ROI and Reporting for eCommerce SEO Services

Other |

2026-06-18 07:59:57

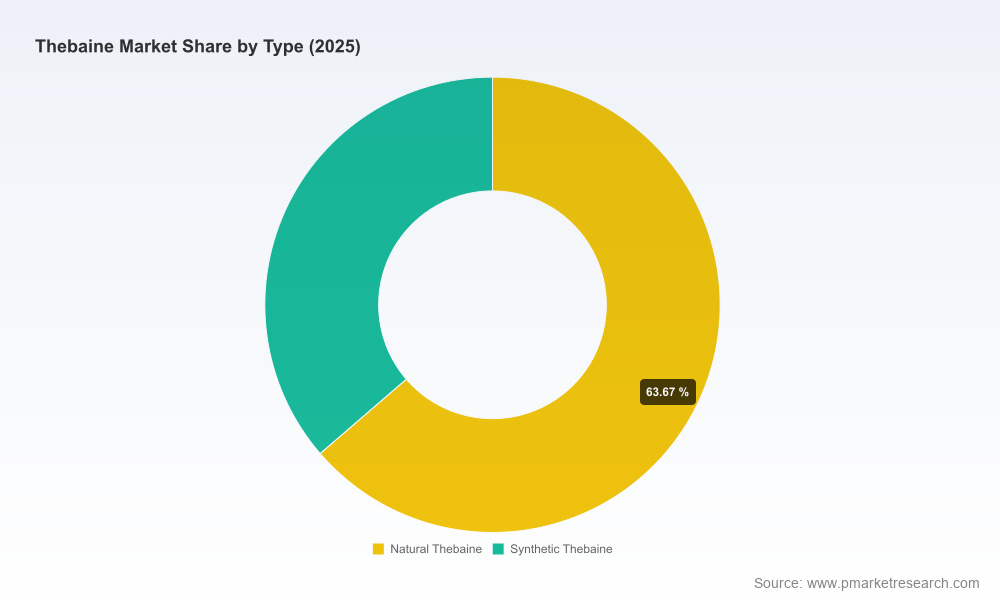

As senior industry advisers at PW Consulting, we view thebaine not simply as an input commodity but as a strategic lever for pharmaceutical supply-chain resilience and product lifecycle risk management. Our latest Thebaine Market study (base year 2025) shows a well-established growth trend: the market expanded materially from the beginning of the decade and reached USD 186.03 Million in 2025, with our forecast modelling indicating continued expansion through the 2026–2032 horizon at a compound annual growth rate (CAGR) of 7.3%, reaching an expected USD 300.2 Million by 2032. Parallel to this growth are concentrated supplier structures and accelerating technological shifts that will reshape sourcing strategies and regulatory engagement for the remainder of the decade.

Thebaine Market

Strategic dependency. A small number of suppliers continue to account for the large majority of global thebaine processing capacity, creating single points of failure that can transmit shocks into opioid API supply chains and downstream drug availability.

Thebaine Market

Technological inflection. The emergence of biosynthetic production pathways is changing the supply economics and onshoring options for controlled-ingredient manufacturing — a shift that alters the calculus for procurement, investment in capacity, and regulatory strategy.

Thebaine Market

Regulatory and policy tailwinds. National programs and quota-setting authorities are increasingly active, reframing what “secure supply” means for drug manufacturers, contract organizations, and health authorities in 2026 and beyond.

On the surface, headline growth (CAGR 7.3% from 2026–2032) signals healthy demand for thebaine-derived APIs used in pain management, addiction therapies and overdose reversal products. Beneath that headline, however, the market is characterized by two structural realities. First, concentrated processing capability magnifies geopolitical, climatic and regulatory risk; our concentration metrics indicate that the top three players control a very large share of the market (CR3 ~87.5%), expanding only slightly when the top five are included (CR5 ~92%). Second, supply-side innovation is creating parallel sourcing pathways: traditional alkaloid extraction from poppy straw remains commercially dominant today, but biosynthetic platforms have entered commercial scale, creating the potential for meaningful onshore supply alternatives within a short planning horizon.

Commercial biosynthesis: A notable milestone occurred when a next-generation biomanufacturing firm completed its first commercial delivery of biosynthetically produced thebaine in late 2024. That delivery validated biomanufacturing at commercial scale and spawned follow-on commitments and procurement discussions in 2025–2026.

Public-sector supply initiatives: Authorities have signalled stronger interest in domesticizing critical-ingredient manufacture for opioid-related APIs. Government awards and programmatic support for onshoring biomanufacturing capabilities are now part of the competitive landscape and will influence capital allocation and contract negotiations.

Production controls and quota management: Regulatory quota mechanisms for controlled substances remain a central determinant of available supply. Firms will need to actively incorporate quota risk into sourcing models and inventory policies to avoid production interruptions.

Agricultural supply volatility: Global output from agricultural sources has contracted relative to previous years, tightening availability for processors that rely on poppy straw. This dynamic amplifies the appeal of alternative production routes among API makers and manufacturers seeking supply diversification.

The competitive topology of thebaine supply is best understood as a two-tier system: established processors with vertically integrated agricultural or refinery assets and a new generation of biosynthetic entrants advancing platform-based supply.

