Best Gold & Metal Detectors from the BR Detectors Dubai Website

Crafts |

2026-04-23 22:34:21

PW Consulting’s new market briefing for Coding and Marking Systems and Solutions positions executives to make high‑conviction decisions in 2026. Our diagnosis combines a quantified end‑market trajectory with actionable adoption playbooks, supplier scorecards, and regulatory impact scenarios. The market is material and growing: after expanding from the low‑hundreds of millions in 2020 to an estimated USD 215 Million in our 2025 base year, we forecast continued momentum through 2032, reaching roughly USD 345 Million. That trajectory reflects a compound annual growth rate of 6.98% across the forecast horizon.

Coding and Marking Systems and Solutions Market

Encoding, marking and traceability are no longer peripheral compliance items; they are operational fulcrums for supply‑chain integrity, anti‑counterfeiting and sustainability reporting. The current capex cycle—driven by pharmaceutical serialization, digital product passport mandates, and food labeling updates—creates a narrow window to embed architecture that will last the next decade.

Coding and Marking Systems and Solutions Market

Market structure is fragmented. Despite a cadre of global vendors and frequent product innovation, the three‑player and five‑player concentration ratios are modest—illustrating ample room for regional specialists and OEM partnerships to capture share through tailored solutions rather than volume pricing alone.

Coding and Marking Systems and Solutions Market

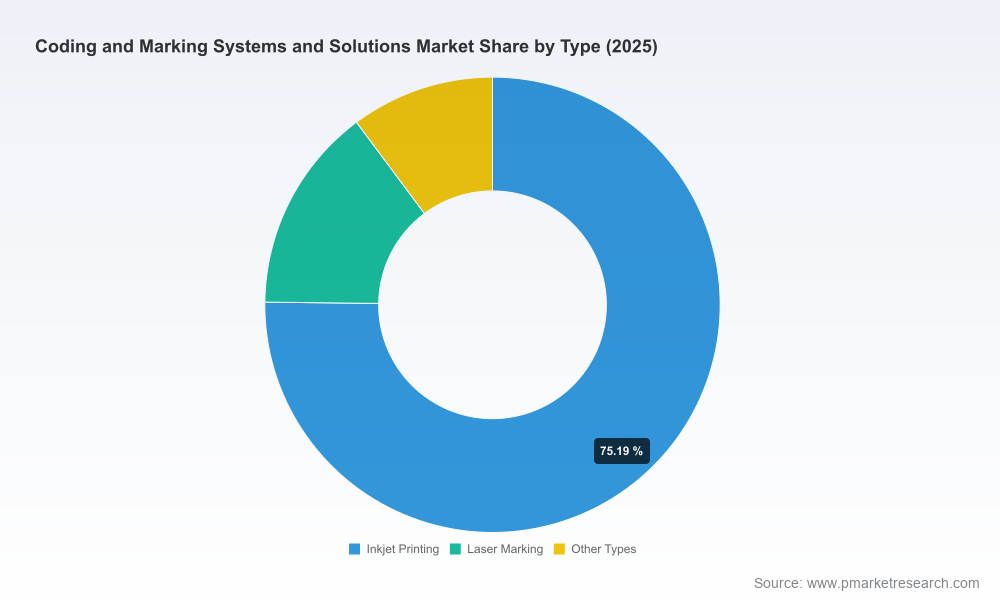

Technology choice now determines downstream agility. Whether the decision is CIJ, laser, thermal inkjet, or integrated labeling, the trade‑offs are no longer purely CAPEX vs. OPEX: they encompass traceability fidelity, consumable ecosystems, verification tooling and lifecycle service economics.

We provide the headline figures above to frame portfolio sizing and investment pacing. Deliberately, this preview omits granular regional and application splits that vendors and strategists consider proprietary decision inputs. Why? Because these splits are the levers you will act upon — channel strategy, service footprint, and R&D focus — and unlocking them is the point of engaging the full report. Think of this article as a high‑resolution trailer: it demonstrates rigour and directional clarity while reserving the tactical maps for authorized use.

The report is built for implementers, procurement leads and corporate strategists. Key deliverables include:

The vendor ecosystem mixes global incumbents, regional specialists and technology innovators. Our competitive analysis synthesizes public product roadmaps, trade show activity and recent launches to reveal emergent battlespaces.

Videojet Technologies (Wood Dale, IL) remains a bellwether on continuous inkjet, laser and labeling platforms. Their emphasis on end‑to‑end traceability and virtualized production demonstrations positions them as a frontrunner for large CPG tiers seeking unified solutions.

Domino Printing Sciences (Cambridge, UK) continues to leverage Industry 4.0 connectivity and consumable ecosystems to lock in recurring revenue — a model that is increasingly attractive to risk‑averse procurement teams.

Markem‑Imaje (Geneva) and Matthews International (Pittsburgh) are competing on high‑speed 2D coding and compliance features; Matthews’ recent XIJ micro‑valve announcement underscores how micro‑fluid innovations are shifting operational economics.

Japanese and German engineering houses — including Hitachi Industrial Equipment Systems, SATO and Paul Leibinger — are advancing solutions that emphasize reliability for high‑throughput lines and sustainable ink chemistries, while also embedding predictive maintenance via machine learning.

REA Elektronik, Koenig & Bauer Coding and regional players such as Control Print and ITW FoxJet are consolidating positions where local regulation and rapid service response are decisive procurement criteria.

Recent industry milestones illustrate the competitive dynamic: new CIJ design philosophies and high‑resolution demonstrations at major trade shows in 2025–2026, machine‑learning enabled label printers launched in late 2025, and product debuts at interpack 2026 that preview the next wave of field‑service and ink innovations. These events are not merely PR — they indicate where R&D and go‑to‑market dollars are flowing.

Regulatory acceleration is the dominant demand driver. Unit‑level serialization mandates and anti‑counterfeit directives have produced sequential investment cycles in laser marking and verification tools. Equally important are standards harmonization efforts (AIAG guidance, ISO 10012, OEM DataMatrix expectations) that create minimum acceptable performance baselines for permanent direct part marking readability.

Three practical takeaways for procurement and engineering teams:

Across the installed base, three trends will dominate TCO and platform choice through the late 2020s:

For example, platforms that offer tight integration between marking hardware, verification sensors and MES/APIs will attract premium valuations and faster procurement cycles from pharma, food & beverage, and electronics OEMs that need validated chain‑of‑custody data.

The coding and marking market is transitioning from a collection of point solutions to an interoperable layer of industrial data capture and compliance. For companies that move in 2026 with a clear TCO lens, a procurement playbook and targeted pilots, there is an opportunity to convert mandatory spend into a platform capability that reduces risk, shortens recall windows and creates new after‑market services.

This article teases the analytical depth and operational frameworks contained in PW Consulting’s full Coding and Marking Systems and Solutions Market report. To access the segmentation matrices, supplier scorecards, ROI models and the complete regulatory scenario suite, please consult the full publication on the PW Consulting report page.

For detailed analysis of this topic, please visit the official page:Coding and Marking Systems and Solutions Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com