds tied to operating pressure and dew-point requirements.

- Demand-side concentration: While the market exhibits moderate concentration at the top end, pockets of high buyer concentration in specific industrial segments create supplier dependence risk that we quantify in the full dataset.

Recommended 90-day executive playbook (for Q2–Q4 2026 planning)

- Immediate (0–30 days): Validate OEM claims on ISO 8573-1 performance for your installed base; prioritize retrofit candidates where TCO improvements exceed internal hurdle rates.

- Near-term (30–60 days): Stress-test supplier contracts for desiccant supply continuity; negotiate price-protection clauses or secure secondary suppliers to lock in replacement-material exposure.

- Mid-term (60–90 days): Accelerate pilot deployments of energy-optimized units (heated-regenerative or blower-purge with proven payback) in high-utilization sites; collect metered data to build a repeatable sales case.

Conclusion — where to focus for differentiated outcomes

The desiccant dryer market in 2026 remains an attractive, stable-growth industrial segment. Success will flow to organizations that combine: (a) demonstrable ISO-aligned performance, (b) transparent lifecycle economics, (c) resilient supply chains for desiccant media, and (d) scalable aftermarket/service models. The full PW Consulting study packages the granular models, segment breakdowns, vendor scorecards, and acquisition targets that executives will need to transform these strategic priorities into measurable outcomes.

To access the complete datasets, interactive models, and the full segment-level intelligence that underpin this preview, please consult the full report landing page — it contains the detailed breakdowns and appendices intentionally omitted here to preserve the value of the subscription-grade analysis.

For detailed analysis of this topic, please visit the official page:Desiccant Dryer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com