Biosynthetic pioneers: Early commercial-stage biomanufacturers have demonstrated the technical feasibility of producing thebaine at scale through fermentation and synthetic biology. Their advantage lies in geographic flexibility, potential to reduce agricultural exposure, and compatibility with national onshoring agendas. These entrants are attractive partners for firms aiming to secure domestic or near-shore supply, and they create strategic optionality for long-term contracting and capacity investments.

Established processors and vertically integrated suppliers: A set of incumbent companies operates end-to-end value chains — from cultivation and straw processing to alkaloid extraction and the manufacture of controlled API intermediates. Their strengths are scale, regulatory experience, long-standing customer relationships, and established compliance frameworks for controlled substances. However, these players are exposed to agricultural input volatility, quota constraints, and growing competition from non-agricultural production routes.

Contract manufacturers and pharmaceutical integrators: Several contract manufacturers and integrated pharma groups hold critical downstream capabilities (refinement, synthesis to finished controlled APIs) and will be pivotal in determining how shifts in raw thebaine supply translate into finished-drug availability. They are also the most likely acquirers or strategic partners for biosynthetic innovators seeking to accelerate market access.

For C-suite leaders, procurement heads, and corporate development teams, the Thebaine Market presents both risk and opportunity. The following are near-term actions we recommend to translate market insight into durable advantage:

Adopt scenario-based sourcing strategies: Move beyond single-point forecasts. Build supply scenarios that layer quota disruption, agricultural shortfalls, quality incidents, and rapid scale-up of biosynthetic options. Stress-test manufacturing continuity under each scenario and define explicit trigger points for contract activation, inventory drawdown, or capacity investments.

Prioritize diversified contracting and manufacturing optionality: Secure a balanced portfolio that mixes long-term offtake with adjustable short-term contracts and options with biosynthetic providers. Include performance clauses tied to regulatory approvals, yield metrics, and supply security to safeguard against supplier failures.

Engage early with platform innovators and regulators: Firms that cultivate collaborative relationships with biosynthetic producers and proactively engage quota authorities and health agencies will be better positioned to shape favorable supply arrangements and obtain priority allocation in constrained environments.

Re-evaluate inventory and safety stock policies: Given the high concentration of supply and quota-driven availability, firms should quantify the trade-off between holding higher safety stock versus securing flexible secondary supply lines. Our probabilistic demand-supply models demonstrate that modest increases in buffer inventory can meaningfully reduce stockout risk for essential therapies.

Screen for M&A and strategic alliances: The convergence of biosynthesis and incumbent scale creates deal opportunities. Target profiles to consider include: (a) biosynthetic platforms with validated production runs, (b) regional processing facilities that provide regulatory continuity, and (c) contract manufacturers that can integrate new feedstocks without lengthy revalidation.

Invest in compliance and traceability systems: As sourcing becomes more multi-modal, provenance and chain-of-custody systems will be essential for regulatory acceptance and payer trust. Digital traceability and audit-ready quality systems reduce transaction costs and speed approvals during supplier transitions.

Our full Thebaine Market report goes well beyond market sizing and narrative. It is structured as a playbook for decision-makers who need to operationalize strategy in 2026. Key deliverables include:

Probabilistic supply-demand models that map quota, agricultural variability and biosynthetic uptake to availability scenarios across the 2026–2032 forecast window.

Supplier risk matrices and a decision tree for procurement teams to qualify and prioritize partners under differing regulatory and logistical conditions.

Contract templates and performance KPIs tailored for mixed sourcing strategies (agricultural feedstock, refined alkaloid, biosynthetic thebaine).

Regulatory pathway mapping that aligns quota processes, controlled-substance scheduling impacts, and approval touchpoints for alternative production technologies.

An M&A playbook highlighting target archetypes, valuation levers and integration risks specific to the thebaine value chain.

To preserve the strategic value of this insight and to comply with proprietary confidentiality, the report intentionally omits some granular segmentation disclosures in public summaries. Companies that require the detailed breakdowns, supplier-level volumes, and modeled price elasticity outputs should consult the full report and dataset.

Between now and 2032, participants that combine disciplined supply-risk management with selective investment in new production modalities will convert today's vulnerability into tomorrow's competitive edge. The sector’s growth trajectory — evidenced by the market’s steady expansion and a projected rise to roughly USD 300.2 Million by 2032 — creates a permissive environment for partnerships, targeted capacity build-outs, and value-accretive M&A. Yet structural concentration and quota-driven supply dynamics mean that complacency will be costly. Firms that move early to diversify, digitize, and align with both biosynthetic innovators and experienced processors will be the ones that ensure continuity of care and capture disproportionate margin expansion as the market evolves.

For procurement and supply-chain teams: commission a rapid scenario audit based on the report’s supply-demand module to quantify exposure and prioritize mitigation steps.

For corporate development: request our target-screening brief to identify near-term partnership or acquisition candidates aligned with your strategic objectives.

For regulators and public health planners: engage with our regulatory mapping to understand how onshoring initiatives and quota mechanisms intersect with therapeutic availability.

PW Consulting’s Thebaine Market study is designed to be the operational cornerstone for these actions. For full access to the data, supplier-level analysis, and proprietary models, please refer to the full report on the PW Consulting research portal.

For detailed analysis of this topic, please visit the official page:Thebaine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com